Dave Jones, JD, LLM, CFP®, Bailard’s Director of Estate Strategy, provides a practical guide to wallets, exchanges, and trust planning for digital assets.

Cryptocurrency ownership has grown rapidly, and many people now hold Bitcoin, Ethereum, Solana, and other digital assets in wallets or on exchanges, such as Coinbase. Yet estate planning for these assets can be challenging. Unlike most traditional assets, cryptocurrency lacks a straightforward titling or beneficiary framework, which means it does not always fit neatly into conventional revocable trust planning.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

Why Cryptocurrency Requires a Different Approach in Revocable Trust Planning

Traditional assets can often be placed into a revocable trust by changing legal title. A home can be deeded into a trust. A brokerage account can be retitled. Certain assets, such as life insurance policies, generally do not require retitling and instead name the revocable trust as the beneficiary.

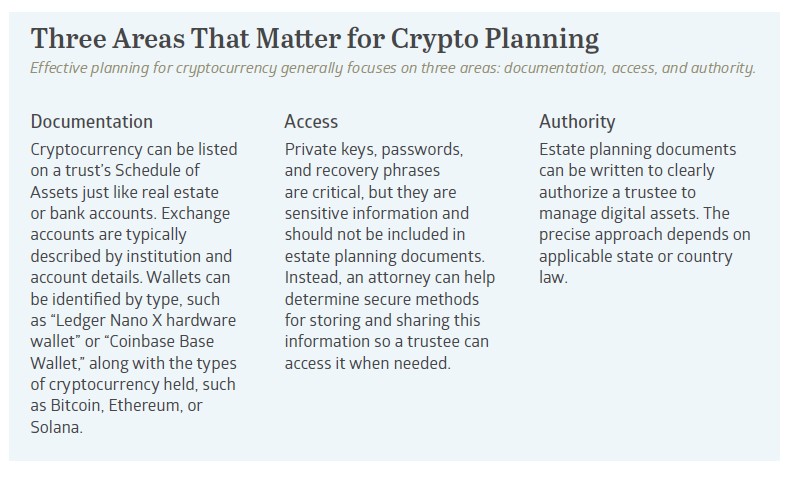

Other assets are handled differently. Tangible personal property—such as artwork, antiques, or collectibles—is commonly addressed by listing the asset on the trust’s Schedule of Assets and, in many cases, by executing a general assignment of personal property. These assets are not retitled in the traditional sense, but they are still brought within the trust’s asset base.

Cryptocurrency fits within revocable trust planning in a similar way, but with an added layer of complexity driven by how the asset is held. For estate planning purposes, the critical distinction is whether cryptocurrency is held directly by the individual in a self-custody wallet or held with an institutional custodian through an exchange account.

Wallets vs. Exchange Accounts

Self-custody wallets such as Ledger, Trezor, MetaMask, or Coinbase Base Wallet are controlled directly by the owner through private keys. There is no institution standing between the individual and the blockchain, which is a decentralized, secure digital ledger that transparently records transactions.

Because there is no traditional “title” to change, bringing wallet-held cryptocurrency into a revocable trust is typically handled by:

- Listing the wallet on the trust’s Schedule of Assets, and

- Executing an assignment of digital assets.

When done properly, a trustee can step in and manage these holdings directly without probate or other court involvement. What wallets generally do not allow is conversion into dollars or other fiat currencies. To liquidate, assets often must be transferred from the wallet into an exchange account.

Exchange accounts operate differently. Personal cryptocurrency exchange accounts generally cannot be held in the name of a revocable trust. Instead, the exchange functions as an institutional custodian and controls the private keys on behalf of the account holder.

During life, exchange accounts make it easy to buy, sell, and convert cryptocurrency to cash. After death, however, access often slows significantly. Institutional custodians are rightly cautious about releasing assets and typically require formal legal documentation to establish authority. Even when an exchange account is listed on the trust’s Schedule of Assets, custodians commonly require:

- A certified death certificate

- Proof of the trustee’s identity

- Court-issued authority, such as letters testamentary or letters of administration

In practice, this often means probate court involvement may still be required, despite advance planning. In California, a limited remedy may be available through a Heggstad petition, which allows a probate court to treat an asset as trust property if it was clearly listed on the trust’s Schedule of Assets, even if it was never formally transferred. While a successful Heggstad petition may help avoid a full probate administration, it still requires probate court filings, legal fees, and several months to complete.

[Note: Some institutional platforms support trust-owned accounts, such as Coinbase Prime, though these are generally designed for business or institutional use rather than personal accounts.]

A Practical Example: How Wallets and Exchanges Are Treated

Consider John, a California resident with two types of crypto holdings.

Wallet-held assets:

John has $150,000 of Bitcoin stored on a Ledger Nano hardware wallet and $50,000 of Ethereum in a Coinbase Base Wallet. Both are listed on his revocable trust’s Schedule of Assets and supported by an assignment of digital assets. When John passes away, the trustee retrieves the recovery information and transfers the cryptocurrency as directed in the trust. No probate court involvement is required, and the process remains private.

Exchange-held assets:

John also keeps $75,000 of cryptocurrency in a personal Coinbase exchange account. Even though the account is listed in the trust, the institutional custodian requires a death certificate, proof of identity, and probate court-issued letters of authority before granting access. This portion of his estate is delayed and requires legal filings.

Wallets may allow for smooth administration within a revocable trust. Exchange accounts held with institutional custodians are more likely to involve probate court oversight, even with advance planning.

Facilitating Access for the Trustee

Facilitating Access for the Trustee

The most important element of cryptocurrency estate planning is coordination. Working with an attorney helps ensure that critical access information is organized, securely documented, and available to the trustee when needed.

Cryptocurrency can be owned by a revocable trust and administered without probate, but only if the trustee can actually access the assets. Control depends on passwords, private keys, recovery phrases, and platform-specific procedures. Because this information is highly sensitive, it should not be included directly in the trust document. Instead, attorneys often help prepare a separate memorandum of instructions that explains where assets are held and how the trustee gains access.

This approach reduces confusion, delays, and court involvement by giving the trustee both clear authority and a practical roadmap for administering cryptocurrency assets.

Key Takeaways

Cryptocurrency does not have to derail a well-designed estate plan. The key distinction lies in how assets are held. Wallet-based cryptocurrency, when properly documented and connected to a revocable trust, may pass to heirs privately and efficiently without probate. Exchange-held cryptocurrency, managed by institutional custodians, may still require probate court involvement before funds are released unless accounts are structured in advance through platforms that support trust ownership.

# # #

This discussion is for educational purposes only and is not legal advice. Always consult a qualified attorney in your jurisdiction for guidance on your specific situation.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.