Jon Manchester, CFA, CFP®, Chief Strategist, Wealth Management, traces a quarter in which the chips moving the market were made of silicon, as an AI-fueled boom handed semiconductors their best three months on record and a hawkish new Fed weighed against mounting signs of speculation.

In 1968, amidst one of the most consequential years in U.S. history, a quiet revolution began in the potato chip industry. With relatively little fanfare, consumer goods giant Procter & Gamble (P&G) entered the fray with a product called Pringle’s Newfangled Potato Chips, using Indiana as a test market. It had been over a decade in development. P&G tasked chemist Fredric Baur with overcoming common complaints about broken or stale chips made by the competition. These manufacturing and logistical challenges had created an industry dominated by local or regional potato chip tycoons who benefited from proximity to stores. P&G aimed to be a national player, leveraging its marketing might to capture a hefty share of this lucrative corner of the snack market. Baur and colleagues came up with both the chip’s distinctive saddle shape—allowing the chips to be tightly stacked—and the iconic tubular can that helped to protect and preserve the chips. Importantly, they also used a mash of dehydrated potatoes and other ingredients, essentially creating a synthetic chip that would last much longer on grocery shelves.

When Pringles finally made its debut, early reviews were underwhelming. In fact, the brand struggled for years, with the New York Times reporting nearly a decade later that the most common gripe was that the chips “taste like cardboard.”1 Once consumers popped, they could stop. P&G also faced strong opposition from the Potato Chip Institute International, which represented close to 400 domestic and foreign chip makers. At issue was the fact that P&G referred to Pringles as potato chips—despite deviating from the dictionary definition. It prompted Time magazine to describe the debate as “The Potato-Chip War” and eventually caused the Food & Drug Administration (FDA) to weigh in. Today, when you toss that can of Pringles® 7-Layer Dip into your shopping cart, you might notice that Baur’s prized creation is labeled “Potato Crisps,” a long-established admission that a product made up of approximately 42% potatoes falls, in fact, into a different category.

It proved to be a momentous 1968 for chips made of silicon as well. In addition to important technological advances for the integrated circuit, Gordon Moore and Bob Noyce left Fairchild Semiconductor and founded Intel (Integrated Electronics). They were dissatisfied with the lack of stock options at Fairchild and tired of meddling by the company’s New York headquarters.2 Roughly two years later, Intel released a dynamic random access memory (DRAM) chip, and the company’s long run atop the industry began. These chips are still central to computer memory. In fact, memory stocks experienced a stunning rally over the last 12 months due to the memory shortage crisis, cheekily referred to as RAM-ageddon. Insatiable data center demand for high bandwidth memory (HBM) has weighed heavily on DRAM supply and forced even behemoths such as Apple to scramble for available product and pay sharply higher prices.

After decades of consolidation, the lone major U.S. memory firm is Micron, whose stock soared 836% during the trailing year ending June 30. In reporting its fiscal third-quarter results recently, Micron said the average selling price of its DRAM spiked by more than 260% year-over-year, while the company’s gross margin more than doubled to 85% from 39%. A few years ago, Micron was losing money. The company posted five straight quarters in the red entering calendar year 2024. Now it occupies the catbird seat, turning what was viewed as a basic commodity into a precious one. In May, The Wall Street Journal pointed out that the world’s three largest memory-chip makers had a combined market capitalization ~22% larger than that of the world’s three most valuable oil companies.3 Boise, Idaho-based Micron, it should be noted, received seed funding from a local potato farmer named J.R. Simplot, who made his fortune supplying frozen french fries to McDonald’s. The humble potato strikes again, albeit in a supporting role.

MO-mentum

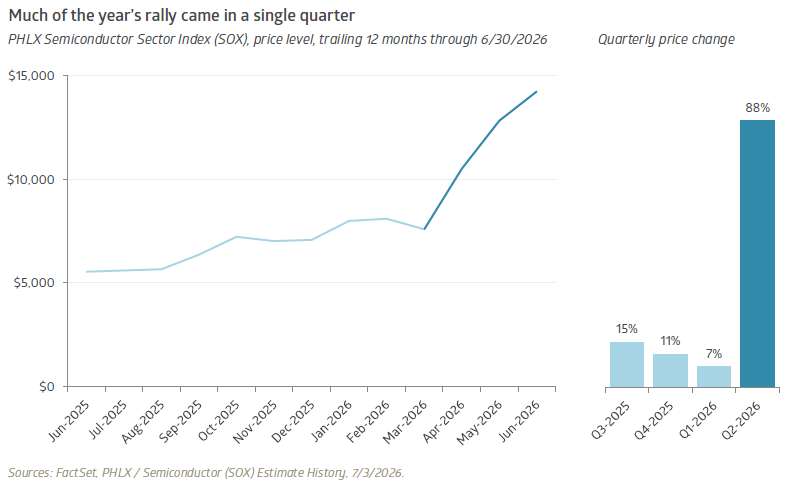

Moore and Noyce were visionaries who foresaw a world in which semiconductors are key to the global economy. Still, they might have been surprised by the meteoric ascent many chip stocks enjoyed in the second quarter. The PHLX Semiconductor Sector Index (the “SOX”) shot up nearly 88%, its best quarter on record. Intel, which had been left behind in favor of the anointed AI winners, gained an astounding 216%. Earnings estimates likewise rocketed higher. At year-end 2025, the consensus Wall Street estimate for the SOX’s 2026 earnings per share (EPS) was roughly $272.4 As the first half of 2026 concluded, that consensus estimate had jumped 76% higher to $479, dampening some of the valuation expansion.

Broadening out to the Standard & Poor’s (S&P) 500 Index, a lot depends on the continued AI spending spree. Our Bailard Research team calculates that just two companies—semiconductor titans Micron and Nvidia—are projected to contribute 31% of the S&P 500’s earnings growth in 2026. Nonetheless, earnings growth looks healthy elsewhere. Even after excluding the five largest expected contributors to 2026 earnings growth, the rest of the Index is forecast to grow EPS at nearly 15%. This forward momentum in corporate profits has allowed investors to keep their chips on the table, betting that this capital expenditures (capex) cycle has room to run. It also means that the S&P 500’s forward price/earnings (p/e) ratio remains at roughly 22x—right where it started the year—despite the Index’s +9.6% price-only advance over the first six months of 2026.

AI remains the predominant theme in the markets, sucking all of the oxygen (and power and water) out of the proverbial room. Questions linger around the durability of the AI capex buildout and regarding the return on investment the hyperscalers (Alphabet, Amazon, Meta Platforms, Microsoft, Oracle) will ultimately see. In June, The Wall Street Journal cautioned that there’s a catch to the impressive earnings growth: much of it is due to a lag in the timing of when the costs of huge AI investments hit the books.5 A large wave of depreciation expense is coming, the article notes, but the big AI spenders can spread these costs over many years on the income statement. According to Todd Castagno, an accounting analyst at Morgan Stanley, the result is “a golden window where everybody looks good.” Longer-term, these AI investments will need to bear fruit in order to sustain profits and feed the ecosystem.

Investors have largely shrugged off AI-related concerns to this point, choosing to ride the momentum. Following the stock market’s 5% melt-up in May, Bank of America strategist Savita Subramanian flagged the widening outperformance of expensive stocks relative to cheap stocks—one of her team’s signals of excessive speculation and potentially a market peak.6 Along with investors piling into stocks that have outperformed—and typically carry higher valuation ratios—we have also seen a surge in margin debt, or borrowing against a brokerage account to invest in securities. FINRA’s data showed that U.S. margin debt rose 54% year-over-year to a record $1.4 trillion in May.7 Further, money has been flowing into leveraged exchange-traded funds (ETFs) that produce double or triple the daily move of underlying stocks. Assets held in leveraged ETFs nearly doubled between March 30 and June 3, according to FactSet.8 Following three straight years of double-digit returns for the S&P 500 Index, perhaps the risk-on mentality has established roots. Leverage is a fickle mistress, though; a lesson best learned not via personal experience..8

Fedspeak, or not to speak

Kevin Warsh could have scripted an easier opening act. Warsh, 56 years old, is the new chair of the Federal Reserve (the “Fed”). He spent his undergraduate years at Stanford, earned a J.D. from Harvard Law School, and served for five years as a member of the Fed during 2006-11. In May, Warsh took the reins with the U.S. embroiled in an on-again, off-again war with Iran that has muddied the global inflation picture. On the domestic front, the Consumer Price Index (CPI) rose at a 4.2% year-over-year pace in May, or 2.9% excluding Food & Energy prices. In his first press conference after announcing that the Federal Open Market Committee (FOMC) would maintain the target Fed Funds rate in the 3.50% to 3.75% range, Warsh acknowledged that, “Persistently high prices are a burden for the American people.”9 He then stated simply: “This Committee will deliver price stability.” Warsh sent a message by choosing to reassure the markets that the Fed will continue its focus on stable prices—without mention of its other mandate, full employment.

With the official unemployment rate well contained at 4.2%, the Fed can afford to lean hawkish. This is reflected both by inflation expectations and in the Federal Funds futures market. The five-year U.S. Treasury Note yield ended June at 4.2%, approximately 230 basis points10 above its inflation-protected equivalent, suggesting relatively tame inflation in the years ahead. Meanwhile, the Fed Funds futures market currently assigns the highest probability to one rate hike by year end, which would take the low end of the target range back up to 3.75%. Warsh has expressed disinterest in providing forward guidance, potentially leaving it to the markets to divine the FOMC’s policy path. He also appears set on embracing brevity: the FOMC’s June statement totaled just 132 words, down from more than 300 words in April.

A concise central banker, who knew? Warsh will no doubt face myriad challenges in the years ahead, which may even require some word-count inflation in future FOMC statements. For now, though, his newfangled Fed sees economic activity “expanding at a solid pace,” aided by a historically robust capex cycle. This should allow more time to focus on monitoring price changes, whether it be chips or crisps.

# # #

1. http://“Pringle’s Loses Some Skirmishes,” www.nytimes.com, 11/14/1976.

2. Chris Miller, Chip War (New York: Scribner, 2022), p. 67.

3. “AI Has Made Memory Chips More Valuable Than Oil,” www.wsj.com, 5/29/2026.

4. FactSet, PHLX / Semiconductor (SOX) Estimate History, 7/3/2026.

5. “Turbocharged Earnings Are Pushing Stocks Higher. There’s a Catch.” www.wsj.com, 6/18/2026.

6. “Too many red flags. Take profits.” BofA Global Research, 6/5/2026.

7. “Margin Statistics,” www.finra.org, 7/3/2026.

8. “The Trillion-Dollar Borrowing Binge Lifting the Stock Market to Risky Heights,” www.wsj.com, 6/28/2026.

9. “Chairman Warsh’s Press Conference,” www.federalreserve.gov, 6/17/2026.

10. A basis point (bp) is 0.01%.

Past performance is no indication of future results. All investments involve the risk of loss. Please see the last page for important disclosures as well as index and category definitions.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.