Lena McQuillen, CFP®, TPCP®, Director of Financial Planning, and Ryan Chavez, CFP®, CPWA®, Investment Counselor, share how timing and diversification decisions shape what employees keep from their equity, and why the best time to plan is before an IPO or a large vesting event.

For many professionals, equity compensation is more than another employee benefit. It is an opportunity to participate in a company’s success and build long-term wealth. Whether your company offers restricted stock units (RSUs), stock options, or an employee stock purchase plan (ESPP), these benefits can become a significant part of your overall wealth.

With several high-profile IPOs making headlines and private companies continuing to reward employees with equity, more individuals are finding themselves with valuable compensation that also comes with unique financial and tax considerations. Understanding how your equity works and setting a plan early, before those decisions arrive, tends to leave you with more options and fewer surprises.

With several high-profile IPOs making headlines and private companies continuing to reward employees with equity, more individuals are finding themselves with valuable compensation that also comes with unique financial and tax considerations. Understanding how your equity works and setting a plan early, before those decisions arrive, tends to leave you with more options and fewer surprises.

Understanding the different types of equity compensation

While the specifics vary by company, most equity compensation falls into a few common categories.

Restricted stock units are company shares granted to employees that vest over time. Once vested, the value of those shares is generally treated as taxable compensation, regardless of whether you sell the stock. Many private companies structure RSUs with a double trigger, meaning shares do not actually vest until both a time-based condition and a liquidity event, such as an IPO, have occurred. One detail that catches people off guard is when the holding period for tax purposes begins. It starts the day the shares are actually released, not the original grant date. For employees at a company that has recently gone public, this can mean a concentrated block of shares becomes eligible to sell all at once, which is worth planning for in advance.

Stock options give employees the right to purchase company stock at a predetermined price, known as exercising the option. Depending on whether the options are incentive stock options (ISOs) or non-qualified stock options (NSOs), the tax treatment and planning opportunities can vary significantly. ISOs carry potential alternative minimum tax (AMT) exposure and require meeting a qualifying holding period to receive favorable tax treatment, while NSOs are taxed as ordinary income at the time of exercise. AMT exposure is not a mystery, and it can be modeled before you exercise, often revealing opportunities to spread purchases across multiple years and reduce or avoid the tax.

Employee stock purchase plans allow employees to purchase company stock, often at a discount, through payroll deductions. While that discount can be valuable, the tax treatment depends on how long you hold the shares. Selling shortly after purchase means the discount is taxed as ordinary income, while meeting the required holding periods can shift more of the gain into long-term capital gains treatment. Knowing which outcome you are choosing before you sell is part of the planning.

Although these programs differ, they share one important characteristic: the decisions you make can have lasting financial consequences.

More than a tax question

One of the biggest misconceptions about equity compensation is that it is simply a tax issue. Taxes are an important piece, and so is how your equity fits into your overall financial plan.

Consider questions such as how much of your net worth is invested in your employer’s stock, or how a downturn at your company would affect both your income and your investments. Should you hold shares after they vest, or diversify into other investments? How will an option exercise affect your cash flow? Are there charitable or estate planning opportunities that could help maximize the value of appreciated shares?

Depending on the shares involved, the answers can draw on tools beyond a simple hold-or-sell choice. Some address the concentration directly through an exchange fund or hedging to limit downside. Others manage taxes or timing, including qualified small business stock treatment, a prearranged 10b5-1 plan for company insiders, or a gift of appreciated shares to a donor-advised fund or charitable trust.

These are planning decisions with real financial consequences.

Avoiding concentration risk

It is natural to feel optimistic about the company you work for. After all, you have invested your time and talent in helping it succeed.

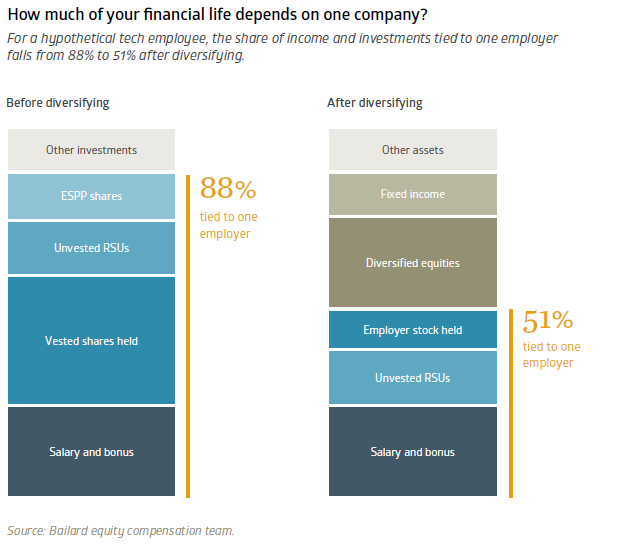

However, many employees unintentionally become heavily concentrated in a single stock. Between salary, bonuses, retirement plans, and equity compensation, a large portion of both their income and their savings may depend on the success of one company. Diversifying helps keep any single investment, or a single employer, from having an outsized impact on your long-term financial security.

Why timing matters

Many of the most important equity compensation decisions involve timing, and small differences in timing can lead to meaningful financial outcomes. Examples include deciding when to exercise stock options, planning for the taxes associated with RSU vesting, and coordinating stock sales with your broader tax strategy. Timing also matters when preparing for a tender offer, IPO, or other liquidity event, and when evaluating whether a charitable gift of appreciated shares makes sense in the same tax year as a large income event.

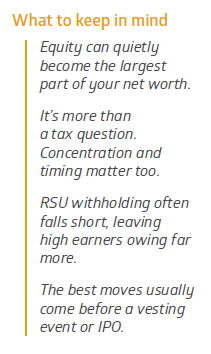

RSU withholding is a good example of why anticipating these moments pays off. Most companies withhold taxes on vested RSUs at the Federal supplemental rate of 22%, but if your total income places you in the 35% or 37% bracket, that withholding falls well short of what you actually owe. On a sizable vest, the difference can reach tens of thousands of dollars due at tax time. For the largest awards, supplemental wages above $1 million in a year are withheld at the top rate, though the gap on the first $1 million remains. Employees who see this coming can set aside funds or adjust estimated payments in advance, while those who discover it in April face an unwelcome scramble. Acting ahead of an event usually leaves more options open.

Every situation is different

Two employees with identical equity awards may arrive at very different decisions depending on their personal circumstances. Someone approaching retirement may prioritize reducing concentration risk and generating income. A younger employee with substantial future earning potential may choose a different strategy. Family goals, tax brackets, charitable intentions, estate planning objectives, and the broader investment portfolio can all influence the best course of action. That is why equity compensation works best when it is viewed as a component of a larger, comprehensive plan.

Getting started

Equity compensation rewards planning ahead. The decisions that matter most, like when to sell or how much to diversify, extend beyond your grant agreement and are easiest to get right when there is time to weigh them. Understanding how your equity fits with your taxes and your long-term goals puts you in a stronger position to make those calls.

Equity compensation rewards planning ahead. The decisions that matter most, like when to sell or how much to diversify, extend beyond your grant agreement and are easiest to get right when there is time to weigh them. Understanding how your equity fits with your taxes and your long-term goals puts you in a stronger position to make those calls.

Whether you are receiving your first equity award, approaching a vesting date, preparing for an IPO, or considering when to exercise stock options, having a thoughtful strategy in place can help you make the most of the opportunity. If you have questions about your company’s equity compensation program, our Equity Compensation Planning team can help you evaluate your options, understand the tax implications, and develop a strategy that fits your situation. We encourage you to reach out before your next major equity event, while there is still time to plan.

A good starting point is often simpler than people expect. Bringing your grant documents, vesting schedule, or option agreement to an initial conversation gives us enough to identify the decisions ahead of you and where timing matters most. You do not need to have already made a decision, or even know what questions to ask. The goal of that first conversation is to map out your equity alongside the rest of your financial picture.

# # #

The tax rates and rules described in this article reflect Federal law in effect as of the date of publication and are subject to change. This material is provided for educational purposes only. Neither Bailard nor any of its employees can provide tax or legal advice. Please consult your tax advisor regarding your particular situation.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.