Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Markets reprice on rapid policy shifts

Dave Harrison Smith, CFA

Chief Investment Officer

March 23, 2026

Policy signals are driving market swings

Markets have swung sharply over the past 72 hours, driven less by fundamentals and more by policy signals.

Late Friday, oil prices surged on news of escalation in the Middle East, alongside President Trump’s threat of potential strikes on Iranian energy infrastructure. By early Monday, that tone reversed, with a pause on military action following reported discussions with Iranian counterparts. Iran has since pushed back, denying meaningful progress.

This kind of whiplash is not new. It echoes April 9, 2025, when markets sharply rebounded after a sudden tariff reprieve. The S&P 500 rose 9.5% in a single session. Policy-driven reversals can be abrupt and non-linear. A single tweet can move mountains.

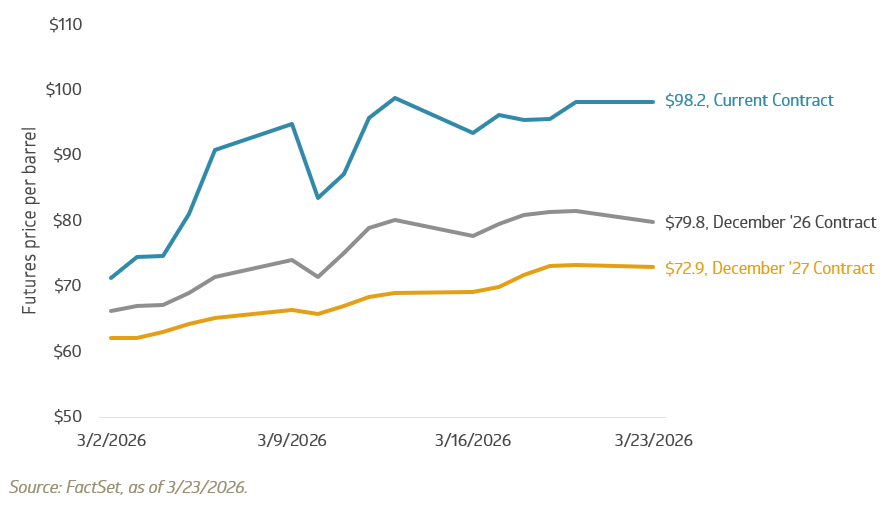

Oil markets are still pricing a de-escalatory base case, with futures below $80 per barrel by year-end and closer to $70 by late 2027. That baseline remains vulnerable to escalation, infrastructure damage, or a more prolonged conflict.

Crude oil WTI futures pricing remains below escalation scenarios

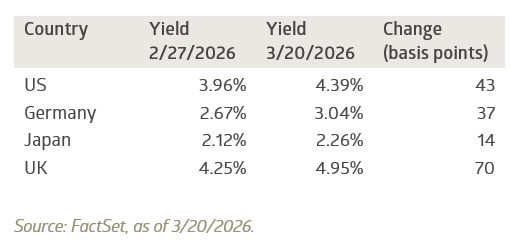

Rising oil prices are already showing up in bond markets

Higher energy prices raise the risk of persistent inflation. That, in turn, is pushing yields higher. Yields have moved higher across major economies as markets reprice a combination of higher inflation, elevated growth risk, and sustained fiscal deficits. As of last week, the U.S. 10-year reached 4.39%, with similar moves across Germany, Japan, and the UK.

Global 10-year yields have moved higher

Short-term yields tell the same story. Just one month ago, futures markets implied a 92% probability of at least one Fed cut, with 2–3 cuts as the most likely outcome. Today, that has shifted materially. Markets now imply a 70.9% probability of zero cuts, with roughly equal odds of either one cut or one hike.

At the start of the year, the expectation was for steady easing. That path now looks less certain. Sticky inflation, geopolitical risk, and the potential pass-through from higher energy prices are all pushing in the same direction.

The outlook has become less linear

The year began with a clear expectation of easing monetary policy. That view has been challenged.

Tighter policy and higher anticipated borrowing costs are starting to show up across equity valuations, bond markets, and investor sentiment. At the same time, uncertainty around inflation and geopolitics is narrowing the range of likely outcomes.

Instead of a clean easing cycle, markets are now adjusting to a more conditional path forward. Policy decisions and external shocks are playing a larger role than many expected at the start of the year.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.