Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy prices test the consumer and the Fed

Dave Harrison Smith, CFA

Chief Investment Officer

March 16, 2026

Energy prices rise, consumer holds for now

The conflict in the Middle East continues, with no clear path to de-escalation. Oil has moved higher, with WTI crude closing Friday near $100 per barrel. U.S. gas prices have also risen sharply, with the national average reaching $3.80 per gallon, up from below $3.00 pre-conflict (source: gasbuddy.com).

Markets, for now, appear to be pricing in a relatively contained and short-lived disruption. Even in best-case scenarios, damage to Gulf infrastructure will likely take months to repair and return to full capacity. As a result, many analysts expect oil prices to remain elevated for much of 2026. Sustained higher energy prices feed into inflation and add pressure on consumers through rising fuel costs.

Encouragingly, the consumer entered March in solid shape. High-frequency spending data from Bank of America showed strong trends in February, and commentary from Visa and Mastercard was broadly constructive at recent investor conferences. Even discount retailer Dollar General reported strong earnings, noting that spending remains “pretty resilient from a consumer perspective.”

Historically, energy shocks act as a tax on consumers. The longer prices remain elevated, the greater the risk of demand shifting away from discretionary categories. The key question is durability.

Sticky inflation complicates the Fed’s path

The Federal Reserve faces a challenging backdrop. Energy prices have surged and will likely pressure inflation in the coming months. While the Fed has historically looked through supply-driven inflation and focused on underlying demand, inflation remains sticky and above target even before the recent escalation.

The February CPI release was mixed. Inflation has moderated but remains above the Fed’s 2% target, with core CPI rising at a 2.5% annualized pace. The read-through to the Fed’s preferred inflation gauge, PCE, may point to somewhat higher inflation given its different basket of goods. Importantly, this data does not yet reflect the recent increase in energy prices.

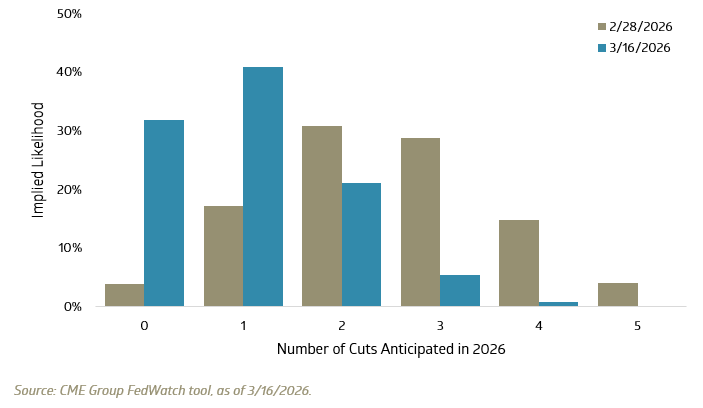

Inflation remains persistent, and markets have adjusted accordingly. Futures markets now price in between zero and one rate cut for the remainder of 2026.

Number of rate cuts expected in 2026, as implied by market futures

Market leadership shifts following the start of the conflict

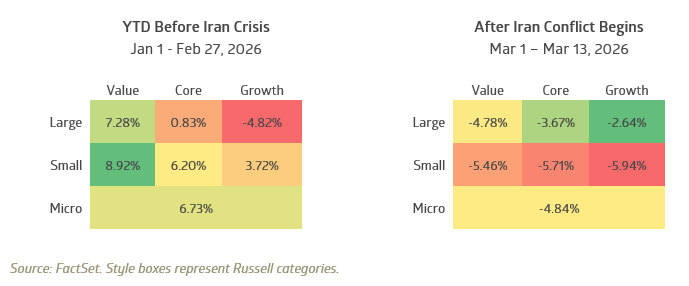

Market leadership has shifted alongside changing rate expectations and rising economic uncertainty. For the first two months of the quarter, small-cap and value stocks outperformed, with small-cap value rising nearly 9% through the end of February. Large growth, dominant in recent years, lagged, with the Russell 1000 Growth Index down 4.8%.

Style returns, before and after the start of the Iran conflict

As the conflict escalated, that leadership dynamic began to reverse. Large-cap growth stocks, while still negative, have held up relatively better. Small-cap stocks have lagged across growth, core, and value styles, reflecting greater sensitivity to economic growth and financial conditions.

The earlier strength in small-cap and value reflected a broadening of participation across U.S. equities. Markets are now re-pricing both economic growth and interest rate expectations in real time.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.