Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The Gulf erupts, oil surges, and markets reprice

Dave Harrison Smith, CFA

Chief Investment Officer

March 9, 2026

The Strait of Hormuz closes and oil surges 60%

The situation in the Middle East has devolved into a fierce and sprawling military conflict. Iran’s response to continued Israel/U.S. strikes has entangled a dozen other countries, with tens of thousands killed or injured, civilian infrastructure shuttered, and energy production and transportation facilities abruptly offline.

Over the past week, the conflict has broadened well beyond initial expectations. This is not a repeat of the targeted strike on Iran’s nuclear facilities in 2025. Iran’s response has drawn in a wide swath of major energy-producing countries. Critically, the Strait of Hormuz—through which roughly 20%/30% of global oil/natural gas supply flows—has effectively closed to shipping traffic. Production shutdowns across Kuwait and other countries reflect not just fear of direct strikes, but a breakdown in transportation and available storage capacity. Systemic complexity is amplifying the energy disruption in ways not fully anticipated.

The impact on oil prices has been dramatic and swift. West Texas crude has spiked from $66.96/barrel at the end of February to above $110 as of this writing. At an increase of over 60%, this places it among the largest six-day moves in three decades and second only, in dollar terms, to the immediate aftermath of the COVID shutdown in 2020. Average U.S. gasoline prices have risen more than $0.50 per gallon in a single week, with further increases likely. Jet fuel has surged as well, foreshadowing higher travel costs heading into summer. Businesses and consumers are reeling.

U.S. equities hold; international markets and bonds sell off

Beyond commodity prices, the financial market reaction has been significant. U.S. equities have been relatively resilient, reflecting the United States’ position as a major energy producer since the shale boom, with the S&P 500 Index down 2.0% and the Russell 2000 Index down 4.0% on the week. International markets have fared worse: the EAFE Index fell 6.7%, and Emerging Markets declined 6.9%, reflecting both the global growth risk from spiraling energy costs and the impact of a strengthening U.S. dollar, which has functioned as a safe-haven currency.

Government bonds have also broadly sold off, failing to provide refuge. Yields on the U.S. 10-Year Treasury increased to 4.15% last week, up from 3.96% at the end of February, while the 2-Year rose from 3.39% to 3.57%. These moves reflect elevated inflation fears and a reduced likelihood of Federal Reserve rate cuts. The market is now pricing in a single cut in 2026, down from the two to three cuts anticipated just last week.

Energy price shocks create a complex dynamic. Headline inflation rises directly; so too does core inflation, as fuel and electricity costs are absorbed into the production costs of goods and services broadly. At the same time, sustained energy price increases tend to compress consumer spending, particularly among lower-income households, where food and fuel represent a disproportionate share of the budget. Our research suggests this segment of the economy is already under meaningful financial stress, and the current shock will deepen that pressure.

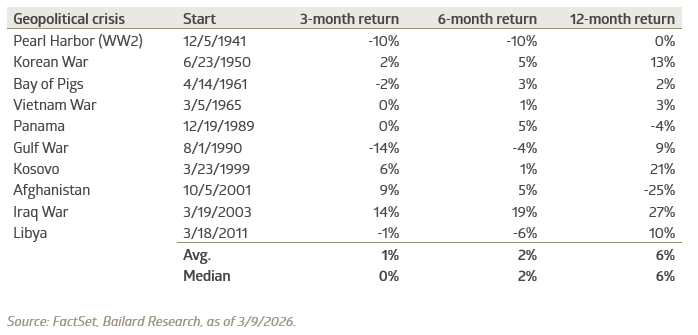

What history says about markets after geopolitical shocks

The news flow remains difficult, and volatility is elevated. A key question worth considering: how much risk is already priced into current market levels? The history of geopolitical events offers useful and heartening context. Past events have often followed a similar pattern: an initial repricing as uncertainty spikes, followed by stabilization and recovery as the situation becomes more legible to markets. The S&P 500 has frequently produced positive returns over the three-, six-, and twelve-month periods following major geopolitical crises, illustrating how quickly these shocks can be absorbed into market expectations.

Market returns following major geopolitical crises

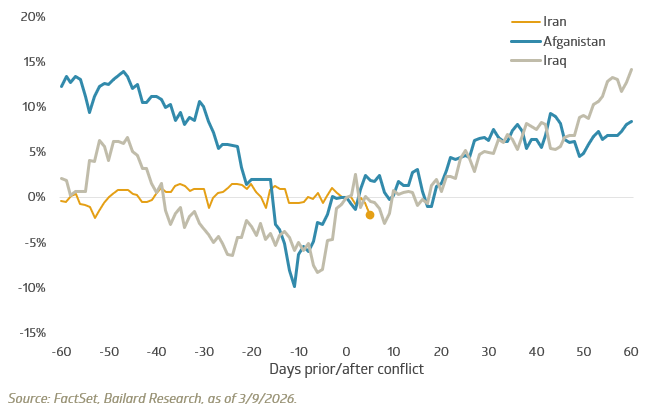

Looking at recent Middle East conflicts specifically, the S&P 500 posted positive average returns over each of these time horizons, rising 11.5%, 12%, and 1% over 1-, 3-, and 12-month periods, respectively. The sample size is limited, and each conflict’s surrounding economic and geopolitical environment is different. This history is best understood as descriptive context, not a forward-looking projection.

S&P 500 Index price return around onset of select conflicts

We remain focused on where risk is concentrated and where dislocations may be surfacing opportunity. Our emphasis on quality across strategies is designed to provide relative resilience in periods like this. We continue to evaluate exposure in areas most sensitive to sustained energy cost increases—across regions, sectors, and individual companies—while remaining alert to the pricing anomalies that fear and volatility tend to create.

In our experience, periods of acute uncertainty often obscure the eventual recovery. When markets begin to anticipate stabilization, recoveries can unfold quickly and well in advance of any formal resolution. In periods of elevated uncertainty, patience and discipline remain among the most durable investment advantages.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.