Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Hot CPI, cooler context

Dave Harrison Smith, CFA

Chief Investment Officer

May 19, 2026

The pain of the post-pandemic surge of inflation remains fresh in investors’ minds. What was initially expected to be a transitory shock persisted far longer than many economists had estimated and eventually forced one of the most aggressive monetary-tightening cycles in more than 50 years. This, combined with the historical tendency for bouts of inflation to be followed by secondary or repeat waves, has left investors anxiously awaiting signs that the global energy crisis is beginning to seep into prices more broadly.

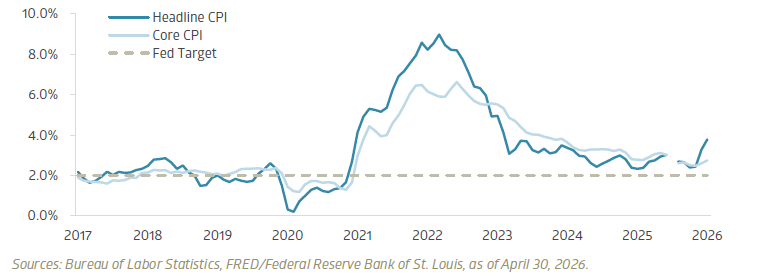

April’s inflation data came in hot and did little to quell concerns. Headline CPI rose 3.8% over last year, accelerating sharply for the second consecutive month. Core CPI, which excludes volatile food and energy prices, also came in above expectations, rising 2.8% from last year. On a monthly basis, headline CPI slowed to 0.6%, with the pace moderating modestly as energy price increases eased after a massive uptick in March. More concerning, however, was that monthly core CPI accelerated to 0.4%, a marked increase from March.

Headline and Core inflation remain elevated (2017-2026)

What drove the surprise

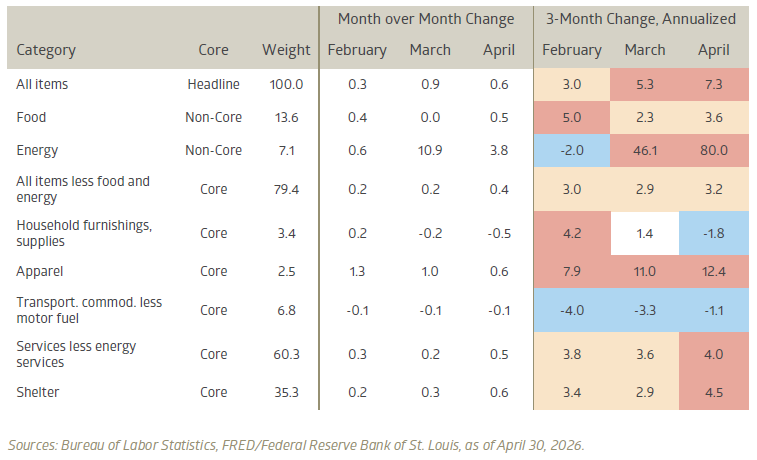

The headline numbers are challenging to digest, but the news may not be as bad as at first blush. A meaningful portion of the price increase was due to technical factors tied to shelter inflation. Due to the government shutdown last October, the Bureau of Labor Statistics did not collect semiannual rent-level data for a cohort and instead carried forward the previous month’s stale data. April’s report laps that temporary data, creating an artificial jump in shelter prices. Given shelter’s large weight in the CPI basket, the 0.6% monthly jump had a significant impact on overall inflation in April. Prior to this month, shelter prices had been rising at a relatively steady rate in the mid-to-high 2% range, indicating April’s figure was significantly inflated and suggesting that we are likely to return to a more normalized monthly pace in short order.

Select CPI components, month-over-month and 3-month annualized changes

Markets reprice inflation risk

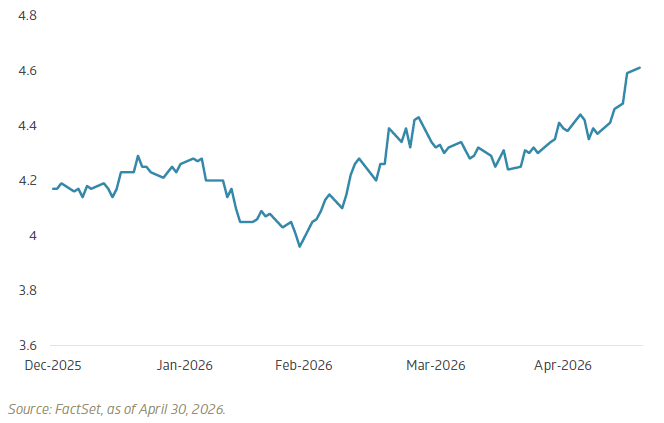

Still, the inflation print was a challenging one for bullish investors. Bond investors were quick to react, with the yield on the US 10-Year note rising to 4.62% on Friday. This represents a 45-basis-point increase since the start of the year (a basis point, “bp”, is 0.01%). Interest rate futures repriced meaningfully, as well, as the market positioning on futures now favors at least one rate hike by year-end. Outgoing Federal Reserve Chair Jerome Powell has consistently emphasized that interest rate tools are less effective against supply-driven inflation shocks such as the current energy crisis. Yet, we know that psychology matters, and that inflation fears tend to become self-reinforcing. The very prominent rise in gas prices may eventually seep into our collective psyche, and the slow creep of broad cost inflation may soon follow.

10-Year US Treasury yield (%) climbs on inflation fears

Duration matters

At the onset of the war in Iran, we admonished that the duration of the conflict would prove as important as the magnitude of the initial shock. The longer the crisis, the more painful the economic implications. We are beginning to see the effects of the conflict’s duration. Global governments have thus far relied on temporary mitigation measures to dull the pain, such as releasing oil from strategic reserves. We are beginning to discover the limits of these measures. Critically, inflation expectations appear to remain anchored despite price inflation beginning to filter into transportation, airline, and grocery prices. For now, at least, the market appears willing to accept that this bout of inflation is supply-driven and temporary. Just don’t call it transitory.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.