Dave Jones, JD, LLM, CFP®, Director of Estate Strategy, and Mikhail Saliba, CFP®, Estate and Financial Planning Associate, outline how state estate and inheritance taxes differ from federal rules and where they come into play.

Over the last several months, we’ve had a noticeable increase in questions about state estate and inheritance taxes. There’s good reason for that. Federal exemption levels have grown quickly, while many state thresholds have not kept pace.

Over the last several months, we’ve had a noticeable increase in questions about state estate and inheritance taxes. There’s good reason for that. Federal exemption levels have grown quickly, while many state thresholds have not kept pace.

As a result, these are not parallel systems. They operate differently, with lower thresholds, different rules, and outcomes that aren’t always obvious. That can change results more than expected.

The gap between federal and state planning

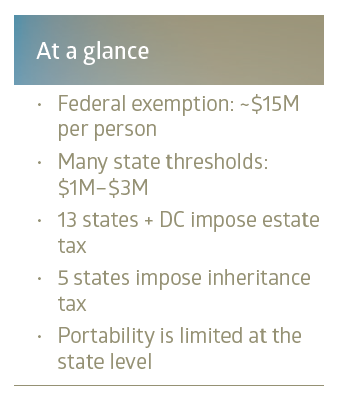

The federal estate tax exemption is now approximately $15 million per person. Many state exemptions sit far below that level, often in the $1 million to $3 million range.

That creates a disconnect. Many with moderate wealth may have no federal estate tax exposure, yet still face meaningful state-level taxes depending on where they live or what they own.

State systems also differ in how they treat married couples. While federal rules allow portability of a deceased spouse’s unused exemption, most states do not. Planning decisions that work well at the federal level may not translate cleanly to the state level.

Location drives the outcome

State tax exposure is not determined by a single factor.

Domicile is typically the starting point. The state considered your permanent home will often govern whether your estate is subject to tax. But other connections matter as well.

Owning real estate or tangible property in another state can create exposure there, even if you do not live in that state. In some cases, inheritance tax rules also depend on who receives the assets and where they reside. When there are multiple homes or long-standing ties to different states, these layers can overlap in ways that are not always intuitive.

How state rules vary

This exhibit highlights how varied these systems are: 2026 state estate & inheritance tax overview. A few patterns stand out:

- Several states impose estate taxes at relatively low thresholds, including as low as $1 million in some cases

- Tax rates can reach into the mid-teens or higher, depending on the state

- Only a small number of states allow portability between spouses

- A handful of states impose inheritance taxes, where the tax depends on who receives the assets rather than the size of the estate

The result is a patchwork. Similar balance sheets can face very different outcomes based solely on geography.

A different kind of tax: inheritance

A smaller group of states imposes an inheritance tax rather than, or in addition to, an estate tax. The distinction matters. Estate tax applies to the value of the estate itself, whereas inheritance tax is paid by the beneficiary, meaning the person receiving the assets is responsible for the tax.

Spouses are generally exempt. Children and other lineal descendants are often treated favorably. More distant relatives or unrelated beneficiaries may face higher rates. That makes beneficiary designations and trust structures an important part of the equation, particularly when planning across generations.

Liquidity can become a constraint

State estate and inheritance taxes are typically due within six to nine months after death. For estates that are primarily liquid, that may not present an issue. But when wealth is concentrated in real estate, private investments, concentrated stock positions, or closely held businesses, timing can become a constraint.

Without planning, decisions can be made under pressure, including the sale of assets at inopportune times.

Balancing planning trade-offs

Addressing state-level exposure often involves coordinating several moving pieces.

Trust structures, including credit shelter and QTIP trusts, can help align federal and state objectives. Charitable planning can also play a role, depending on overall goals and timing. At the same time, these decisions may affect income tax outcomes, including basis step-up considerations.

For married couples, the lack of portability in many states introduces an additional layer of complexity. Decisions made at the first death can influence both the surviving spouse’s tax exposure and flexibility.

In practice, planning becomes less about a single strategy and more about balancing trade-offs across tax, liquidity, and long-term goals.

Easy to overlook, important to address

State estate and inheritance taxes tend to sit outside the federal framework most planning focuses on. That makes them easy to overlook.

For those with multi-state ties, real estate holdings, or evolving residency, state estate and inheritance taxes can meaningfully affect outcomes. Reviewing state tax exposure alongside the broader plan helps ensure that structure, liquidity, and intent remain aligned over time.

# # #

Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.