Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Consumers still spending as balance sheets hold up

Dave Harrison Smith, CFA

Chief Investment Officer

May 27, 2026

Consumer confidence weakened again in May, with the University of Michigan index falling below the previous June 2022 trough and setting a new all-time low. In the survey, consumers frequently cited rising costs of living as the leading factor in their worsening outlook. Expectations for future inflation also played a role, further weighing on sentiment.

The confidence index has been in a downward trend for much of the last two years. This stands in sharp contrast to strong consumer spending data and relative economic stability. Making sense of the sharp divide between ‘soft’ survey data suggesting depressed outlooks (what people say) and strong ‘hard’ spending data (what people do) has been a frequent topic of discussion among economists and financial analysts.

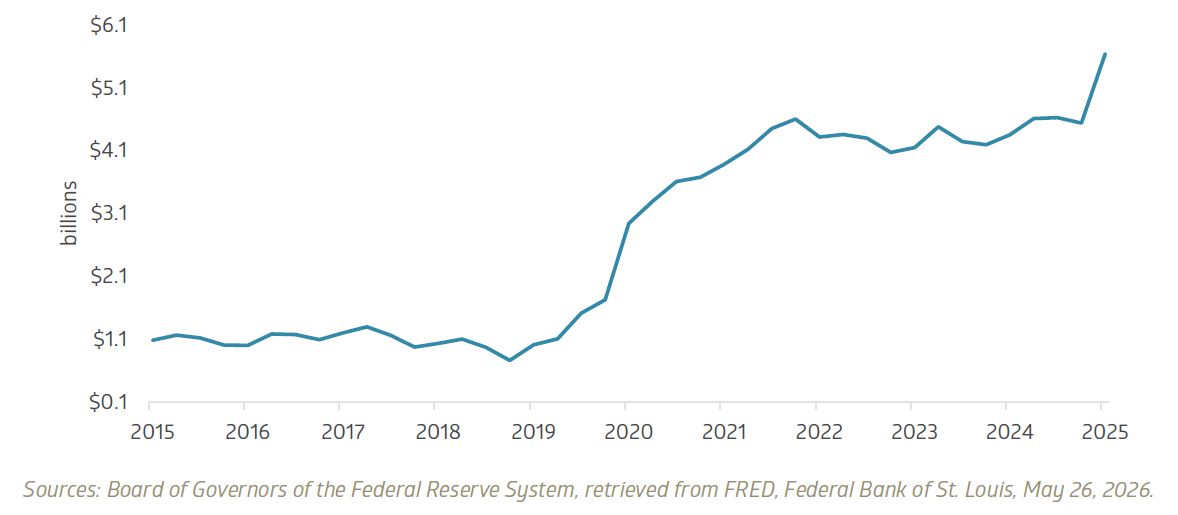

At least in recent periods, the ‘hard’ data has won the day, as soft consumer sentiment has not resulted in a pullback in consumer spending. Encouragingly for investors, we see evidence that households have room to keep spending. Consumer balance sheets continue to look healthy, with a boost from the recent tax refund season, in which the average refund rose 11%. That provided a timely cash infusion as higher gas prices and renewed inflationary pressures threatened real wage growth.

Household checkable deposits remain historically high

Debt service ratios remain well below crisis levels

The offset is the level of consumer debt. The aggregate level of debt continues to receive significant attention in media reports, and for good reason; the total dollar value of consumer debt continues to march higher. However, the ability to service debt levels is a more important measure for evaluating household strain. From that vantage, the data is encouraging, as the share of income devoted to debt payments has been relatively flat and remains well below the over-leveraged period leading up to the Great Financial Crisis. This suggests there is adequate household coverage for current debt levels.

Household debt service as a share of disposable income

We still see reasons for cautious optimism about the health of the U.S. consumer, a critical pillar of the current economic growth regime. We are carefully watching for signs of weakness as the one-time support from the tax rebate stimulus fades and the pain from higher gas prices bites more deeply. But for now, the aggregate story looks resilient.

The kids are (not) alright

While the aggregate consumer data continues to look solid, the averages mask stress beneath the surface. Specific cohorts are showing clear signs of distress. Young Americans, in particular, continue to face a challenging environment.

In past editions of the Morning Macro, we have highlighted elevated unemployment rates among younger demographics, both among college-educated and high school-educated cohorts. Below, we show two graphs of credit stress, broken down by age group. Both show further evidence of stress in this group. Auto-loan balances transitioning to serious delinquency have risen significantly for younger Americans and have yet to normalize. While the aggregate data may not indicate broad weakness, we do see meaningful pressure among younger households with thinner financial cushions.

Auto-loan delinquency rates by age group

Credit-card delinquency rates by age group

Taken together with employment data showing elevated unemployment rates among younger Americans, we see evidence of a generation under pressure. We are also potentially seeing it manifest in unusual ways. There is growing backlash in the younger generation against artificial intelligence and its impact on the labor market, whether real or perceived. Recent news articles have highlighted several commencement speeches in which graduates have booed the mention of AI (see here and here). These graduates are entering adulthood in a world defined by high housing costs, elevated inflation, and uncertain career paths. This is as much a societal issue as an economic one, particularly with elections on the horizon, and its impact may be felt in unpredictable ways. Somewhere out there, the next Steinbeck is penning the modern-day Grapes of Wrath. Hopefully, for history’s sake, without the aid of ChatGPT.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.