From the legacies of iconic investors to the dynamic 2023 markets, Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist, Wealth Management, and Portfolio Manager, Sustainable, Responsible and Impact Investing) presents an insightful perspective on the economic climate, aided by the witticisms of Charlie Munger.

Legendary investor Charlie Munger passed away in late November, just a month shy of reaching the century mark. For 45 years, Munger served as the witty and characteristically caustic partner to Warren Buffett at Berkshire Hathaway. He was a surefire sound bite, adept at delivering zingers with a wry smile while on stage at Berkshire’s annual “Woodstock for Capitalists” shareholder meetings in his hometown of Omaha, Nebraska. Sometimes, he was funny: “Learning from other people’s mistakes is much more pleasant.” Often, he was insightful: “People calculate too much and think too little.” Undeniably, he was practical: “Don’t bail away in a sinking boat if you can swim to one that is seaworthy.” The vast collection of “Mungerisms” captures his concise yet astute speaking style, and lent Munger cult hero status amongst the investment crowd. Long before Twitter’s original 140-character limit, Munger endorsed brevity. In Berkshire’s 2022 letter to shareholders, Buffett acknowledged that “what it takes me a page to explain, (Charlie) sums up in a sentence.”

Legendary investor Charlie Munger passed away in late November, just a month shy of reaching the century mark. For 45 years, Munger served as the witty and characteristically caustic partner to Warren Buffett at Berkshire Hathaway. He was a surefire sound bite, adept at delivering zingers with a wry smile while on stage at Berkshire’s annual “Woodstock for Capitalists” shareholder meetings in his hometown of Omaha, Nebraska. Sometimes, he was funny: “Learning from other people’s mistakes is much more pleasant.” Often, he was insightful: “People calculate too much and think too little.” Undeniably, he was practical: “Don’t bail away in a sinking boat if you can swim to one that is seaworthy.” The vast collection of “Mungerisms” captures his concise yet astute speaking style, and lent Munger cult hero status amongst the investment crowd. Long before Twitter’s original 140-character limit, Munger endorsed brevity. In Berkshire’s 2022 letter to shareholders, Buffett acknowledged that “what it takes me a page to explain, (Charlie) sums up in a sentence.”

Munger liked to keep things simple. In fact, his favorite tool to tackle thorny issues was the humble checklist: “I’m a great believer in solving hard problems by using a checklist. You need to get all the likely and unlikely answers before you; otherwise, it’s easy to miss something important.” The checklist method was no guarantee of cracking the case, however. Munger said that if they lacked special insight into a company, they would set the investment aside as “too tough” and move on. Acknowledging one’s limitations is an important trait, something Munger referred to as staying within their circle of competence. However, both Buffett and Munger admitted they missed their share of investment opportunities this way, notably, in the technology sector. Further, the duo faulted themselves for “mistakes of omission,” where they failed to invest in a company such as Wal-Mart despite having a solid understanding of the business. Those called strikes didn’t hurt too badly: a $1,000 investment in Berkshire Hathaway made at the end of 1978 was worth nearly $3 million by year-end 2022.

It could be said that the hallowed performance track record assembled by the Oracles of Omaha was one percent inspiration, and ninety-nine percent contemplation. Both Munger and Buffett spent countless hours reading and thinking, and comparatively few hours taking action. Buffett reportedly playfully referred to Munger as “The Abominable No-Man” because Munger so frequently turned down potential investments. When they did decide to invest, it was typically in a big way, either buying a business outright or taking a significant stake in the company. Berkshire spent $1.3 billion buying shares of Coca-Cola several decades ago, and in 2022 received dividend payments of $704 million on their shares, which had by then appreciated to a $25 billion market value. The annual dividend yield calculated on their original cost had ballooned to a gaudy 54% – a testament to time, patience, and the power of dividend growth.

Checking it Twice

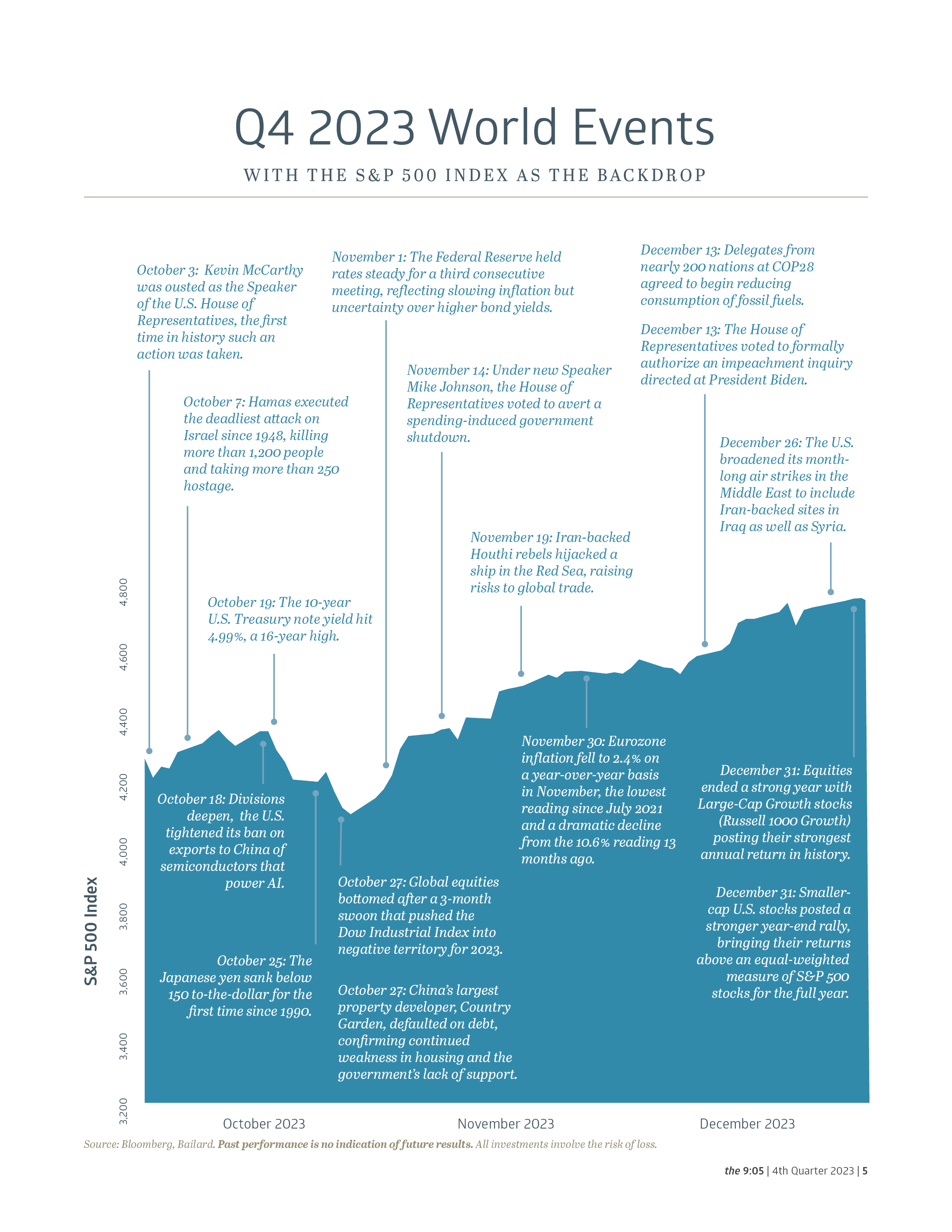

In honor of Charlie Munger, a simple checklist for U.S. equity investors in 2023 is presented at right. Essentially every item broke in favor of equities. First and foremost: inflation. The trend couldn’t have been much more favorable on that front. The Consumer Price Index (CPI) increased a worrisome 6.5% year-over-year in 2022, peaking at a 40-year-high of 9.1% mid-year. By November 2023, the CPI’s growth rate had slowed to 3.1%, within striking distance of the Federal Reserve’s 2% target.

Importantly for consumers (and politicians), the headliners of food and energy prices have improved significantly. Gasoline prices declined nearly 9% year-over-year as of November, while food prices rose just 2.9%. A surge in domestic oil supply helped to dampen energy prices. In fact, U.S. oil production established a new worldwide record of 13.2 million barrels per day in November, surpassing the previous highwater mark set by the U.S. in early 2020. Domestic output—led by shale oil drillers in the Permian Basin of Texas and New Mexico—is so strong that we are exporting as much crude oil, refined products, and natural gas liquids as Saudi Arabia or Russia produces.

The sharp deceleration in the rate of inflation enabled Fed officials at their December meeting to project three Fed Funds rate cuts in 2024 and four more in 2025, suggesting we may have seen the end of the Fed’s rate hiking campaign. This had visions of a soft landing dancing in investor’s heads, that magical scenario in which the Fed is able to quell inflation via higher borrowing rates without incurring a recession. Economist Paul Krugman went so far as to say, “So far, this has been ‘immaculate disinflation,’ requiring neither a recession nor a large rise in unemployment.” While communicating the Fed’s rate decision, chairman Jerome Powell noted that U.S. Gross Domestic Product (GDP) was on track to expand around 2.5% (inflation-adjusted) for 2023 as a whole. As for corporate earnings, the Standard & Poor’s 500 Index is estimated to have generated 8% to 9% growth per share in 2023. In both cases, that growth lands squarely in the sweet spot, neither overheated nor ice cold.

The sharp deceleration in the rate of inflation enabled Fed officials at their December meeting to project three Fed Funds rate cuts in 2024 and four more in 2025, suggesting we may have seen the end of the Fed’s rate hiking campaign. This had visions of a soft landing dancing in investor’s heads, that magical scenario in which the Fed is able to quell inflation via higher borrowing rates without incurring a recession. Economist Paul Krugman went so far as to say, “So far, this has been ‘immaculate disinflation,’ requiring neither a recession nor a large rise in unemployment.” While communicating the Fed’s rate decision, chairman Jerome Powell noted that U.S. Gross Domestic Product (GDP) was on track to expand around 2.5% (inflation-adjusted) for 2023 as a whole. As for corporate earnings, the Standard & Poor’s 500 Index is estimated to have generated 8% to 9% growth per share in 2023. In both cases, that growth lands squarely in the sweet spot, neither overheated nor ice cold.

In retrospect, the “recession that wasn’t” in 2023 failed to materialize primarily due to basic economic bedrocks: the employment and housing markets. Higher interest rates and still elevated inflation did pose challenges, as anticipated, but consumer spending didn’t wither in the face of those headwinds. Personal Consumption Expenditures (PCE) rose 2.7% year-over-year in November, a modest acceleration from the 2% to 2.5% growth range the series registered for much of the year. Consumers enjoyed the stability of a tight job market, with unemployment at just 3.7% in November, and average hourly earnings up 4%, topping the inflation rate. Further, housing prices have absorbed higher mortgage rates without too much trouble. Transactions are down: monthly existing home sales hit a 13-year low in October. Low inventory has aided prices, however. The S&P CoreLogic Case-Shiller National Home Price Index reflected a 4.8% year-over-year gain in October, a ninth-consecutive month of gains and establishing a new record high. The wealth effect theory—that people spend more as the value of their assets rises—seems intact.

Revenge Spend

To paraphrase music superstar Bruno Mars, consumers are dangerous with some money in their pockets. According to a Bloomberg article, Americans continued to splurge in 2023, shelling out for revenge travel, Taylor Swift tickets, and expensive restaurant meals. A lot of it was funded with debt, the article cautions, pushing credit card balances up to $1.08 trillion prior to the holiday season. Delinquency rates are only modestly above pre-pandemic levels, but the average annual percentage rate (APR) has spiked north of 20%, the highest on record. Some have identified a “silent recession” with millions of people struggling to keep up with student loans, car loans, pricey groceries, and higher housing costs. This doesn’t bode particularly well for consumer spending in 2024, although if the current trend of softening interest rates continues the impact could be dampened.

The term “revenge spending” has been around for several years and is commonly defined as elevated spending in the aftermath of a challenging event or time, such as the pandemic. Carnival Corporation has been a somewhat surprising beneficiary of this phenomenon. An early casualty during the pandemic, for obvious reasons, Carnival pulled in record revenues of $21.6 billion in 2023 and has already booked two-thirds of their occupancy for 2024 at “considerably higher prices.” Carnival noted they captured over 3.5 million new-to-cruise guests during 2023. The stock remains well below its pre-pandemic level, despite a 132% rally in 2023, with the company working to pay down its bloated debt load. After peaking north of $36 billion, Carnival has reduced its long-term debt to just above $30 billion, still exceeding its market capitalization of $23 billion. Although Carnival’s debt remains junk-rated by S&P Global, it did receive an upgrade in December by two notches to BB-. The pandemic’s reverberations are still being felt economically, both positively and negatively.

For equity investors, the banner year for U.S. large-cap indices begs the question of how much upside remains at present. The S&P 500 Index concluded 2023 trading at approximately 22x estimated trailing earnings per share, and nearly 20x estimated 2024 earnings. Valuations have been pushed higher in particular by the incredible surge in tech stocks. According to Bernstein Research, 18% of tech stocks now trade at greater than 10x revenues versus a historical average of 6%. At its year-end 2023 level, the S&P 500 arguably has already discounted the positive impact of lower rates in the year ahead, plus the assumed S&P 500 earnings growth of roughly 13%. That said, markets perpetually look forward and will attempt to start pricing in 2025 assumptions as the year progresses.

For equity investors, the banner year for U.S. large-cap indices begs the question of how much upside remains at present. The S&P 500 Index concluded 2023 trading at approximately 22x estimated trailing earnings per share, and nearly 20x estimated 2024 earnings. Valuations have been pushed higher in particular by the incredible surge in tech stocks. According to Bernstein Research, 18% of tech stocks now trade at greater than 10x revenues versus a historical average of 6%. At its year-end 2023 level, the S&P 500 arguably has already discounted the positive impact of lower rates in the year ahead, plus the assumed S&P 500 earnings growth of roughly 13%. That said, markets perpetually look forward and will attempt to start pricing in 2025 assumptions as the year progresses.

If you listen to prominent economist and strategist Ed Yardeni, there is plenty of upside left. His eponymous research firm believes we might be looking at a “Roaring 2020s” scenario, buoyed by wealthy and liquid households, a strong labor market, productivity gains from the ongoing high-tech revolution, and receding inflation, among other factors. An optimistic take, perhaps, but its longer-term focus would be endorsed by Charlie Munger. In his words: “Warren and I don’t focus on the froth of the market. We seek out good long-term investments and stubbornly hold them for a long time.” That approach seemed to work out okay.

1 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 104

2 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 46

3 Berkshire Hathaway 2022 shareholder letter, www.berkshirehathaway.com

4 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 6

5 “The United States is producing more oil than any country in history,” www.cnn.com, 12/19/2023

6 “Inflation, disinflation and vibeflation,” www.nytimes.com, 12/5/2023

7 “’Revenge Spending’ Drives US Credit Card Debt Past $1 Trillion,” www.bloomberg.com, 12/22/2023

8 “Carnival Corporation & PLC Reports Record Fourth Quarter And Full Year Revenues With Continued Strong Bookings And Earnings Momentum,”

www.carnivalcorp.com/investor relations, 12/21/2023

9 “The $19 Trillion Question – What to do with Tech in 2024?”, www.bernsteinresearch.com, 12/18/2023

10 “Ed Yardeni: 12 reasons stock investors will see the S&P 500 hit 5,400 in 2024,” www.marketwatch.com, 12/27/2023

11 Berkshire Hathaway 2022 shareholder letter, www.berkshirehathaway.com

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.