Jon Manchester, CFA, CFP®, Senior Vice President and Portfolio Manager – Sustainable, Responsible and Impact Investing

September 30, 2020

It seems safe to say that 2020 has been a fairly monumental test of our nation’s collective optimism. A bright-eyed view of the world, long seen as an inherently American trait, has faced a torrent of negative news flow this year. The buoyancy meter has mostly ebbed and flowed with the daily COVID case count, amidst a host of other related challenges including high levels of unemployment, social isolation, and— for many—bouts of anxiety. For those in California, another outbreak of wildfires and the resulting poor air quality have cast a sometimes eerie backdrop to the doom-and-gloom delivered via other airwaves.

Dissonance

As November approaches, the presidential election threatens to overshadow all else, a politically fractious, fast-moving current that has stranded many on opposite banks. The passing of Supreme Court Justice Ruth Bader Ginsburg only added to the turmoil. With seemingly everything politicized, and every issue polarizing, it has been difficult to look forward with much of a shared hopefulness.

That is, unless, you happen to invest in stocks. Optimism is readily apparent on Wall Street, and particularly evident in the tech-heavy NASDAQ Composite Index, which posted a cool +25% for the first three quarters of 2020. We know that Wall Street is not Main Street, and that stocks tend to discount the future. Still, the near-relentless rise from the March depths for equities must give even the half-full crowd pause.

Elsewhere, too, are signs that investors are looking past the 2020 wreckage. The U.S. dollar high yield (junk) bond market is expected to set a new annual record for issuance volumes, boosted in part by “fallen angels” or corporate issuers that were investment-grade rated previously. The flood of junk bonds has been met with steady demand, indicating no significant risk aversion. In August, metal packaging company Ball Corp. issued $1.3 billion worth of 10-year bonds at 2.875%, a record-low yield for a junk bond with a maturity of at least five years. Ball originally hoped to borrow (only) $1 billion, but added $300 million to the deal upon receiving strong interest.

With money pouring into growth stocks, junk bonds, and blank-check companies, we might wonder where all the cash is coming from.

Animal spirits are alive and well on the IPO (initial public offering) front as well. September marked the busiest month for IPOs in the New York Stock Exchange’s history, and year-to-date U.S.-listed IPOs have raised nearly $95 billion. That’s not far off from the boom years of 1999 and 2000, with three months to go in 2020. According to The Wall Street Journal, more than 80% of the money raised this year has fallen into three buckets: healthcare, technology, and Special Purpose Acquisition Companies (shell firms set up to acquire private entities and take them public, otherwise known as SPACs or blank-check companies).(1) North of 235 corporations have gone public in the U.S. thus far, on track for the most since 2000.

The Tie that Binds

With money pouring into growth stocks, junk bonds, and blank-check companies, we might wonder where all the cash is coming from. It seems clear that monetary policy has played a big role in all this risk seeking. The Federal Reserve’s (the Fed’s) latest projections indicate they expect to keep the overnight Fed Funds rate near 0% through at least 2023. In August, the Fed announced a landmark shift in its philosophy regarding inflation. The new policy—average inflation targeting—will effectively allow the Fed to let inflation run above its 2% goal for longer stretches, instead of feeling obligated to raise rates. In making the announcement, Fed Chairman Jerome Powell noted “inflation that is persistently too low can pose serious risks to the economy.”

The intent is clear. Within its dual mandate, the Fed will favor maximum employment over price stability for the foreseeable future. This pro-growth stance sends a message to investors, and a long-dated one at that. Further, the Fed’s open-market operations continue, with the tab for their purchases of U.S. securities on the open market currently at $80 billion per month in Treasury securities, plus $40 billion in Agency mortgage-backed securities. As a result, the money supply continues to rise. Per data from the St. Louis Federal Reserve, M2 money stock (a broad measure of ready cash that includes currency in circulation plus checking, savings, money market funds, and small CDs) was up to nearly $19 trillion after starting the year just above $15 trillion. Inflation may follow, although the bond market is not yet convinced. After an initial pop following the Fed’s August policy shift, the 10-year U.S. Treasury breakeven rate (a reflection of the market’s expectation for inflation) retraced back to ~1.6% as of September 30, approximately the same level as prior to the policy change.

Brussels to Beijing

Across the pond, although not in the same category, the European Union (EU) also made waves this summer. In July, the EU agreed on a €750 billion stimulus package, with the debt backed by the EU instead of its individual member countries. It marked the first instance the EU itself issued debt, and prompted some to call it the EU’s “Hamiltonian moment.” Whether this is the start of a new era or simply a one-off response to the COVID crisis remains to be seen. Lehigh University International Relations professor Mary Anne Madeira seemed to indicate the former: “Symbolically, it marks a critical shift in Germany’s willingness to allow the EU to jointly borrow money.”(2)

A late summer surge in COVID cases has put Europe on its heels again, threatening the region’s fragile economic recovery. Weekly cases topped the prior peak level from March, with Spain and France particularly hard hit. This has prompted Spain and some other countries to re-impose restrictions on movement and gathering, albeit of a more targeted and localized nature than the broad lockdowns from earlier this year. In July, citing the economic impacts of lockdown, the EU reduced its Global Domestic Product (GDP) growth estimates for 2020 and 2021, now expecting -8.3% and +5.8%, respectively.

One piece of good news for the EU is the relative health of its second-largest export market: China. Farther along on the COVID recovery curve, China grew its Gross Domestic Product (GDP) by 3.2% in the second quarter. The International Monetary Fund expects China’s real GDP to grow 1% for 2020, versus -4.9% globally. Retail sales returned to pre-coronavirus levels in August, and were up on a year-over-year basis for the first time this year.(3) These positive data points have helped the MSCI China U.S. Dollar Index to a +14.5% price-only return thus far in 2020.

A Digital Divide

Much has been made of the unevenness of the U.S. economic recovery, with some calling it “K-shaped” in which certain sectors or population segments (like Tech or the 1%, respectively) have thrived, while others have lagged including the travel industry and the have-nots to name a precious few. Setting aside the socioeconomic aspects, the pandemic economy has certainly been unsparing to businesses that rely on foot traffic. We might instead refer to the recovery as Amazon-shaped, with that A-to-Z arrow pointing up for e-commerce at the expense of brick-and-mortar retailers.

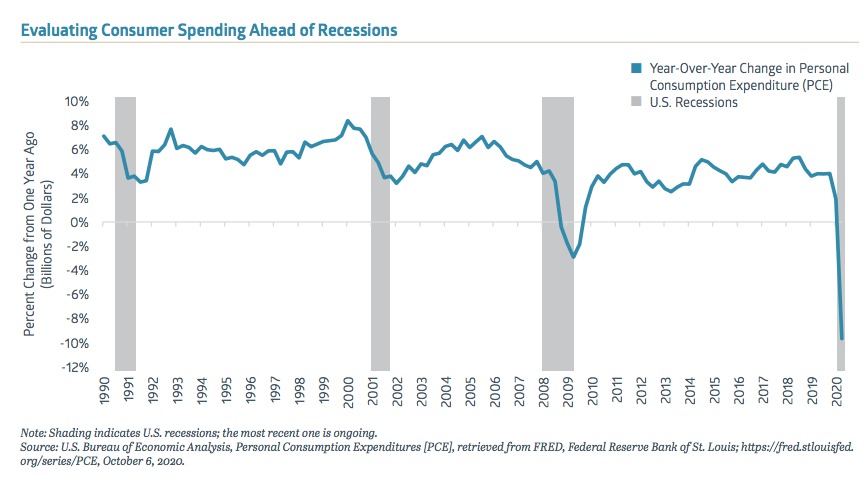

Following a strong recovery in May and June, consumer spending has slowed, advancing +1.5% in July and +1.0% in August. Continued growth is encouraging, although sustained spending is in question with the unemployment rate still elevated at 7.9% in September and additional fiscal stimulus measures in limbo. Recent layoff announcements—such as Walt Disney’s decision to slash 28,000 employees—won’t help. If the economic foundation is to hold and prove the stock market’s optimism correct, U.S. consumers will likely need to play their historic role as savior, not saver.

Following a strong recovery in May and June, consumer spending has slowed, advancing +1.5% in July and +1.0% in August. Continued growth is encouraging, although sustained spending is in question with the unemployment rate still elevated at 7.9% in September and additional fiscal stimulus measures in limbo. Recent layoff announcements—such as Walt Disney’s decision to slash 28,000 employees—won’t help. If the economic foundation is to hold and prove the stock market’s optimism correct, U.S. consumers will likely need to play their historic role as savior, not saver.

Online, the good times largely continue. The Commerce Department reported that non-store retailers (a rough proxy for e-commerce) grew August sales 22% versus the year prior. Companies that combine physical locations with a robust online presence appear to be benefiting as well. Best Buy said their second quarter online revenues soared 242% domestically, while Target reported digital comparable sales growth of 195% for the same period. Even Costco Wholesale, a somewhat reluctant e-commerce participant, noted 91% adjusted growth in that category during their most recent quarter.

Online, the good times largely continue. The Commerce Department reported that non-store retailers (a rough proxy for e-commerce) grew August sales 22% versus the year prior. Companies that combine physical locations with a robust online presence appear to be benefiting as well. Best Buy said their second quarter online revenues soared 242% domestically, while Target reported digital comparable sales growth of 195% for the same period. Even Costco Wholesale, a somewhat reluctant e-commerce participant, noted 91% adjusted growth in that category during their most recent quarter.

The Big Picture

The way we spend is less important in the big picture than simply whether we keep dollars circulating throughout the economy. For those fortunate enough to own a house and have a stock portfolio—key inputs of the wealth effect—spending power should be strong. Equities have regained their mojo, and more time at home has spurred a considerable amount of residential expenditures. The S&P CoreLogic CaseShiller U.S. National Home Price NSA Index rose at a +4.8% year-over-year rate in July, and the Commerce Department recently reported that August new home sales were at their highest monthly level since September 2006.

October marks, at a minimum, the eighth month in the U.S. living with this pandemic. Another flu season approaches and economic activity will continue to depend heavily upon progress in the COVID fight. With great uncertainty and political upheaval ahead, we may need to draw on our optimism reserves. Faith in the future is not our only tool. The adaptability and ingenuity of humans can see us through this challenge, and hopefully, to some greater degree of normalcy.

1 “IPO Market Parties Like It’s 1999,” wsj.com, 9/25/2020.

1 “IPO Market Parties Like It’s 1999,” wsj.com, 9/25/2020.

2 “What Alexander Hamilton has to do with the EU’s $850 billion coronavirus stimulus plan,” vox.com, 7/21/2020.

3 “China’s Economic Recovery Helps Drive Its Stocks Higher,” wsj.com, 10/4/2020.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.