Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy costs and a cooling-but-steady labor market

Dave Harrison Smith, CFA

Chief Investment Officer

April 6, 2026

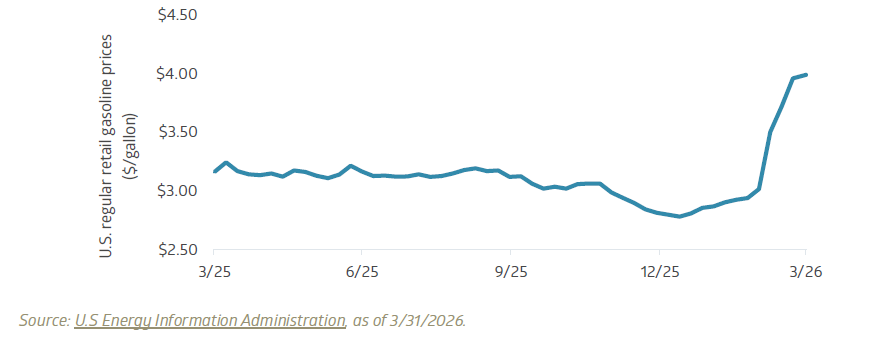

Energy prices and consumer squeeze

Gas prices are moving higher again today. This has been one of the clearest transmission channels from the war in Iran into US markets. The surge in March saw gas prices rise from a national average of $2.94 to $3.99. This five-week move represented a 35.9% increase, the largest five-week increase since the Energy Administration Agency began tracking the data in 1991. Price pressures have continued into April, further compounding this move.

Average national retail gasoline prices, regular blend

Consumer response to higher gas prices is a well-studied phenomenon. Studies have found that gas demand itself is relatively inelastic; in non-economist speak, that means consumers do not purchase more/less of a good if the price decreases/increases. Households still need to commute, families need to run errands, and folks still maintain daily routines. Rising gas prices have historically had little impact on driving behavior.

Where adjustment does occur is in the consumption basket, specifically in reduced purchasing behavior for non-discretionary goods. As gas prices rise, it pinches consumer wallets, particularly for lower- and middle-income households. Studies have shown that consumers reallocate spending away from areas such as leisure, out-of-home dining, and retail goods. This can explain some stock reactions in March as gas prices spiked, particularly among companies more exposed to these sectors and among lower-income households.

Consumer and retail spending have been a central pillar of U.S. economic growth over the last decade. The impact of changes in consumer spending can thus have a meaningful effect on growth, with the initial impact likely to be felt in discretionary spending. Further, the rapid shift threatens to dim consumer outlook on finances and erode consumer confidence. Any sustained pressure over a long period of time threatens to become a broader economic headwind.

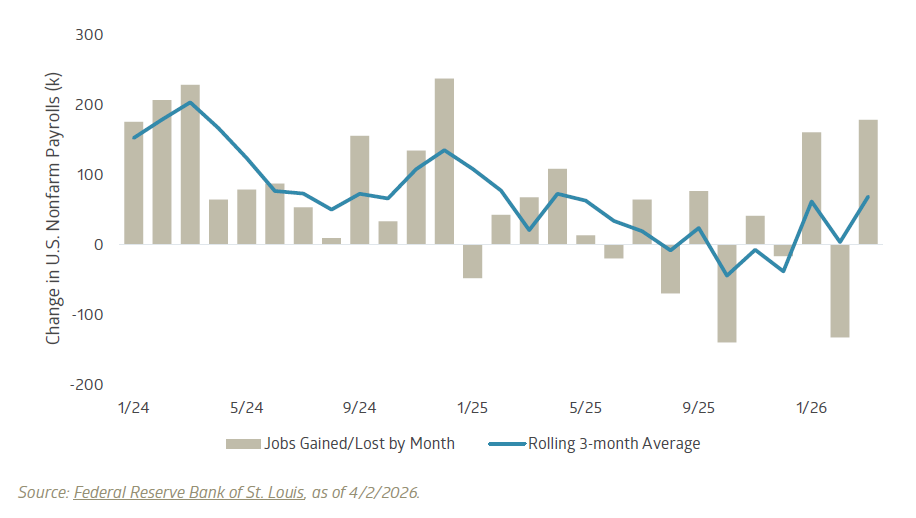

Jobs report: A strong number, though outlook remains uncertain

Last week, we highlighted a key data release: the Bureau of Labor Statistics Nonfarm Payrolls report, which many view as an estimate of net job creation in the U.S economy. February’s print, published in early March, had come in well below expectations, showing a decline of 133 thousand jobs versus expectations of a modest gain. We noted that this was in contrast to several other labor market indicators, such as continuing unemployment claims and private-sector employment estimates, which had indicated greater stability. As a result, we were focused on this data release to confirm or refute the February weakness

The March report surprised to the upside, with payrolls increasing by 178,000 jobs, well ahead of expectations of approximately 60,000.

Broadly, this data reinforces our view that the labor market is cooling but not cracking. The moving three-month average of jobs gained has turned modestly positive after a softer period in the second half of 2025. Importantly, this level of job creation should be consistent with a stable unemployment rate, currently in the low 4% range, particularly in the context of the country’s recent shift to lower net immigration and reduced population growth.

In isolation, this report would be encouraging for the Federal Reserve, suggesting that the labor market remains on solid footing. Yet the background is anything but static, and the high degree of uncertainty stemming from both the war in Iran and rapid advances in artificial intelligence raises the difficulty of forecasting the labor market outlook. Against this context, the takeaway is straightforward: this was a relatively strong report, even if the broader path remains uncertain.

Change in BLS Nonfarm Payrolls by month, rolling 3-month average

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.