Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Beyond the first-day pop

Dave Harrison Smith, CFA

Chief Investment Officer

June 2, 2026

2026 is shaping up to be a banner year for initial public offerings, or IPOs. Few market events capture investor attention quite like a high-profile debut. A long-private company, often benefiting from a powerful secular trend, offers investors their first opportunity to participate through the public markets. The first-day trading pop, the volatility, and the outsized personalities involved all make for a compelling story.

The investment track record is more complicated.

Jay Ritter, a finance professor at the University of Florida and a leading authority on IPOs, has spent decades studying IPO performance. His research consistently finds that IPOs often generate strong first-day returns, but those gains primarily accrue to investors who receive shares at the offering price, typically large institutions and company insiders.

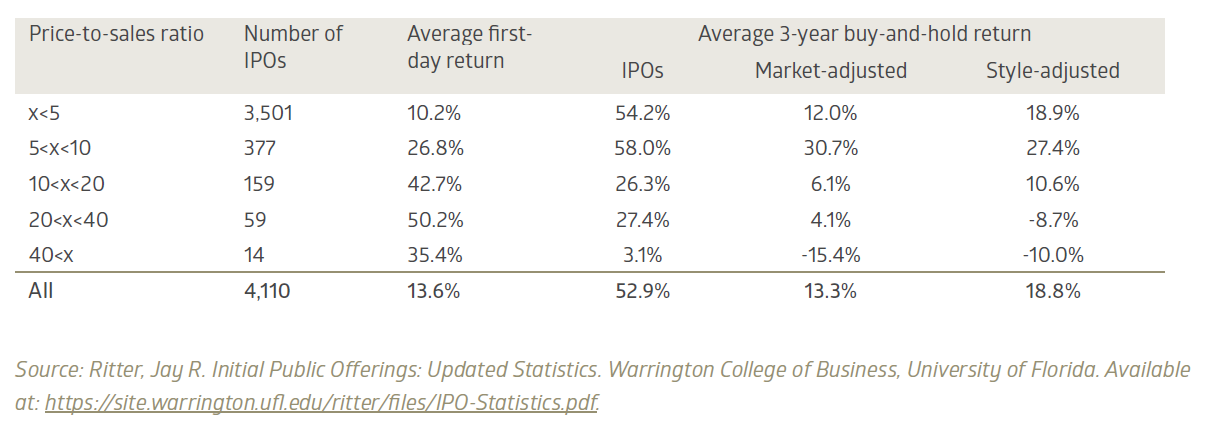

Beyond that initial bump, the historical record becomes far less compelling. From 1980 through 2023, excluding the technology bubble and subsequent collapse, Ritter found that the average three-year buy-and-hold return from the first closing market price was just 26.8%. That trailed the broader market by 19.0 percentage points. Put differently, investors would have been better served owning the broad market than chasing the average IPO.

The averages also hide substantial dispersion. Notably, Ritter’s work has shown stark differences in historical returns by valuation, with expensive IPOs performing especially poorly. In Dr. Ritter’s data, IPOs with a price-to-sales ratio above 40x underperformed the market by an average of 15.4% over three years, even for investors who purchased at the offer price. Staggeringly, only 3 of the 14 IPOs in this cohort outperformed the market, even if investors were able to secure shares at the offer price. For investors unable to acquire the shares at the offer price and instead purchased at the end of trading on the first day, the returns are even worse: -58.5% versus the broad market over three years.

When valuations get extreme, returns often disappoint

Three-year IPO returns by valuation cohort (1980-2023), measured from the offer price

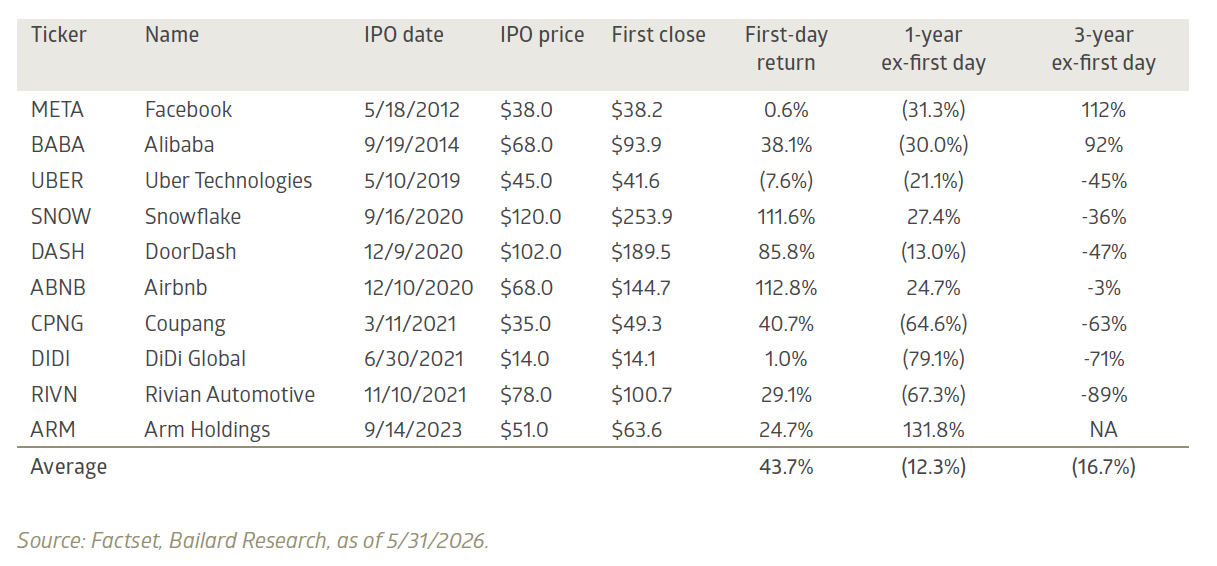

There have been several prominent IPOs in the technology sector over the past fifteen years, including household names like Meta, Airbnb, and DoorDash. The table below highlights 10 of the largest and most notable IPOs over that time period. Notably, the average first-day return is substantial, though outcomes varied widely, with META’s essentially flat first-day return in 2012. Overall, while the group has some success stories, the longer-horizon return data illustrate the challenging investment proposition discussed earlier.

The IPO pop is only the beginning of the story

First-day, one-year, and three-year returns for select technology IPOs (2012-2023)

This does not mean IPOs should be dismissed outright. Some have become extraordinary businesses and exceptional long-term investments. But the IPO market has historically been susceptible to excitement, scarcity, and extrapolation, forces that can overwhelm valuation discipline.

As large IPOs continue to attract investor attention, history argues for selectivity rather than enthusiasm. The lesson is not to avoid IPOs altogether, but to evaluate them with the same rigor applied to any other investment. Our view is that a compelling story may capture investors’ attention, but long-term returns are ultimately determined by business fundamentals and the price paid for them.

.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.