In this quarter’s issue, Lena McQuillen, CFP ®, TPCP®, Director of Financial Planning, shares how claiming decisions shape income over time, especially for a surviving spouse.

Social Security is often treated as a timing decision. Should you claim early, or wait?

That’s part of the decision, but it’s not the whole story. Even for those who may not rely on it, Social Security is one of the few sources of income that lasts for life and adjusts for inflation. How it’s claimed can shape retirement income over many years, particularly for a surviving spouse.

Putting Social Security in perspective

Before getting into the decision itself, it’s worth addressing a common concern.

Social Security is not going away. While the trust fund is projected to be depleted in the early 2030s, that doesn’t mean benefits disappear. Ongoing payroll taxes are expected to continue funding a substantial portion of benefits, currently estimated at roughly 75%, and historically, Congress has stepped in to adjust as needed.

For planning purposes, it’s reasonable to assume Social Security will remain part of the picture.

Framing the trade-off

There isn’t a single right answer here. What makes sense depends on your health, your income needs, and the resources you have available.

Health and family longevity are a natural place to start. If your health is poor or your family history suggests a shorter life expectancy, claiming benefits earlier may make sense. If you’re in good health, delaying benefits can meaningfully increase your monthly income over time. Claiming at age 62 can reduce benefits by up to 30% compared to waiting until full retirement age. On the other side, delaying beyond full retirement age can increase benefits by roughly 8% per year up to age 70.

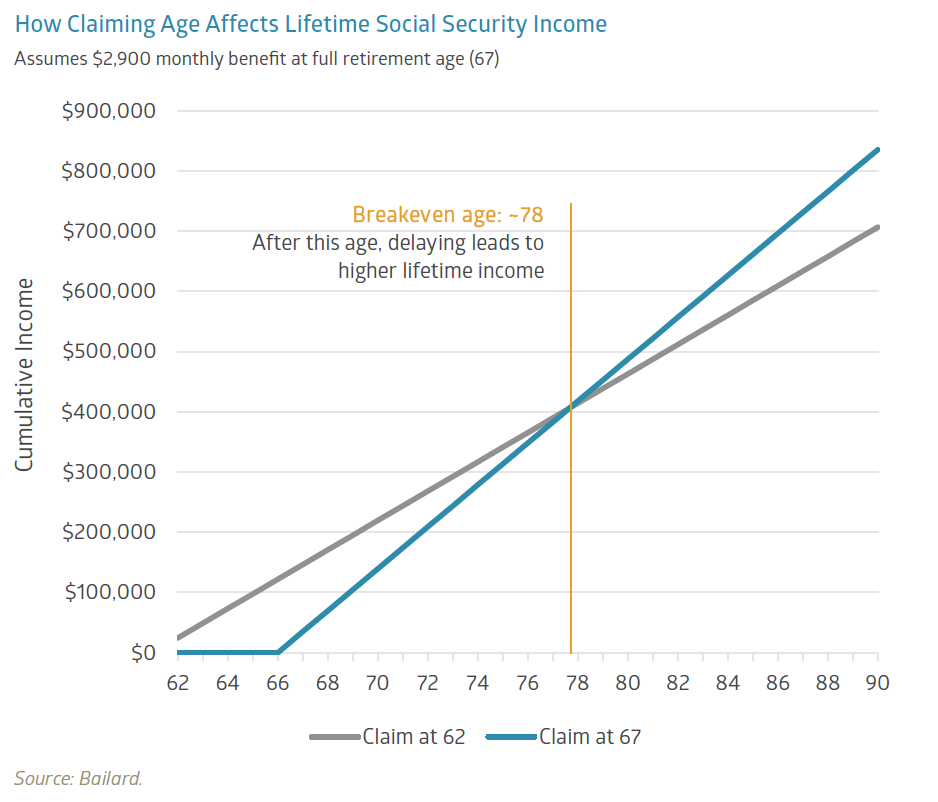

One way to think about this trade-off is through the idea of a “breakeven age,” which compares total benefits over time based on when you claim.

In the example below, the breakeven point falls around age 78. If you live beyond that, waiting typically yields a higher total income. If not, claiming earlier may come out ahead.

The math may be helpful, but it’s only part of the story. It needs to fit within your overall plan, especially in how you’re drawing from other income sources. If you have flexibility early on, whether from taxable investments or retirement accounts, it may be easier to delay Social Security and increase your future benefit. When done thoughtfully, that approach can also help manage taxes and reduce required minimum distributions (RMDs) over time.

For couples

For married couples, the decision isn’t just about one person.

For married couples, the decision isn’t just about one person.

When one spouse has lower lifetime earnings, they may qualify for a spousal benefit of up to 50% of the higher-earner’s primary insurance amount (PIA). At the time of filing, Social Security evaluates both options and pays whichever is higher.

There are a few important nuances. Spousal benefits don’t increase beyond full retirement age, and claiming early reduces both the individual benefit and any spousal supplement.

Survivor benefits are where this becomes especially important. When one spouse passes away, the surviving spouse keeps the higher of the two benefits, including any increase from delayed retirement credits (which increase benefits for each year you wait beyond full retirement age, up to age 70). For many couples, that becomes the income floor on which the surviving spouse lives. When the higher earner delays, they increase their own benefit and, in turn, raise the income that remains in place for the surviving spouse.

Other situations to be aware of

Divorced individuals may also qualify for benefits based on a former spouse’s earnings record.

In general, the marriage must have lasted at least 10 years, the individual must be unmarried and age 62 or older, and their own benefit cannot exceed 50% of the former spouse’s PIA. In some cases, benefits may still be available even if the former spouse has not yet filed, as long as the divorce has been finalized for at least 2 years.

Widowed individuals may be eligible for survivor benefits as early as age 60, though those benefits are reduced if claimed before the survivor’s full retirement age. At full retirement age, the full survivor benefit becomes available.

There’s also some flexibility in how benefits are taken. In certain situations, it may make sense to start with a survivor benefit and switch to your own retirement benefit later, or the other way around, depending on which approach leads to higher lifetime income.

Taking a broader view

Social Security is one of the few sources of inflation-adjusted income that lasts for life. That makes it worth thinking about as more than just a timing play.

What matters is how it fits within your broader plan. Health, longevity expectations, income needs, and how your assets work together all play a role. Walking through a few scenarios and seeing how they unfold over time can help bring the right approach into focus.

# # #

Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.