Jamil Harkness, Research and Performance Associate, offers a broad introduction to the potential for attractive investment opportunities in a segment of the multifamily property type that Bailard defines as “Attainable A.”

The Bailard real estate team has long believed in the advantages of investing in multifamily properties, mainly for the consistent cash flow, manageable volatility, lower capital intensity, and the asset type’s ability to adjust to broader economic conditions more quickly.

Supply & Demand

In the largest 40 U.S. metropolitan areas, roughly one-third or 4.5 million units of the multifamily housing inventory (defined as apartment complexes of 20 or more units) comprise Class A units. Within this category, the more expensive “trophy luxury A” and “luxury A” tiers represent 11% and 52%, respectively. The lower-cost end of the Class A spectrum, the remaining 37%, represents what the Bailard team defines as “Attainable A” properties.

According to CoStar, multifamily supply and demand dynamics at the end of 2022 favored Attainable A properties. As a result, despite a general slowdown in demand across all segments and geographies in the past year, the vacancy rate for Attainable A only increased by 1%, reaching 6.4% by year-end 2022. In contrast, the vacancy rate for trophy luxury A and luxury A properties increased by 1.2% and 1.1%, respectively, ending the year at 8.7% and 9.2%.

Rents for Attainable A increased 3% year-over-year in 2022, with the average asking rent for all unit types within this segment reaching $1,726 per month. Comparatively, average asking rents for trophy luxury A and luxury A reached $3,425 and $2,250 per month, respectively: rent growth of 2.6% and 2.3%, substantially lagging Attainable A.

Defining Attainable A

The Bailard Real Estate team defines Attainable A as high-quality, well-amenitized, recent-vintage, moderately priced multifamily properties generally located in close-in and first-ring suburban markets. Attainable A differs from trophy luxury A and luxury A in several respects, including design, materials, finishes, amenities, and locational attributes. Exhibit 1 enumerates a variety of features that help frame the similarities and differences of the three Class A apartment segments.

Attainable A multifamily is often a good fit for middle-income “renters-by-necessity.” Pew Research defines middle-income earners as individuals who make between 75% and 170% of the median income. According to the Bureau of Labor Statistics, median income for an individual in 2022 was $54,132. Therefore, target renters for Attainable A are those middle-income earners who have an annual income of $40,600 to $95,000.

Attainable A multifamily is often a good fit for middle-income “renters-by-necessity.” Pew Research defines middle-income earners as individuals who make between 75% and 170% of the median income. According to the Bureau of Labor Statistics, median income for an individual in 2022 was $54,132. Therefore, target renters for Attainable A are those middle-income earners who have an annual income of $40,600 to $95,000.

Middle-income renters account for 54.3% of U.S. renters and the majority fall within the 22 to 45 age group, which comprises Gen Z, Millennials, and Gen X. Almost half, 49.6%, either live alone or with roommates. A sample of the kinds of occupations that provide the foregoing levels of compensation are as follows: carpenters, plumbers, firefighters, police officers, office managers, nurses, teachers, sales associates, marketing managers, surgical technologists, IT professionals, project managers, and real estate agents.

Data obtained from Costar indicates trophy luxury A and luxury A one-bedroom apartments in urban or in-fill neighborhoods average $3,000 and $2,100 per month, respectively, making them unaffordable for most middle-income individuals. However, an Attainable A one-bedroom apartment in a first-ring suburban market rents for approximately $1,440 per month. To qualify using the traditional “35% of salary” rent affordability metric, a $49,000 annual income is needed for Attainable A, while $102,000 and $75,000 per year is the baseline for trophy luxury A and luxury A properties.

The Case for Attainable A

Over the past decade, the 40 largest metropolitan areas have seen completed construction of 2.9 million multifamily units. Class A apartments, across all segments, accounted for 86% of these new deliveries. However, only 587,000 Attainable A apartments were constructed, only a quarter of that large Class A pie slice. Many middle-income Americans are experiencing limited affordable housing options.

Despite the modest number of Attainable A apartments completed in the last ten years, the middle-income renter pool remains sizable. In fact, the proportion of middle-income earners in the U.S. has remained stable at around 51% of all workers, versus 52% in 2012. However, due to employment and population growth, the absolute number of full-time working earners has substantially increased in that same period. According to data from the Census Bureau and Pew Research, across the 40 largest metropolitan areas, 3.5 million new middle-income earners were added to the workforce over the past decade. Given the sheer size of the pool of working adults in the middle-income bracket—which is growing and constantly being refreshed by new (and younger) workers entering the labor force—Attainable A product is an attractive and affordable option.

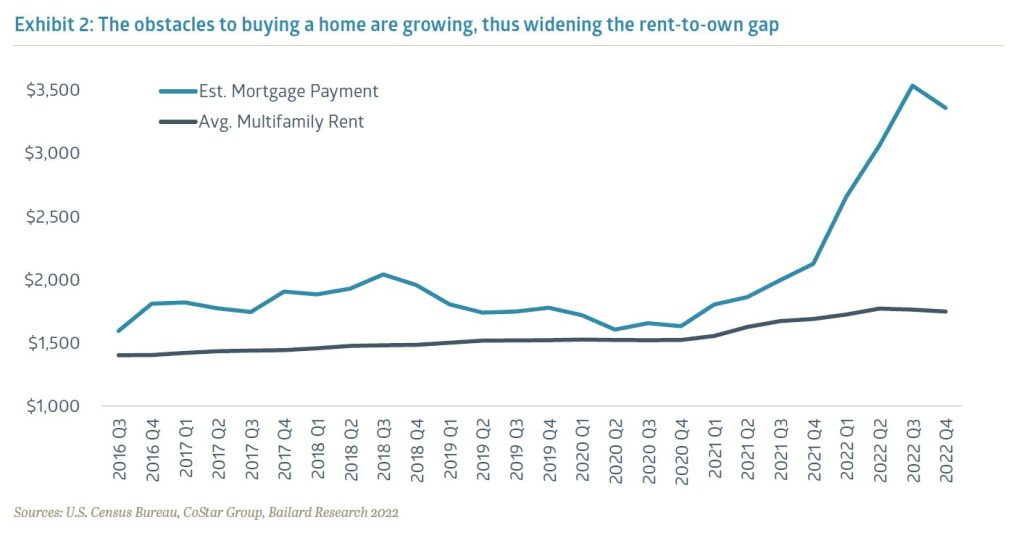

Another crucial factor that has recently expanded the growing renter pool, especially for those in the middle, is the declining affordability of single-family homes. Due to the recent increases in interest rates, the average 30-year mortgage rate reached 6.5% in Q4 2022, up from 2.7% in 2020.1 Average home prices have also increased dramatically (33%) over that same two-year period, from $403,900 to $535,800. Assuming a 90% loan-to-cost, 30-year amortizing mortgage, the average monthly mortgage payment is $1,570 higher than average multifamily rents. The widening rent-to-own gap is illustrated in Exhibit 2; the pool of renters is expanding beyond middle-income earners to higher-income earners who may have previously considered buying a home, but can no longer afford to do so.

Although the investment case for Attainable A is strong, several factors limit additions to supply. First, homeowners generally fear that multifamily developments could bring undesirable impacts (i.e., traffic, congestion, strain on public services, etc.) and potentially depress surrounding property values. This can result in significant public opposition and/or more regulatory burdens that prevent building new apartments, often in areas that need them. Additionally, it should come as no surprise that elevated construction costs—due to inflated commodity prices, higher labor costs, increased costs for planning, permitting and approvals, and the higher cost of capital—can stand in the way of new multifamily development. According to CBRE Research, construction costs increased by 14.5% in 2022 (vs. 2.8% per year average in the prior ten years).2

Although the investment case for Attainable A is strong, several factors limit additions to supply. First, homeowners generally fear that multifamily developments could bring undesirable impacts (i.e., traffic, congestion, strain on public services, etc.) and potentially depress surrounding property values. This can result in significant public opposition and/or more regulatory burdens that prevent building new apartments, often in areas that need them. Additionally, it should come as no surprise that elevated construction costs—due to inflated commodity prices, higher labor costs, increased costs for planning, permitting and approvals, and the higher cost of capital—can stand in the way of new multifamily development. According to CBRE Research, construction costs increased by 14.5% in 2022 (vs. 2.8% per year average in the prior ten years).2

Beyond that, local zoning regulations remain resistant to new multifamily projects in favor of single-family housing in nearly every state nationwide. And, last but not least, labor availability has the potential to curtail housing development generally, particularly multifamily construction, as the workforce is not expanding at the rate necessary to meet demand.

Conclusion

Attainable A multifamily properties offer good value within the Class A universe, providing high-quality residential options to millions of renters who either cannot afford, or do not wish to live in, trophy luxury A or luxury A apartments. The Attainable A product segment is well positioned to continue to be a strong performer due to population/demographic trends, favorable supply/demand dynamics, and the unfavorable affordability challenges for single-family home ownership. And, given the expected growth of the target renter pool across the country for the foreseeable future, the need for housing, especially affordable housing, is more acute than ever.

1 https://fred.stlouisfed.org/series/ASPNHSUS , https://fred.stlouisfed.org/series/MORTGAGE30US, CBRE-EA

2 CBRE-EA: Construction Costs Trends, Released November 2022

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.