Bailard’s financial planning and tax strategy teams help make sense of the One Big Beautiful Bill Act, so you can plan confidently for what lies ahead.*

As 2025 comes to a close…

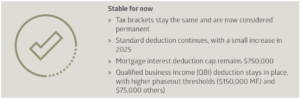

Year-end planning takes on added importance with the passage of the One Big Beautiful Bill Act (OBBBA). This sweeping legislation brings both clarity and complexity to the tax landscape, introducing notable changes while leaving other familiar provisions intact. With some rules already in effect and others beginning in 2026, now is the time to take stock and ensure your financial plan remains well positioned.

Here’s a high-level overview of what’s changed—and what hasn’t—under the OBBBA, in three timely themes to consider before December 31:

- Accelerate charitable giving

- Leverage the expanded SALT deduction

- Consider Roth conversions

1) Accelerate charitable giving before the new AGI floor

For many families, charitable giving is both a personal priority and a key planning tool. Beginning in 2026, charitable contributions for those who itemize deductions will only be deductible to the extent they exceed 0.5% of adjusted gross income (AGI).

While that may sound modest, it adds another hurdle for higher earners who regularly itemize. The good news: for 2025, gifts remain fully deductible up to current limits without the AGI floor. That makes this year a smart time to “lump” several years’ of donations into 2025. Doing so can help maximize deductions under today’s rules and reduce taxable income more effectively than spreading gifts across future years.

A donor advised fund (DAF) can make this easier. It allows you to make a larger, deductible contribution now while granting to charities gradually over time.

» Here’s how it works:

A high-income earner with $1,000,000 of AGI who typically donates $50,000 each year will, starting in 2026, only be able to deduct the portion exceeding $5,000 (0.5% of AGI). Their $50,000 annual gift would yield only a $45,000 deduction going forward.

By instead contributing three years’ worth of giving ($150,000) to a DAF in 2025, they can take the full deduction this year—without the AGI floor—and still direct $50,000 per year to their chosen causes. They’ve captured a larger deduction upfront, and likely lowered their 2025 tax bill in a meaningful way.

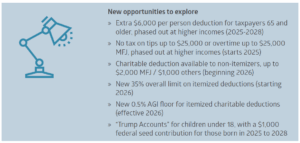

While itemizers face the new AGI floor starting in 2026, non-itemizers will gain a new opportunity to deduct up to $1,000 ($2,000 for married couples filing jointly, or MFJ) of charitable giving on cash contributions. Donations to a DAF or private foundation will not be eligible for this new deduction. It’s a small but welcome benefit for those who take the standard deduction.

2) Leverage the expanded state and local taxes (SALT) deduction

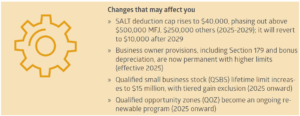

One of the more notable OBBBA provisions is the temporary expansion of the state and local tax deduction cap. For tax years 2025 through 2029, the cap increases from $10,000 to $40,000 for both single and joint filers who itemize.

However, this benefit begins to phase out at $500,000 of AGI and fully reverts to the $10,000 limit once income reaches $600,000 or more. After 2029, the $10,000 cap returns unless further legislation is passed.

The higher SALT cap could make itemizing more attractive, especially for those living in high-tax states with sizable income and property tax bills. But it’s not just high earners who should take notice. Many households have defaulted to taking the standard deduction in recent years (currently $15,750 for single filers and $31,500 for MFJ), yet the higher SALT limit could make itemizing worthwhile again.

» Planning strategies if you’re near the phaseout:

If your income falls near the $500,000 to $600,000 phaseout range, there are ways to remain eligible for the full deduction this year and beyond:

- Defer income such as bonuses or business earnings into the following year

- Maximize pre-tax contributions to 401(k), 403(b), HSA, and similar employer retirement plans

- Use qualified charitable distributions (QCDs) if you’re subject to required minimum distributions (RMDs). QCDs allow you to donate up to $108,000 per year directly from an IRA to a qualified charity, satisfying all or part of your RMD while reducing AGI

3) Consider Roth conversions wile rates remain low

While the OBBBA makes today’s tax brackets “permanent,” that doesn’t mean they’ll stay that way. For now, rates remain historically low, offering an opportunity for proactive long-term tax planning.

For individuals with significant pre-tax retirement savings in traditional IRAs or 401(k)s, Roth conversions can be a powerful way to manage future taxes. RMDs can substantially increase taxable income once they begin, potentially pushing retirees into higher tax brackets, even under current rates.

The years between retirement and the start of RMDs or Social Security often present a valuable window. Many retirees fall into a lower tax bracket than during their working years, or after RMDs begin. That gap creates an opportunity to convert pre-tax retirement assets to Roth accounts, recognizing income at lower rates now to avoid higher rates later.

» Why Roth conversions can help:

- Qualified Roth withdrawals are tax-free in retirement

- Roth accounts aren’t subject to future RMDs, which allows longer tax-free growth

- Conversions may help offset potential tax increases after 2025, particularly for those expecting higher future income or estate tax exposure

If you’re nearing retirement or already retired but not yet taking Social Security or RMDs, consider whether a Roth conversion makes sense. Today’s low tax rates won’t last indefinitely, and acting now could make a lasting difference over time. Taking time to plan ahead now can make future withdrawals, and your overall tax picture, far more manageable.

Let’s make the most of 2025’s planning opportunities

The OBBBA has ushered in both new opportunities and new complexities in tax planning. Perhaps the clearest takeaway is this: AGI matters more than ever. From the new charitable giving floor to the expanded SALT deduction, many of the law’s most impactful provisions hinge directly on income thresholds.

That makes 2025 a pivotal year to manage income and deductions with care. Coordinating charitable giving, income timing, and retirement strategies can help keep your plan aligned with your goals while maintaining flexibility for what’s ahead.

Every household’s situation is unique, but preparation and foresight go a long way. A steady approach, informed by thoughtful planning, can help you feel confident that you’re well-positioned for what’s ahead.

Let’s talk.

OBBBA Snapshot: What’s changed and what’s new?

* Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.