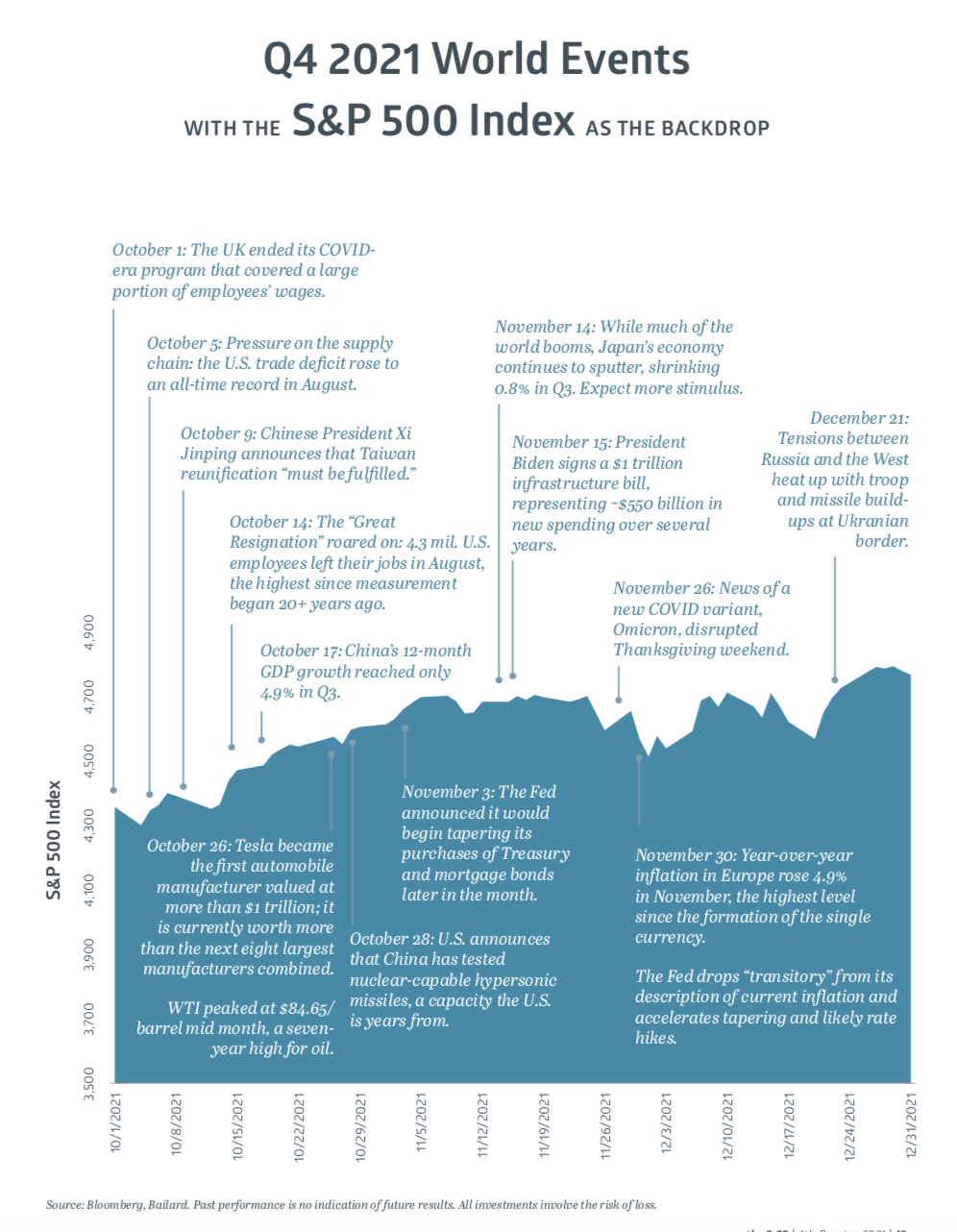

As we tread into the new year, Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) delves into the current trends with a caution to ‘expect the unexpected.’

December 31, 2021

If history rhymes, but doesn’t repeat, there were some distinct notes of the 1980s in last year’s manic markets. For one, a central figure of the 1980s—disgraced junk bond king Michael Milken—was back on the scene, at least indirectly. Pardoned by former President Trump, Milken remains banned from working in the securities industry, but according to Forbes magazine is a “whale” among SPAC [Special Purpose Acquisition Company] investors with interests in 125 separate SPAC’s. (1) Milken’s former family office, now Silver Rock Financial, is reportedly a key member of the “SPAC Mafia,” a group of hedge funds who have thirstily embraced what Forbes reports are “no risk returns” of between 10% and 20%.

In financing SPAC deals—because they have the option to withdraw—the hedge funds are guaranteed to at least get their money back, plus interest, as well as a kicker in the form of low-cost stock warrants. SPACs are set up as a shell company, with the intent to ac- quire a business down the road. They are therefore referred to as blank check companies. For the fat cat hedge funds, it’s a “heads I win, tails you lose” proposition. For the average investor who gets in following the SPAC’s initial public offering (IPO), it’s a much rockier road to riches. Short-seller Carson Block of Muddy Waters Research laid it bare: “A business model that incentivizes promoters to do something – anything – with other people’s money is bound to lead to significant value destruction on occasion.”(2)

A gush of cash poured into SPAC offerings last year, generating roughly $162 billion in gross proceeds, nearly double the 2020 level, which had quintupled versus 2019.(3) With the Federal Reserve continuing to push the easy button on monetary policy, the Milken era “greed is good” ethos seemed to seep into numerous markets. Cryptocurrencies continued their erratic behavior, yet the trend remained higher as inflation fears, blockchain fervor, non-fungible tokens, and good old-fashioned speculation drove the total market capitalization for digital assets north of $3 trillion. Philippe van der Beck, a researcher at the Swiss Finance Institute, noted that without cash flows to forecast, “People are just betting on how they think demand for the asset will change in the future.”(4) In other words, it’s a momentum trade.

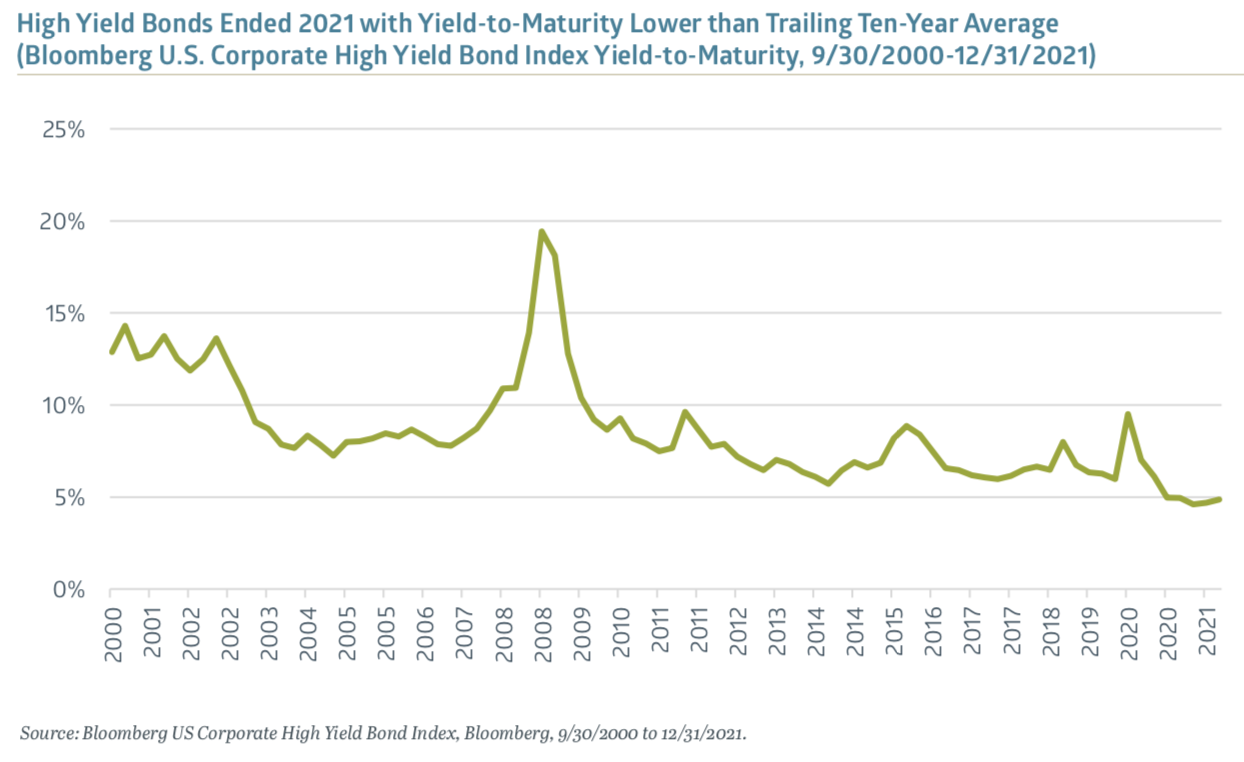

More traditional asset classes were not forgotten: a staggering amount of cash went into equity funds in 2021. Bank of America noted that the more than $1 trillion added to equity funds globally exceeded the cumulative net inflows from the prior two decades!(5) Milken’s old playground, the high yield or junk bond market, showed no lack of resolve. The Bloomberg U.S. Corporate High Yield Bond Index returned 5.3% in 2021, and its yield-to-maturity (YTM) remained comfortably numb to inflation or credit concerns at 4.8%, well below the Index’s 6.6% average YTM over the trailing decade. High yield bonds have been more of a coincident indicator in the past, but at present, there is a “What, me worry?” aspect to junk spreads. In fact, by late November, the U.S. junk bond market had already set a record for annual issuance at more than $455 billion, topping 2020’s record. (6) When you include leveraged loans, more than $1 trillion of high yield debt hit the market, also a high-water mark.

Investors who piled into risky assets were largely re- warded in 2021, although it wasn’t all caviar dreams. IPOs averaged a 10% decline following their trading debut, worst in over a decade. (7) Half of the 28 companies that raised at least $1 billion via an IPO last year traded below their offer price by year-end. Nonetheless, speculation was clearly on the boil with an exceedingly ample supply of money floating around. This fever may extend into 2022 with Fed tightening at a glacial pace, but some caution is warranted, keeping in mind the Warren Buffett adage to be fearful when others are greedy.

Calling all bulls The rise of the retail investor was well-documented last year with Reddit and Robinhood, and the roller coaster rides of meme-stocks such as GameStop and AMC Entertainment after years of torpor. Perhaps an underappreciated part of the story is the method behind the madness: options. Long a domain occupied primarily by professional traders, the options markets have attracted a bevy of retail investors during the pandemic. In 2021, a record (there’s that word again) 39 million options contracts traded daily, on average, up 35% versus 2020. (8) Over 25% of the trading was done by retail investors, and they exhibited a clear preference for buying call options.

Owning a call gives you the right to buy a stock at a stated price within a specific timeframe. For example, if a stock is trading at $50 per share, and you feel it’s worth significantly more, you might buy calls on that company’s shares at $55/share, with the expectation that the stock price will pop prior to the expiration of the options contract. Options are a relatively low-cost way to provide access to a company’s shares and potentially capture upside. Although success requires some luck with timing – unless you happen to coordinate via social media with a lot of other bulls on that same stock (GameStop, e.g.) and end up pushing the price higher unnaturally. Nomura analyst Charlie McElligott commented on this phenomenon: “The fundamentals aren’t the driver. That’s not what matters anymore. It’s the scale and the growth of the options market as this lottery ticket vehicle, which is especially magnified right now because of the retail frenzy.”(9)

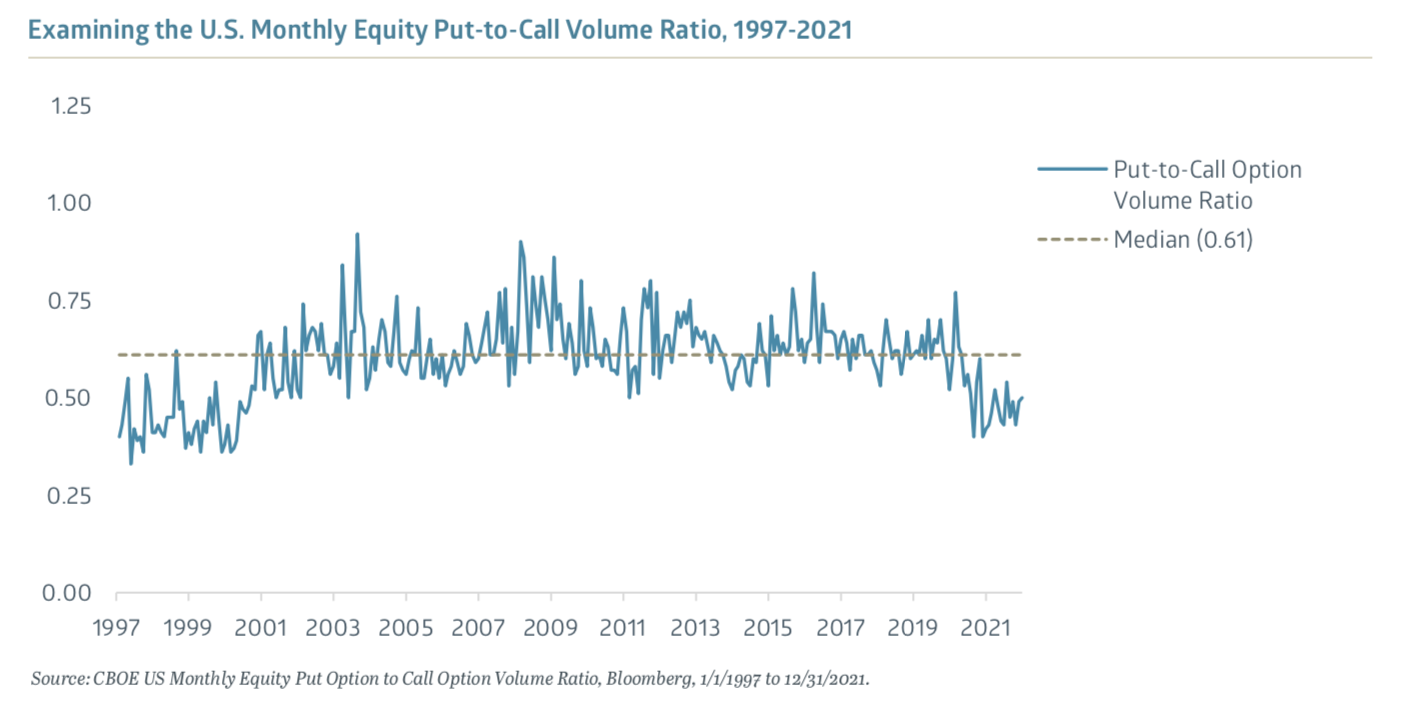

By the end of 2021, the U.S. Monthly Equity Put-to- Call Volume ratio—as reported by the Chicago Board Options Exchange (CBOE)—stood at 0.50, up from a 0.38 low in January 2021. Readings below 0.50 hadn’t been seen since the tail end of the Tech bubble in the late 1990s, suggesting a high level of optimism. This will likely prove a contrarian indicator, although timing is uncertain, as evidenced by the stock market’s very strong 2021 following that January low point for the Put-to-Call ratio. Steven Sears of Options Solutions wrote a piece for Barron’s in which he said the options market has become the biggest casino in the country and warned that “these gambling sideshows tend to end poorly.”(10)

Thread the needle Markets face a difficult task in 2022 following the exuberance of the past 21 months. There are some clear positives, however. Economic growth remains strong, despite the ongoing COVID-19 headwinds and the struggle to stabilize supply chains. The Atlanta Fed’s current estimate of U.S. fourth-quarter 2021 real gross domestic product (GDP) growth is 7.4%, driven by robust consumer spending and higher inventories. For the whole of 2021, the Conference Board estimates 5.6% real GDP growth, which would be the fastest rate since 1984. Looking forward, they peg U.S. real GDP growth at 3.5%, weighed down a bit by another COVID-19 wave, plus persistently high inflation and a more hawkish Federal Reserve.

The outlook for consumer spending is positive, underpinned by gains in both financial and real assets. The S&P CoreLogic Case-Shiller U.S. Home Price Index rose 19% in October on a year-over-year basis. Amazingly, the Index recorded its four highest readings in its 34-year history during the July-to-October 2021 stretch. Warm-weather cities Phoenix, Tampa, and Miami led the way in October amongst the 20- City Composite, with Phoenix atop the charts for 29 straight months! In the press release, S&P reiterated their belief that the housing market’s strength is partly a function of “locational preferences” as households react to the pandemic. The catch for home buyers is that affordability continues to worsen, tempered only marginally by low mortgage rates.

Valuations remain stretched across most markets. Earnings growth for the S&P 500 Index was a bright spot in 2021, with operating profits now projected to have jumped ~65% per share versus 2020. That takes the S&P 500’s trailing price/earnings multiple down to 23.6x, roughly seven points lower than a year ago. Profitability has been impressive in a challenging environment, but the S&P 500 remains historically rich, elevated by lofty prices for growth companies. Strategas Securities calculated that approximately 18% of the Russell 3000 Index was trading at more than 10x sales near year-end, higher than the 14% level of the tech bubble. (11) Earnings will need to meet or preferably exceed expectations for valuations to hold up, particularly if interest rates move higher as projected.

Fiscal and monetary policymakers will attempt a soft landing for the economy and markets amidst a host of inflationary pressures and an unrelenting pandemic. This seems like a big ask, but perhaps taking steps towards normalizing interest rates will tamp down enough inflation and speculation to keep this bull market on track. If the last two years are any indication, expect the unexpected, and hold onto those Miami Vice Ray-Ban sunglasses in case an 80’s party breaks out.

1 “From Junk Bond King to SPAC Whale: How Michael Milken Became A Big Investor In The SPAC Boom,” www.forbes.com, 5/26/2021

2 “What is a SPAC? Explaining one of Wall Street’s hottest trends,” www.cnbc.com, 1/30/2021

3 SPAC Statistics, www.spacinsider.com, 12/31/2021

4 “Behold the Paranoid Style in American Investing,” www.bloomberg.com, 12/22/2021

5 “The $1 trillion that has flowed to global stocks in 2021 is bigger than the last 20 years combined,” www.marketwatch.com, 9/10/2021

6 “High-Yield Bond Sales Soar to Record as Investors Have Few Other Places to Go,” www.wsj.com, 11/26/2021

7 “More Than 1,000 Companies Went Public in 2021, But Returns Are Worst in a Decade,” www.barrons.com, 12/27/2021

8 “Options trading activity hits record powered by retail investors, but most are playing a losing game,” www.cnbc.com, 12/22/2021

9 “How Options Trading Could Be Fueling a Stock Market Bubble,” www.nytimes.com, 1/25/2021

10 “The Options Market Is Now a Casino. Here’s How to Bet Wisely,” www.barrons.com, 12/22/2021

11 “Daily Macro Brief,” Strategas Securities, 12/17/2021

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.