Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Earnings growth is broadening beyond AI

Dave Harrison Smith, CFA

Chief Investment Officer

June 30, 2026

As the first half of 2026 draws to a close, investors have no shortage of competing narratives. Geopolitical turmoil, corporate drama, and artificial intelligence have all seized media and investor attention. To us, one theme stands out from the rest: the strength in corporate earnings. The current earnings boom is unusually robust for this stage of the economic cycle. Current estimates are for aggregate S&P 500 earnings to increase by 25.3% over 2025 levels. That’s the strongest annual growth since the pandemic recovery year of 2021 and is a significant driver of stock returns thus far in 2026.

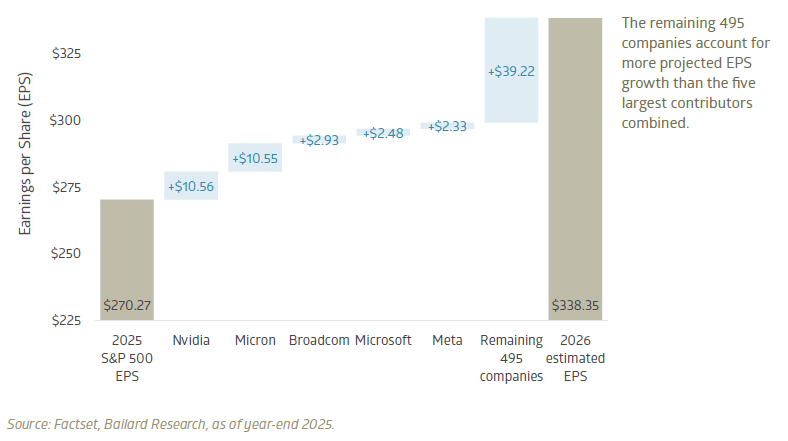

The demand for artificial intelligence infrastructure is a major driver of this growth. Nine of the ten largest contributors to projected earnings growth are technology or technology adjacent companies. The top three are all semiconductors: Nvidia, Micron, and Broadcom. Micron and Nvidia, two of the most notable semiconductor suppliers to AI data centers, alone are expected to account for 31% of the S&P 500’s earnings growth in 2026. This concentration helps explain why the durability of the AI investment cycle is such a critical point for investors.

AI dominates headlines, but earnings growth is becoming more broad-based

That said, the concentration we see does not imply the absence of growth elsewhere. Excluding the top 5 contributors to earnings growth in 2026, the rest of the S&P 500 is still expected to grow 14.6% over last year. That’s a healthy year by historic standards, and modestly above the low double-digit growth rates of 2024 and 2025.

There are also signs of strong growth in smaller companies. Over the next four quarters, analysts expect the median stock in the Russell 3000 index to increase operating income by nearly 10%. That represents an acceleration from the current growth rate of just under 9% and implies broad strength in corporate fundamentals. Certainly, the major beneficiaries of artificial intelligence, particularly semiconductor companies, are major contributors to growth. Yet, the narrative that this strength implies an absence of strength elsewhere in the economy and the market may be misleading.

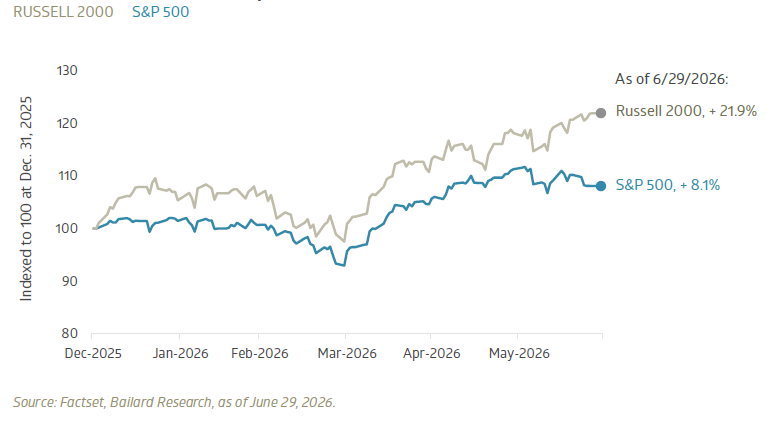

Despite the solid growth outlook, it has been a tumultuous journey for investors so far. The year began with optimism around strengthening economic activity as we moved past the most volatile aspects of the tariff negotiations. The Russell 2000 Index, comprising small- and mid-sized US companies, outperformed strongly as investors eyed a broad group of cyclical and economically sensitive industries. The war in Iran injected uncertainty and commodity price volatility back into the market, and strong earnings from mega-cap and AI beneficiaries drove outperformance in the large-cap S&P 500 index. In recent days, we’ve seen a resurgence of broader market strength, perhaps coinciding with data showing an acceleration in the underlying economy and easing geopolitical tensions.

S&P 500 and Russell 2000 indices, year-to-date total return

The concentration of earnings growth stemming from artificial intelligence remains a genuine risk. The boom in AI infrastructure investment benefits not only the direct supply chain but also a wider ecosystem. A pullback in spending would not only damage the earnings outlook for the direct supply chain but also affect industries such as construction, power generation, and heating and cooling.

This helps explain why the widening participation of growth is so important. The resilience of earnings outside the largest contributors, the strong growth in operating income among median companies, and the outperformance of small-cap stocks all suggest a broadening of corporate fundamental strength beyond the AI theme. Should it continue, it would create a wider opportunity set and create a market environment less dependent on a handful of companies. We consider this to be a critical theme for investors going forward, from both a portfolio risk and an asset allocation standpoint.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.