Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

When good news becomes a problem

Dave Harrison Smith, CFA

Chief Investment Officer

June 9, 2026

Labor market strength complicates the Federal Reserve’s path

Americans remain uneasy about the job market. The constant drumbeat of corporate layoffs, particularly in tech-heavy markets like Silicon Valley, has been compounded by an omnipresent narrative of artificial intelligence-enabled worker replacement. This has created a dour outlook for many consumers and investors. The data, however, tell a slightly brighter story.

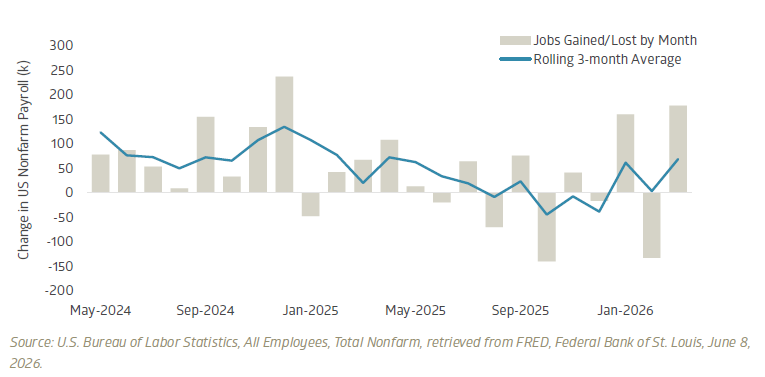

The Bureau of Labor Statistics (BLS) updated its count of nonfarm payrolls through the end of May, and the report was encouraging. Critically, it reinforced a recent pattern of modest re-acceleration in the labor market after stagnant, and in some markets, outright negative job growth in 2025. The start of 2026 has been notably firm, with the most recent three months showing an economy adding at least 172,000 jobs per month. The average gain of 188,000 jobs per month marks the strongest three-month pace of job growth since March 2024, and punctuates steady re-acceleration in the labor market.

Job growth has reaccelerated in 2026

U.S. nonfarm payroll additions, monthly change (thousands), May 2024-May 2026

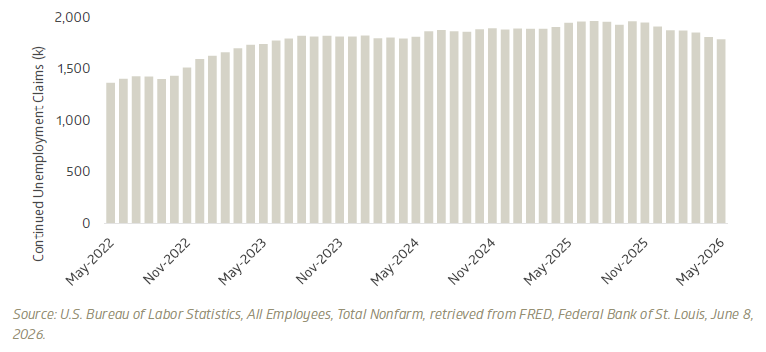

Continued unemployment claims tell a similar story. Claims, a count of Americans who have been jobless for more than one week, have risen steadily over the last several years, though from a small base, while overall unemployment has hovered in the 4% range. More recently, the trend has improved, with continuing unemployment claims falling to levels last seen in April of 2024.

Fewer workers are remaining unemployed

Continued unemployment claims (thousands), May 2022-May 2026

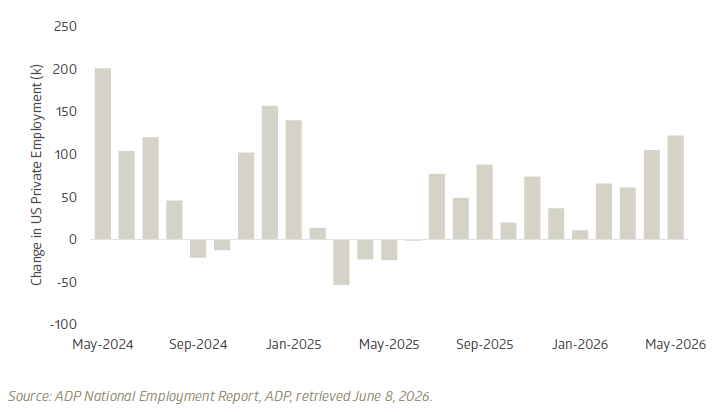

Given growing concern about the accuracy and reliability of government labor statistics from both sides of the aisle, it’s useful to supplement BLS data with private sector measures. ADP’s employment report, which aggregates data from more than 26 million private sector workers in the U.S., provides a useful supplemental check. Encouragingly, this data set also shows a modest re-acceleration off of a challenging 2025, with the recent trend returning to levels last seen in 2024. Job growth has been led by Education and Health Services companies, perhaps reflecting structural demand from our aging society, and a rebound in Information sector jobs. One notable distinction is how job growth differs by company size relative to 2024. In 2024, job growth was broadly distributed across companies of all sizes. 2026, however, has been marked more by strength among the largest, with companies with 500+ employees showing consistent growth, as well as a recent rebound among sub-20-person companies. Mid-sized companies, however, have continued to struggle.

Private sector hiring signals similar improvement

ADP private employment growth, monthly change (thousands), May 2024-May 2026

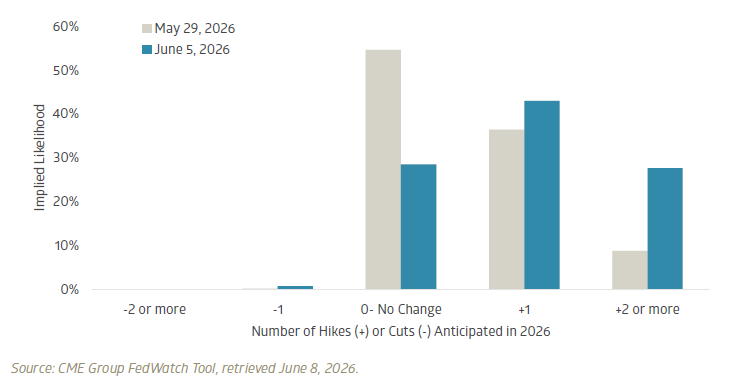

The stock market response to this strong labor market data was decidedly negative, with the S&P 500 down 2.6% and the Nasdaq 4.5% to end the week. The reaction illustrates the challenging nature of making market predictions. A stronger labor market may indicate stability in the U.S. economy, but it paradoxically gives the Federal Reserve more room to focus on taming still-elevated inflation. Futures markets now imply a 69% likelihood of at least one rate hike by year-end, and 26% chance of two or more hikes. This is a significant shift compared to last week, when markets were pricing in nearly even odds of no rate hikes in 2026.

Markets now expect higher rates for longer

Implied Federal Reserve rate changes by year-end 2026, based on futures pricing

For now, it appears we remain in the Goldilocks zone: steady growth, an improving labor market, and strong corporate earnings, without prompting a sharper policy response. The key risk remains inflationary pressure. If inflation becomes too strong for the Federal Reserve’s comfort, its response could be a brake check on economic growth and the business cycle. Labor market stability is good news. Yet in this environment, we are once again reminded how good news can paradoxically create complications for the stock market.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.