Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The end of forward guidance?

Dave Harrison Smith, CFA

Chief Investment Officer

June 23, 2026

For economists, last week was the monetary policy equivalent of a presidential election. For the first time since 2018, a new voice took the helm of the U.S. Federal Reserve (the “Fed”). Kevin Warsh, former Fed governor and, more recently, a lecturer at Stanford Graduate School of Business, officially succeeded Jerome Powell as chair of the Federal Reserve. Warsh wasted little time signaling that some aspects of Fed policymaking may look different under his leadership.

The most immediate changes were in communication. The Federal Open Market Committee’s (FOMC) policy statement, released following the central bank’s meeting, was significantly more concise and removed much of the familiar forward-guidance language. Warsh’s objectives appear more philosophical than stylistic. He has argued that markets can become overly dependent on Federal Reserve guidance, reducing their usefulness as an independent signal of underlying economic conditions. In Warsh’s view, markets function best when they respond to economic data rather than simply reflecting the Fed’s own expectations back to policymakers.

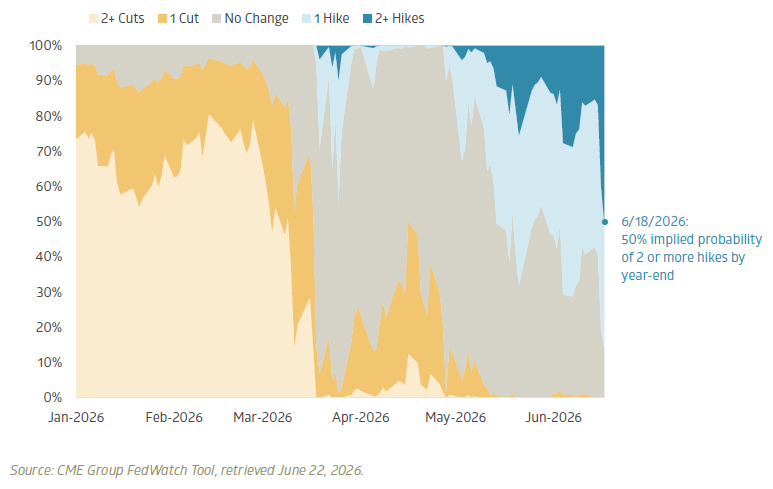

While the statement itself was brief, its closing sentence stood out unambiguously: “The Committee will deliver price stability.” Combined with Warsh’s press conference and the FOMC’s updated projections, markets interpreted the message as a meaningful hawkish policy shift. While the Fed maintained its target range at 3.50% to 3.75%, expectations for additional tightening rose sharply. As of this writing, two or more rate hikes are viewed as the most likely outcome for the remainder of 2026. This marks a dramatic reversal from the start of the year, when investors were confident that the Fed would deliver at least two quarter-point rate cuts.

Fed Funds futures: Expected rate changes through year-end 2026

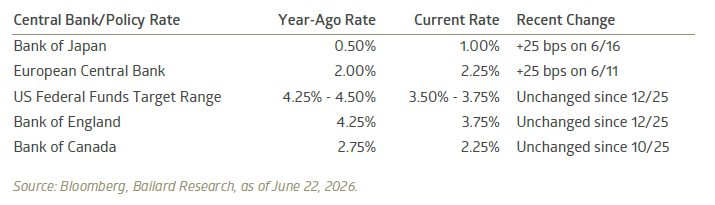

Globally, monetary policy is also tilting toward tighter policy. In June, both the Bank of Japan (BOJ) and the European Central Bank (ECB) raised policy rates by 25 basis points. Investors widely interpreted statements from the BOJ as implying additional rate increases later this year, while recent commentary from ECB policymakers suggested another increase could come as soon as July. Officials from both institutions cited upside inflation pressures as a primary catalyst for further tightening.

Major Central Bank policy rates

The conflict in the Middle East has complicated the policy outlook. Higher energy prices are pushing headline inflation higher and are beginning to filter into other areas of the economy, increasing the risk of second-order inflation effects. We are also seeing a rise in longer-term inflation expectations, a psychological dynamic that can prove difficult to reverse once it becomes embedded. Central banks are increasingly focused on preventing elevated energy prices from altering consumer and business behavior in ways that could sustain above-target inflation for an extended period.

Markets are now pricing in a meaningfully tighter monetary policy backdrop than at the start of the year, and the cushion of lower interest rates many investors expected has largely disappeared. This has important implications for both security selection and asset allocation. We continue to view inflation as one of the most significant risks facing investors today. The backdrop is not necessarily bearish, but it is less forgiving. In our view, inflation expectations remain one of the most important indicators to watch in the months ahead.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.