Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The case for rate cuts gets less urgent

Dave Harrison Smith, CFA

Chief Investment Officer

July 14, 2026

Last week’s release of the June Federal Reserve meeting minutes highlighted an important shift in the balance of risks in the U.S. economy. As recently as the December meeting, the Committee had succinctly stated that “downside risks to employment had risen in recent months,” reflecting rising concern about a prolonged cooling of the U.S. labor market. Today, the picture has markedly improved. By its June meeting, concerns of deterioration had eased with recent data, allowing policymakers to place greater emphasis on elevated inflation and their commitment to price stability.

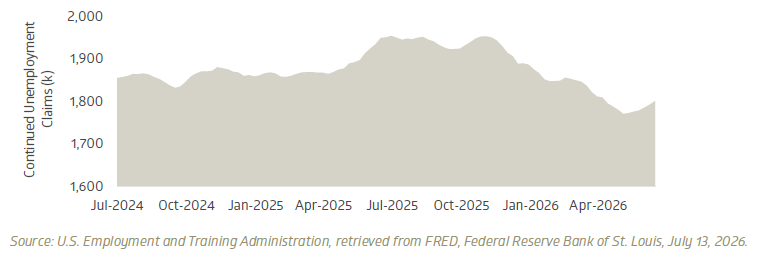

The labor market is not booming, but recent data show encouraging stability. Continued unemployment claims have declined from their late-2025 peak, suggesting fewer American workers are relying on unemployment insurance for extended periods. Similarly, monthly nonfarm payrolls have also posted a string of modest gains, with the moving average recovering considerably from its late-2025 weakness.

Continued claims have eased from their 2025 peak

Four-week moving average, thousands, seasonally adjusted

These gains should be viewed in the context of slower labor-force growth. An aging population and sharply lower net migration mean fewer new jobs are needed each month to keep unemployment stable. Hiring that would have looked weak in prior cycles may therefore be consistent with a balanced labor market today.

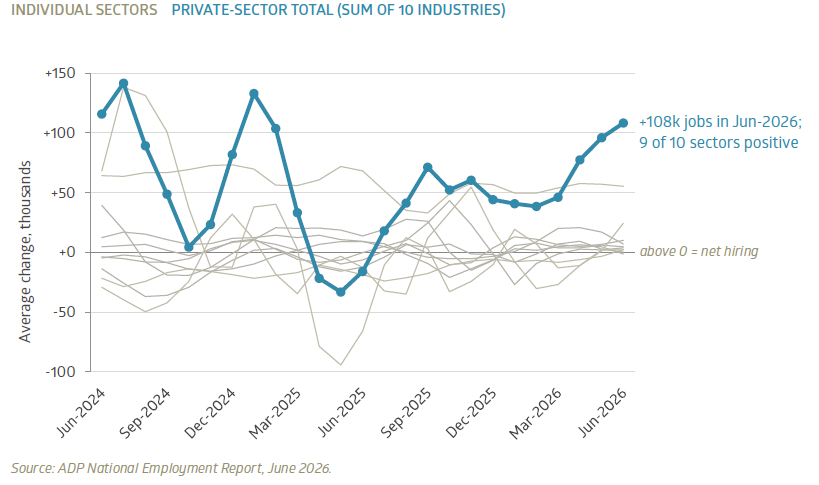

Encouragingly, job growth is also broadening across industries. On a three-month moving-average basis, nine of the ten sectors tracked by the private-sector payroll giant ADP added jobs. As recently as late 2025, more than half of the industries were frequently contracting. The education and health services sector remains the workhorse of the U.S. labor market, as it has been for years. But positive job creation in construction, financial activities, leisure and hospitality, and other sectors has made job creation more resilient and less dependent on a single source.

Most industries are now adding jobs

Three-month average change in private-sector employment, thousands

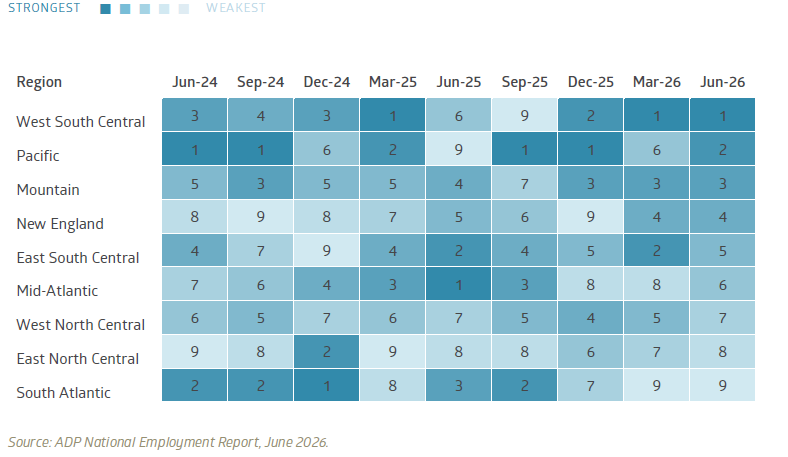

Regional data show a similar rotation in strength. Hiring has improved in the East North Central, New England, and South Atlantic regions, while job growth in the Sun Belt has remained steady. West South Central, which includes Arkansas, Louisiana, Oklahoma, and Texas, has ranked among the strongest regions for much of 2026. The Pacific has shown significant volatility, with growth booms offset by periods of net job loss, coinciding with the early work-from-home days post-pandemic and the widespread tech layoffs in 2023. Most recently, the region surged back near the top of the rankings, likely driven by strong growth in AI-related hiring and investment.

Regional job growth leadership continues to rotate

Rank based on three-month average private-sector job growth

Overall, the U.S. labor market has improved in recent months, both in the pace of job creation and in the breadth of participation across industries and regions. This aligns with data showing a modest acceleration in the underlying economy. The broader base of support is critical because it makes growth less dependent on AI infrastructure and power investment. It also creates a monetary policy tradeoff: a stable labor market reduces the Federal Reserve’s urgency to lower interest rates, shifting attention back toward inflation, geopolitical uncertainty, and the policy implications of the energy market supply shock.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable. Still, its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

The S&P 500 Index measures large-cap U.S. equities; the Russell 1000 Index measures large-cap U.S. equities, with the Russell 1000 Growth and Russell 1000 Value indices measuring the growth and value segments, respectively; the Russell 2000 Index measures small-cap U.S. equities, with the Russell 2000 Growth and Russell 2000 Value indices measuring the growth and value segments, respectively; the S&P MicroCap Index and Russell Microcap Index measure micro-cap U.S. equities; the MSCI EAFE Index measures developed-market equities outside the U.S. and Canada; the MSCI Emerging Markets Index measures emerging-market equities; the Bloomberg U.S. Aggregate Bond Index measures the U.S. investment-grade taxable bond market; the Bloomberg U.S. Treasury Inflation-Linked Bond Index measures U.S. Treasury Inflation-Protected Securities, or TIPS; and the Bloomberg Municipal Bond Index measures the U.S. investment-grade tax-exempt municipal bond market. The U.S. CPI refers to the Consumer Price Index, a measure of inflation based on prices paid by consumers for a representative basket of goods and services.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Recent Insights

Keep Informed

Get the latest News & Insights from the Bailard team delivered to your inbox.