Country Indices Flash Report – January 2026

U.S. asset leadership continued to slide from its early-2025 peak. Gold briefly hit record highs above $5,400/oz as the Fed held rates steady, foreign currencies rallied, and more than 80% of country equity indexes outperformed the U.S. in January. [Read more…]

Quarterly International Equity Strategy Q4 2025

2025 closed by continuing the year’s theme: equity strength driven by economic and corporate resilience, despite policy uncertainty. The U.S.-centered nature of much of this uncertainty gave non-U.S. stocks an edge over U.S. peers for the quarter and year—resulting in the largest annual gap seen in over 30 years. International stocks have shown remarkable breadth—spanning numerous disparate countries, industries, and stocks—in contrast to a narrow U.S. market. A diversity of thematic tailwinds, ranging from AI infrastructure to security spending and improvements in governance, along with undemanding valuations and pressures on the U.S. dollar, support our belief that the year’s strength is just the beginning of a multi-year period of non-U.S. equity leadership.

ComparisonAdviser: "How to Read a Financial Plan as a Client"

Lena McQuillen, CFP®, TPCP®, Vice President & Director of Financial Planning, weighs in on an article published by ComparisonAdviser.

Why International Equities Led Global Markets in 2025

Three Drivers Behind the Rally and the Case for Continued Outperformance in 2026

In contrast to a narrow U.S. market, international equity strength had remarkable geographic and industry breadth.

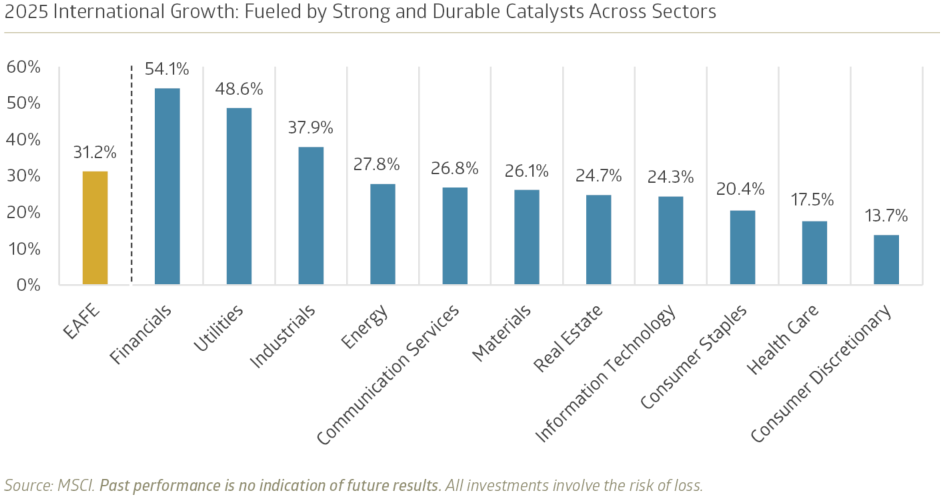

For more than a decade, global portfolios were defined by a singular theme: the undisputed dominance of U.S. equity markets. International markets, tethered by sluggish growth and structural headwinds, largely remained in the shadows. In 2025, however, the tides finally turned. The MSCI EAFE Index surged 31.2% for the year, outperforming the U.S. by a margin not seen since 1993.1

While the U.S. market continued to deliver respectable returns—with the S&P 500 up 17.9% for the year—its performance remained precariously concentrated on a narrowing cohort of mega-cap technology names. By contrast, the rally in international markets has been defined by its extraordinary breadth.

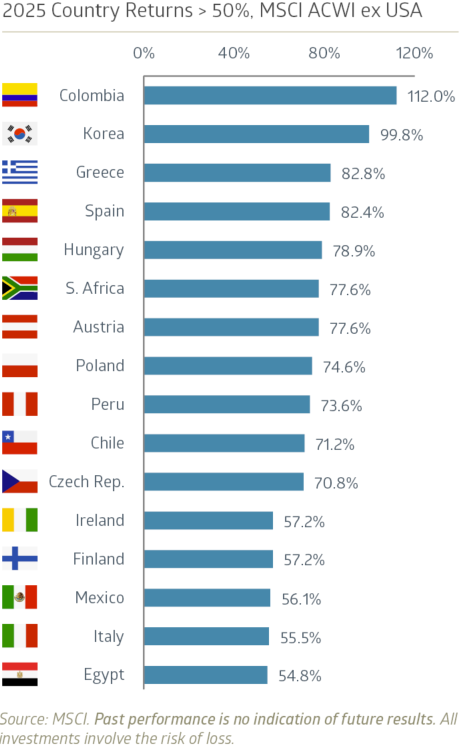

Over one-third of MSCI ACWI ex USA constituent countries (16 of 46) posted returns exceeding 50% in 2025, a level of widespread global growth reminiscent of the 2009 post-crisis recovery. Conversely, only 6 ACWI ex USA nations sat in negative territory. Sector diversity further underscores this health. Growth was powered by a diverse set of catalysts across the globe rather than a single sector; every EAFE sector was up at least 13%, with Financials, Utilities, and Industrials outperforming the broader index. Notably, Technology—the historical engine of U.S. returns—was up a relatively modest 24% in EAFE, signaling that the international rally is built on a much more durable, eight-cylinder engine.

So what fueled that horsepower? Notable drivers behind international equities’ 2025 performance included lasting structural reforms, policy shifts, and secular growth themes. This was most powerfully illustrated by aggressive governance reforms in South Korea, a long-awaited structural recovery in Southern Europe, and a secular boom in global defense. Because these are enduring changes rather than fleeting cyclical blips, we believe this leadership rotation is in its early stages and will likely continue to drive strong international performance through at least 2026.

South Korea: Dismantling the “Korea Discount”

South Korea has emerged as the undisputed standout in the Asia-Pacific region, soaring 99.8% for the year. This outperformance was the result of a powerful convergence between secular AI-driven growth, improved U.S.-Korea trade relations, and shareholder-friendly policy shifts.

The Infrastructure of Intelligence

As U.S. tech giants focus on developing cutting-edge AI software and models, and driving a massive buildout of data centers, Korean firms provide critical hardware infrastructure. Fueled by demand for high-bandwidth memory chips, Samsung Electronics and SK Hynix—which together represent nearly half of the country’s index—contributed 58% of Korea’s total returns in 2025.2 This AI play has been bolstered by favorable trade agreements with the U.S., involving deep investment commitments in defense and shipbuilding, as well as a relaxation of restrictions on nuclear development.

Shareholder-Focused Policy Shifts

The government’s “Value-Up Program” emphasizes corporate governance and capital efficiency in an effort to address the “Korea Discount” and boost the valuations of domestic listed companies. With policy changes well underway, the program has already seen positive impacts and a shift in the investment case for Korean equities.

- Tax Reform: The reduction of the dividend income tax (capping the rate at 30% for high-payout firms, down from 49.5%) has unlocked trapped capital.

- Treasury Mandates: Proposals to mandate cancellation of treasury shares within one year of a buyback are ending the practice of “hoarding” shares to protect family control, forcing capital back to shareholders.

- Governance: Stricter minority shareholder rights and caps on majority voting for audit committees have fundamentally changed the risk profile for foreign investors.

This shift has ignited numerous industries. Hyundai Rotem (Defense) rallied 272%, while Doosan Enerbility (Nuclear) surged 329%. Major financials like KB and Shinhan are no longer value traps, but vehicles for capital return.

Spain: A Decade of Discipline Pays Off

In Europe, Spain delivered its best equity performance in decades, up 82.4% for the year. This rally was powered by its banking sector, which constituted almost 50% of the benchmark at 2025’s end. Heavyweights Banco Santander (+164%) and BBVA (Banco Bilbao Vizcaya Argentaria +154%) acted as the primary engines of growth.

This is not a speculative bubble, but the payoff of a decade-long austerity and deleveraging cycle. Since the Eurozone crisis, Spanish corporates and households have spent ten years cleaning up balance sheets and are now primed to re-lever as European Central Bank rates declined from 4.5% to 2.0%. Consequently, in 2025, we reached an inflection point where lending growth finally began to outpace GDP growth.

Critics point out that valuations are no longer cheap; for example the ‘EURO STOXX Banks Index (SX7E) forward price-earnings ratio is at a slight premium to its 10-year average. But comparing today’s overcapitalized, streamlined banks to the distressed banks of a post-Global Financial Crisis Europe is like comparing apples and oranges. With sector consolidation and expected deregulation providing tailwinds, these institutions’ macroeconomic and policy backdrop has never been stronger, and is paying off for company fundamentals and investor returns.

Security as a Secular Growth Engine

The war in Ukraine—coupled with the United States’ increasing unilateralism and insistence on European strategic autonomy—has catalyzed a permanent shift in European fiscal policy: Europe must own its own security. This is no longer a cyclical reaction to conflict, but a structural pivot.

As a result, NATO’s 2.0% GDP spending target has transformed from a ceiling into a floor. Total EU defense spending topped €380 billion in 2025, a record high.

This rally has broadened beyond ammunition to include infrastructure and energy resilience. We are seeing a “Security Premium” applied to companies involved in, for example, cabling, cyber defense, and energy grid security—creating an investment cycle that can be immune to standard business cycle fluctuations.

The Global Mosaic: Winners and Laggards

International investing in 2025 was not a “rising tide” for all. It required navigating distinct national idiosyncrasies.

International investing in 2025 was not a “rising tide” for all. It required navigating distinct national idiosyncrasies.

Other winners included Poland, which benefited from EU recovery funds and massive industrial acceleration; South Africa, which surged on record gold prices and improved energy stability; and Mexico and Brazil (+49.7%), which saw gains as “nearshoring” trends and high real rates attracted carry-trade yield.

Those left out to sea in 2025 included Denmark, which was down 13.5% for the year as Novo Nordisk faced valuation digestion after its meteoric, GLP-1-driven rise; and Indonesia (-2.8%), hampered by a stubborn dollar and domestic inflation battles. India, too, delivered a sluggish 2.6% return as investors rotated out of its expensive valuations into cheaper Korea and China.

The year’s wide range of country successes, as well as some failures, serve as a good reminder that international equities are a mosaic of distinct geographies, industries, and markets—each with their own drivers. This intricate mix provides a compelling risk-adjusted profile for the asset class, as well as an attractive landscape for active managers to apply a range of skills to identify opportunities and risks.

Outlook: The Case for 2026

U.S. equities and non-U.S. equities have traded off dominance over the past 50 years, typically in cycles lasting 5 – 10 years. Following the Great Financial Crisis, U.S. equities had a historic leadership run of nearly 15 years. It is clear that international equities’ outperformance in 2025 was not a “catch-up” trade, but a fundamental regime change—and we believe this rotation is only revving up. There’s much to support continued international outperformance in 2026.

Despite the 2025 rally, the EAFE index still trades at a 37% discount to the U.S. on a P/E basis. With the U.S. market still top-heavy and largely reliant on technology leadership, the diversity of the international market can provide investors with a differentiated risk-adjusted profile compared to single-country or domestic-only portfolios. However, risk and return characteristics will vary over time and are subject to changing market conditions. The structural drivers of 2025—governance reform in Asia, banking health in Europe, and global security spending—highlight the variety of catalysts driving non-U.S. stock performance. Further, each of these trends typically last multiple years, so we believe they will continue to contribute to the mix of drivers shaping international performance in 2026 and beyond.

The U.S. is home to some of the most innovative and resilient businesses in the world, and U.S. holdings will remain a cornerstone of any global portfolio. But international holdings have earned their place. Rather than an afterthought, international exposure has become a strategic necessity for those looking to align their portfolios with these awakening global markets.

1 Unless otherwise stated, data and market performance are based on the MSCI EAFE and MSCI country indexes. Past performance is no indication of future results. All investments involve the risk of loss.

2 Specific investments described herein may represent some but not all investment decisions made by Bailard. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed in this white paper.

About the Bailard International Equities Team

Bailard’s International Equities team is managed by Eric Leve, CFA, and Dan McKellar, CFA, who have a 27-year average firm tenure. The team intentionally reflects the firm’s approach to international portfolios, combining fundamental and quantitative perspectives and closely integrated to make and implement portfolio decisions thoughtfully. With an investment career spanning more than three decades, Eric Leve has helped shape the firm’s thinking across international equities—always with an eye on how geopolitics, demographics, and macroeconomic systems intersect to influence investment outcomes. Dan McKellar leads the team’s quantitative research, driving model enhancements in country and security selection—and working closely with the firm’s analysts to bridge quantitative and fundamental insights which collectively determine strategy implementation. The investment team also includes the expertise of analysts Irene Liando, CFA, who focuses on fundamental equity research and analysis; and Yelena Bobyor, who leads top-down macroeconomic, thematic, and geopolitical research across global developed and emerging markets. The team also draws upon the talents of Bailard’s quantitative analysts, trading desk, and broader researchers.

About Bailard, Inc.

Bailard is an independent firm that has served individuals, families, and institutions since 1969 with comprehensive wealth management and disciplined asset management solutions. Our work is rooted in clear values, long-term thinking, and a steady commitment to putting clients first.

Across the firm, we provide financial and wealth planning, portfolio management, and asset management strategies spanning domestic and international equities, fixed income, sustainable and responsible investing, private real estate, and customized mandates.

Headquartered in the San Francisco Bay Area, Bailard is woman-led and majority employee-owned. The firm manages more than $7.5 billion in assets as of December 31, 2025, and is a Certified B Corporation™ and signatory to the UN Principles for Responsible Investing. We are built on clarity, accountability, and a long-term commitment to doing what’s right for our clients.

For more information about Bailard’s international equity capabilities, please visit www.bailard.com/equity-strategies/

Diana L. Dessonville

Diana L. Dessonville

Executive Vice President | Director, Institutional Client Services

diana.dessonville@bailard.com

(650) 571-5800

CONTACT US

DISCLOSURES: This publication contains the current opinions of the author, and such opinions are subject to change without notice. Information herein is based primarily on data available as of December 31, 2025, and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. We do not think it should necessarily be relied on as a sole source of information and opinion.

Distribution of this publication is for informational purposes only and is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security, strategy, or investment product. It does not consider the particular investment objectives, financial situations, or needs of individual clients. Any references to specific securities are included solely as general market commentary and were selected based on criteria unrelated to Bailard’s portfolio recommendations or the past performance of any security held in any Bailard account. All investments have risks, including the risks that they can lose money and that the market value will fluctuate as the stock and bond markets fluctuate. There is no guarantee that any investment strategy will achieve its objectives. Charts and performance information portrayed in this piece are not indicative of the past or future performance of any Bailard product, strategy, or account unless otherwise noted. Market index performance is presented on a total return basis (assuming reinvestment of dividends) unless otherwise noted. Bailard cannot provide investment advice in any jurisdiction where it is prohibited from doing so.

There are risks involved in investing, including the risk of loss and the risk that the market value of your investments will fluctuate as the stock market fluctuates. International and emerging market equities are subject to increased risks due to economic or political instability, differences in accounting principles, and fluctuating exchange rates, with heightened risks for emerging markets. Investments in a particular style may underperform other styles of investing or the overall market.

Past performance is no guarantee of future results. All investments have the risk of loss.

Index definitions: The MSCI Europe, Australasia, Far East Index, “MSCI EAFE” index is a free float-adjusted market capitalization index that is designed to measure developed market (ex-US & Canada) equity performance. The MSCI ACWI ex USA Index is a free float-adjusted adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets. The index includes developed and emerging market country indices. The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. With 576 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the US. The S&P 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. All MSCI indices are presented U.S. dollar terms on a total return basis, assuming the reinvestment of dividends after the deduction of withholding taxes. All indices are unmanaged, uninvestable, and do not reflect any transaction costs.

How We’ve Stayed Steady

What stood out was the focus on execution. Decisions were made thoughtfully, and teams stayed engaged through uneven conditions. We continued to invest in our people and our processes rather than waiting for perfect clarity, and our independence gave us the space to be deliberate without the pressure to chase short-term outcomes.

Experience matters, and the colleagues leading our teams today have worked together for years. They’ve been through different cycles, learned alongside one another, and developed a shared way of working. When conditions shift, that experience shows up quickly in how decisions are made and how priorities are set.

Experience matters, and the colleagues leading our teams today have worked together for years. They’ve been through different cycles, learned alongside one another, and developed a shared way of working. When conditions shift, that experience shows up quickly in how decisions are made and how priorities are set.

That continuity is evident in our real estate platform. Nearly a year ago, Preston Sargent, longtime leader of Bailard’s real estate business, announced his intention to retire, allowing ample time to plan the transition with care. Effective January 1, Tess Gruenstein and James Pinkerton now serve as co-heads of the platform and as co-CEOs of the Bailard Real Estate Fund. Their partnership reflects years of working together, with complementary skills and a consistent approach to decision making. Alex Spotswood continues to drive acquisitions and portfolio management, and Preston remains involved as a strategic advisor, offering perspective shaped by decades of experience.

That same approach shows up across the firm. In 2025, Dave Harrison Smith, CFA, became Chief Investment Officer, drawing on his background and the collaborative way our investment teams operate. His promotion reinforced the direction already in place. In his first six months as CIO, Dave has helped bring even greater cohesion across the investment platform.

This all speaks to something simple. Decisions are being made by people who know the business, know the work, and know each other well. Trust is earned quietly, over time. Staying steady comes from the people in place and the way they work together.

# # #

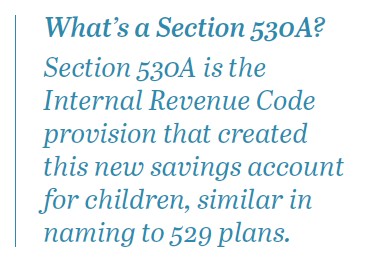

Understanding Section 530A Accounts

When new savings rules are introduced, families often ask a simple question: Is this right for us? The recently created Section 530A account, also known as a “Trump Account,” is no exception.

While the name has drawn attention, the more practical question is how this account fits alongside familiar options such as 529 plans, custodial accounts, and Roth IRAs for children. Like most planning tools, 530A accounts come with trade-offs, and understanding those trade-offs helps families decide whether, and how, this option belongs in a broader strategy.

This article explains how 530As work, where they may fit, and how to think about them alongside other savings tools when deciding where to save for a child.

What Is a 530A Account?

530A accounts are designed to encourage long-term saving and investing for children under age 18. They share some characteristics with traditional IRAs in that contributions and investment earnings grow tax-deferred.

530A accounts are designed to encourage long-term saving and investing for children under age 18. They share some characteristics with traditional IRAs in that contributions and investment earnings grow tax-deferred.

What makes these accounts distinct is how they are funded, invested, and accessed during childhood. Until the year a child reaches age 18, 530As follow special rules that do not apply to traditional IRAs. Beginning in the age-18 year, the account transitions and becomes subject to the standard traditional IRA rules.

How 530A Accounts Are Funded

Contribution rules are one of the most important distinctions between 530A accounts and other savings vehicles for children. Contributions may come from several sources, with different rules applying before and after age 18.

Federal Contribution

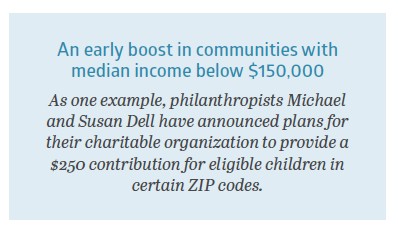

Eligible children born between January 1, 2025, and December 31, 2028, may receive a one-time $1,000 Federal contribution. The child must be a U.S. citizen with a valid Social Security number, and an election must be made on IRS Form 4547. Although eligibility is tied to births beginning in 2025, contributions cannot be made before July 4, 2026.

Personal Contributions

Parents, grandparents, or any other individuals may contribute on a child’s behalf. Unlike traditional and Roth IRAs for children, earned income is not required, and there are no income limits for contributors. Total personal contributions from all sources are capped at $5,000 per year (lower than traditional and Roth IRA limits) and must be made by December 31 of the applicable year. Personal contributions are made with after-tax dollars and are not deductible.

Employer Contributions

Employers may contribute up to $2,500 per year for an employee or an employee’s dependent. These contributions count toward the $5,000 annual personal contribution limit and are not included in the employee’s taxable income.

Governmental and Charitable Contributions

Governmental and Charitable Contributions

Certain governmental entities and charitable organizations may also contribute to 530A accounts for a qualified class of beneficiaries under age 18. These contributions are not subject to dollar limits and do not count toward the annual personal contribution cap.

Contributions Beginning at Age 18

In the age-18 year, 530A accounts transition to a standard traditional IRA framework. Contributions must be supported by the beneficiary’s earned income and are subject to standard IRA limits and deductibility rules.

Investment Rules

While the beneficiary is under age 18, 530A accounts are limited to low-cost mutual funds or ETFs that track the S&P 500 Index, or other qualifying U.S. equity indexes. Individual securities, sector-specific funds, and fixed income investments are not permitted during this period.

Beginning in age-18 year, these restrictions are lifted and the account may be invested like any other traditional IRA, allowing for greater flexibility and alignment with the beneficiary’s time horizon, risk tolerance, and financial goals.

Access and Tax Treatment

530As are subject to a strict lock-up period during childhood. No withdrawals are permitted before age 18, and there are no hardship or special exceptions.

Beginning January 1 of the year the beneficiary turns 18, funds may be withdrawn for any purpose. Distributions generally follow traditional IRA rules, including ordinary income taxation and a potential 10% early withdrawal penalty before age 59½, unless an exception applies. 530A accounts are also subject to required minimum distribution (RMD) rules.

Personal contributions are made with after-tax dollars and create basis in the account. These amounts are not taxed again when distributed, though earnings are taxable and subject to early-withdrawal penalties. Contributions from the Federal government, employers, and charitable organizations (and earnings from these contributions) are treated as pre-tax dollars and are fully taxable when distributed.

All distributions follow pro-rata rules, meaning each withdrawal reflects a mix of taxable and after-tax amounts, rather than allowing personal contributions to be withdrawn first. This calculation applies only to the 530A account itself and does not aggregate other traditional IRAs.

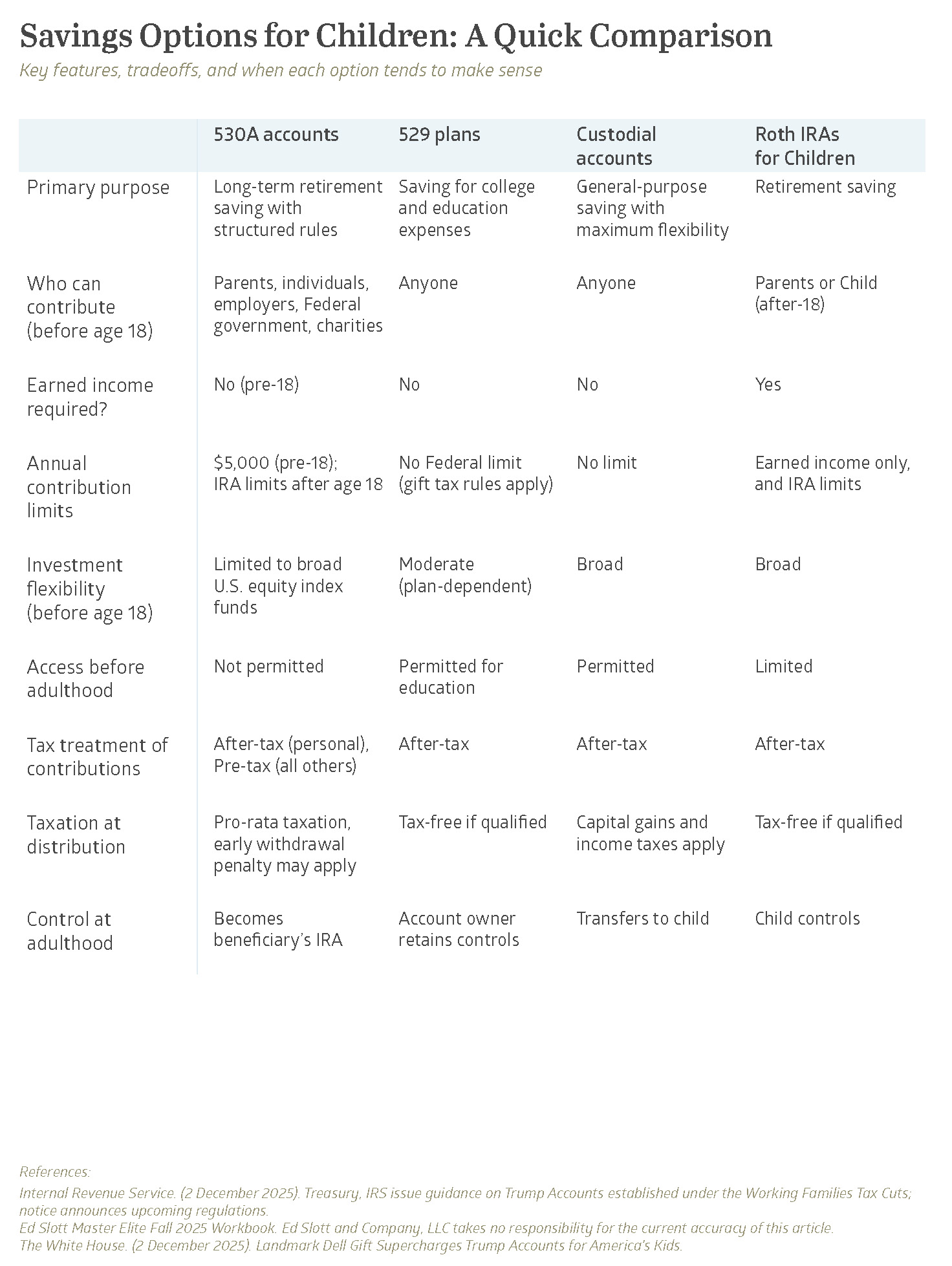

How 530A Accounts Compare to Other Options

Families typically have several tools available when saving and investing for children, each designed for different goals and tradeoffs. The right choice depends on how flexible the funds need to be, how they are expected to be used, and when access may be required.

At a high level:

- 530A accounts emphasize long-term growth with limited flexibility during childhood.

- 529 college savings plans are designed specifically for education-related expenses and often offer the most favorable tax treatment.

- Custodial accounts (UTMA/UGMA) provide broad flexibility but transfer control to the child at the age of majority.

- Roth IRAs for children can be effective when earned income is available and retirement savings is a priority.

The table below summarizes key differences across these options to help frame the trade-offs at a glance. In practice, many families use a combination of strategies rather than relying on a single account type.

Final Thoughts

While they add a tax-advantaged planning option for families, Trump Accounts are not a universal solution. Their usefulness depends on a family’s goals, time horizon, and how much flexibility is needed during childhood.

530A accounts are best viewed as a complement to existing strategies such as 529 plans, custodial accounts, or Roth IRAs for children. In many cases, the most effective approach is not choosing one account over another, but understanding how different tools can work together based on how and when funds are expected to be used.

# # #

# # #

References:

Internal Revenue Service. (2 December 2025). Treasury, IRS issue guidance on Trump Accounts established under the Working Families Tax Cuts; notice announces upcoming regulations.

Ed Slott Master Elite Fall 2025 Workbook. Ed Slott and Company, LLC takes no responsibility for the current accuracy of this article.

The White House. (2 December 2025). Landmark Dell Gift Supercharges Trump Accounts for America’s Kids.

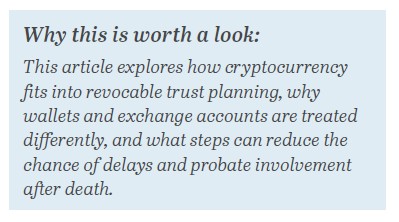

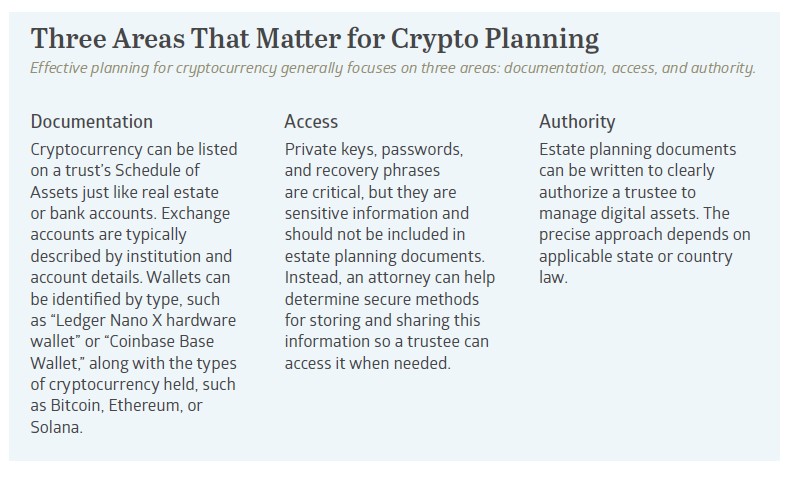

Avoiding Crypto Probate

Cryptocurrency ownership has grown rapidly, and many people now hold Bitcoin, Ethereum, Solana, and other digital assets in wallets or on exchanges, such as Coinbase. Yet estate planning for these assets can be challenging. Unlike most traditional assets, cryptocurrency lacks a straightforward titling or beneficiary framework, which means it does not always fit neatly into conventional revocable trust planning.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

Why Cryptocurrency Requires a Different Approach in Revocable Trust Planning

Traditional assets can often be placed into a revocable trust by changing legal title. A home can be deeded into a trust. A brokerage account can be retitled. Certain assets, such as life insurance policies, generally do not require retitling and instead name the revocable trust as the beneficiary.

Other assets are handled differently. Tangible personal property—such as artwork, antiques, or collectibles—is commonly addressed by listing the asset on the trust’s Schedule of Assets and, in many cases, by executing a general assignment of personal property. These assets are not retitled in the traditional sense, but they are still brought within the trust’s asset base.

Cryptocurrency fits within revocable trust planning in a similar way, but with an added layer of complexity driven by how the asset is held. For estate planning purposes, the critical distinction is whether cryptocurrency is held directly by the individual in a self-custody wallet or held with an institutional custodian through an exchange account.

Wallets vs. Exchange Accounts

Self-custody wallets such as Ledger, Trezor, MetaMask, or Coinbase Base Wallet are controlled directly by the owner through private keys. There is no institution standing between the individual and the blockchain, which is a decentralized, secure digital ledger that transparently records transactions.

Because there is no traditional “title” to change, bringing wallet-held cryptocurrency into a revocable trust is typically handled by:

- Listing the wallet on the trust’s Schedule of Assets, and

- Executing an assignment of digital assets.

When done properly, a trustee can step in and manage these holdings directly without probate or other court involvement. What wallets generally do not allow is conversion into dollars or other fiat currencies. To liquidate, assets often must be transferred from the wallet into an exchange account.

Exchange accounts operate differently. Personal cryptocurrency exchange accounts generally cannot be held in the name of a revocable trust. Instead, the exchange functions as an institutional custodian and controls the private keys on behalf of the account holder.

During life, exchange accounts make it easy to buy, sell, and convert cryptocurrency to cash. After death, however, access often slows significantly. Institutional custodians are rightly cautious about releasing assets and typically require formal legal documentation to establish authority. Even when an exchange account is listed on the trust’s Schedule of Assets, custodians commonly require:

- A certified death certificate

- Proof of the trustee’s identity

- Court-issued authority, such as letters testamentary or letters of administration

In practice, this often means probate court involvement may still be required, despite advance planning. In California, a limited remedy may be available through a Heggstad petition, which allows a probate court to treat an asset as trust property if it was clearly listed on the trust’s Schedule of Assets, even if it was never formally transferred. While a successful Heggstad petition may help avoid a full probate administration, it still requires probate court filings, legal fees, and several months to complete.

[Note: Some institutional platforms support trust-owned accounts, such as Coinbase Prime, though these are generally designed for business or institutional use rather than personal accounts.]

A Practical Example: How Wallets and Exchanges Are Treated

Consider John, a California resident with two types of crypto holdings.

Wallet-held assets:

John has $150,000 of Bitcoin stored on a Ledger Nano hardware wallet and $50,000 of Ethereum in a Coinbase Base Wallet. Both are listed on his revocable trust’s Schedule of Assets and supported by an assignment of digital assets. When John passes away, the trustee retrieves the recovery information and transfers the cryptocurrency as directed in the trust. No probate court involvement is required, and the process remains private.

Exchange-held assets:

John also keeps $75,000 of cryptocurrency in a personal Coinbase exchange account. Even though the account is listed in the trust, the institutional custodian requires a death certificate, proof of identity, and probate court-issued letters of authority before granting access. This portion of his estate is delayed and requires legal filings.

Wallets may allow for smooth administration within a revocable trust. Exchange accounts held with institutional custodians are more likely to involve probate court oversight, even with advance planning.

Facilitating Access for the Trustee

Facilitating Access for the Trustee

The most important element of cryptocurrency estate planning is coordination. Working with an attorney helps ensure that critical access information is organized, securely documented, and available to the trustee when needed.

Cryptocurrency can be owned by a revocable trust and administered without probate, but only if the trustee can actually access the assets. Control depends on passwords, private keys, recovery phrases, and platform-specific procedures. Because this information is highly sensitive, it should not be included directly in the trust document. Instead, attorneys often help prepare a separate memorandum of instructions that explains where assets are held and how the trustee gains access.

This approach reduces confusion, delays, and court involvement by giving the trustee both clear authority and a practical roadmap for administering cryptocurrency assets.

Key Takeaways

Cryptocurrency does not have to derail a well-designed estate plan. The key distinction lies in how assets are held. Wallet-based cryptocurrency, when properly documented and connected to a revocable trust, may pass to heirs privately and efficiently without probate. Exchange-held cryptocurrency, managed by institutional custodians, may still require probate court involvement before funds are released unless accounts are structured in advance through platforms that support trust ownership.

# # #

This discussion is for educational purposes only and is not legal advice. Always consult a qualified attorney in your jurisdiction for guidance on your specific situation.

Communicating Trust and Credibility in an Age of Volatility

The recent fireside-style conversation hosted by Financial Narrative, informed by Financial Times research, explored credibility and leadership in today’s environment. Our SVP of Marketing & Communications, Erin Randolph, PCM®, joined the panel on behalf of Bailard for a candid discussion with industry peers.

Economic Brief: A Little Good News

Many years after hanging up his cleats in favor of a guitar, former linebacker Collins Obinna Chibueze still strikes a commanding presence under the bright lights. Standing 6'4", not counting the cowboy hat, the fast-rising singer better known as Shaboozey enjoyed a breakout year in 2024, earning him a “Best New Artist” nomination for last year’s Grammy Awards. The melodious Shaboozey moniker has its own football roots, dating back to when a high school coach slapped the name on his helmet as a phonetic reading of his surname. Shaboozey has been sounding it out ever since, blending country music with elements of hip hop, rock, and other influences. At their best, Shaboozey’s songs are playful and catchy while also introspective and questioning, built atop a bassline of human struggle.

It was undeniably a doozy of a year in 2025. Bloomberg columnist Clive Crook summarized it nicely: “Over the past 12 months, the U.S. has seen…every norm of economic policy—trade policy, fiscal policy, monetary policy—blithely tossed aside. At the same time, the U.S. economy stands at the bleeding edge of what might be as consequential an economic revolution as the transition from farming to manufacturing, or from manufacturing to services—except that the AI revolution could happen much faster.”1 Besides all that, 2025 was rather uneventful! The jump in economic uncertainty clearly did not dissuade the markets. It was, perhaps, another reminder that the stock market is not the economy. Investors heard sufficient good news to drive equity prices sharply higher for a third straight year. Critically, corporate profits did not disappoint: Standard & Poor’s (S&P) currently estimates that S&P 500 Index operating earnings advanced 13% per-share in 2025. That was the bottom line, but other tailwinds including lower interest rates, AI enthusiasm, and favorable tax policies also helped equities overcome numerous obstacles last year.

Amidst all the policy upheaval and a 43-day U.S. government shutdown—longest in history—investors learned to cope at times with a dearth of information from official government agencies. Beyond minding the information gaps, the August 2025 firing of Dr. Erika McEntarfer, commissioner of the Bureau of Labor Statistics (BLS), cast a shadow across the federal data landscape. Her dismissal immediately followed the Bureau’s July employment report in which the BLS sharply revised down its estimate of jobs added in May and June by a cumulative 258k. Whether or not the administration is correct that the “BLS is broken,” the optics of the decision did not go over well.2 In fact, handing McEntarfer a pink slip via social media hours after a disappointing jobs report may end up sowing more doubt. It prompted the Bloomberg Editorial Board to caution that “In so many words, this tells financial markets that official statistics are no longer to be trusted.”3 The ultimate consequences are unclear for the investment community as 2026 gets underway, but it may encourage decision-makers to rely more heavily on private sector data, where possible. Bloomberg’s Crook suggests that investors may be “flying blind” in an environment of heightened uncertainty and confusion over the state of the economy. For the financial markets, the adage “no news is good news” doesn’t typically apply.

Dot Com Club

A pivot to using more data from the private sector could easily start in Bentonville, Arkansas at Walmart’s global headquarters. The obvious reason: sheer scale. Walmart hauls in roughly 10% of all retail spending in this country, excluding automobiles.4 With around 2.1 million employees across 19 countries worldwide, Walmart amassed a staggering $681 billion of revenue in fiscal 2025—which in Gross Domestic Product (GDP) terms would put Walmart on par with countries such as Argentina and Sweden. Avoiding the company is a logistical challenge: 90% of the U.S. lives within 10 miles of a Walmart store.5 So when Walmart talks, the markets listen. In late November, Walmart reported its third quarter results, posting sales growth of ~6% and closer to a 7% advance for earnings per share (EPS). Perhaps more telling, outgoing CEO Doug McMillon said that U.S. customers and members are “still spending with upper and middle income households driving our growth.”6 McMillon acknowledged that lower income families have been under additional pressure, but also noted that like-for-like Q3 inflation was just 1.3% for Walmart US.

If Walmart as a tech company seems disorienting, consider that the world’s largest retailer just landed on the Nasdaq Stock Market. In December, after trading for over 50 years on the New York Stock Exchange, Walmart’s stock (WMT) migrated to the Nasdaq, joining companies such as Nvidia, Apple, Alphabet, and Microsoft. The exchange of choice for many tech companies, Nasdaq became the first U.S. stock market to trade online back in 1998. Walmart’s share price carries the sheen of a tech stock as well. After rising 23% last year, WMT finished 2025 trading at nearly 38x forward earnings, higher than many of its new Nasdaq peers.

Cold Brew

Although Walmart has managed to keep prices low via some alchemy of scale and technology, the overall inflation picture remains uncertain. Hot spots persist, including some high-profile areas. Electricity prices rose 6.9% year-over-year in November, per the BLS’s Consumer Price Index (CPI).9 Data centers are getting much of the blame, according to The Wall Street Journal, but hurricanes, wildfires, state renewable energy plans, and the replacement of aging or damaged grid equipment are all playing a role.10 California is feeling the pain more acutely than other states: power prices rose 35% inflation-adjusted over the 2019 to 2024 timeframe.

No area is getting more attention than health insurance costs. With the expiration of federal tax credits, the 24 million people that enrolled in coverage last year under the Affordable Care Act (ACA) will see their premiums increase significantly. San Francisco-based health policy organization KFF estimated that premium payments will more than double.11 For those covered under Medicare Part B, the 2026 standard monthly premium is going up nearly 10%. Employer-based health insurance is not immune, either. Mercer projects a total health benefit cost increase of 6.7% this year, pushing the average cost above $18,500 per employee.12 In 2025, Mercer’s annual survey found that the average cost of employer-sponsored health insurance rose 6%, driven in part by sharp growth in prescription drug spending with more companies including GLP-1 coverage.

Through all the noise, geopolitical tumult, and incertitude, Wall Street is uniformly optimistic. In fact, a year-end Bloomberg News survey found that all 21 strategists estimate the S&P 500 Index will post a fourth consecutive positive year in 2026.14 Wall Street analysts are estimating another strong year for corporate profits, as well, with S&P 500 earnings per share expected to increase by 14.8% on top of 2025’s already strong earnings growth.15 Again, the stock market is not the economy, but it does beg the question of whether everybody is gettin’ tipsy, to paraphrase Shaboozey. Another year of rising profits would certainly qualify as a little good news.

# # #

1 “Investors Are Flying Blind Into the ‘Golden Age,’ www.bloomberg.com, 12/26/2025.

2 “BLS Revisions Show President Trump Was Right – Again,” www.whitehouse.gov, 9/9/2025.

3 “Trusted Data Is a Vital Economic Asset,” www.bloomberg.com, 8/15/2025.

4 “How Walmart became a tech giant – and took over the world,” www.economist.com, 5/15/2025.

5 “Walmart, Inc.: Morgan Stanley Global Consumer & Retail Conference,” www.walmart.com, 12/2/2025.

6 “Walmart Inc. Q3 2026 Earnings Call,” www.walmart.com, 11/20/2025.

7 “Can Walmart Shed Its Discount Vibe?” www.nytimes.com, 6/23/2025.

8 “Heard on the Street: Should Walmart Really Be Trading Like a Tech Company?” www.wsj.com, 12/6/2025.

9 “Consumer Price Index for All Urban Consumers (CPI-U), Table 7,” www.bls.gov, 12/18/2025.

10 “Be Prepared to Keep Paying More for Electricity,” www.wsj.com, 12/29/2025.

11 “ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire,” www.kff.org, 9/30/2025.

12 “Mercer survey finds US employers and workers will face affordability crunch as health insurance cost is expected to exceed $18,500 per employee in 2026,” www.mercer.com, 11/18/2025.

13 “High Coffee Prices Are Changing How Consumers Take Their Daily Brew,” www.bloomberg.com, 12/16/2025.

14 “Every Wall Street Analyst Now Predicts a Stock Rally in 2026,” www.bloomberg.com, 12/29/2025.

15 FactSet, EPS One-Year Growth (%) estimated for year-end 2026, data retrieved 1/8/2026.

Specific investments described herein do not represent all investment decisions made by Bailard. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Read more