Country Indices Flash Report – January 2024

Global tensions are rising in the Middle East and beyond. Iran targeted Sunni militias in Pakistan, and their proxies targeted an American air base in Iraq. Red Sea shipping disruptions have caused freight costs for many routes to more than double.

Quarterly International Equity Strategy Q4 2023

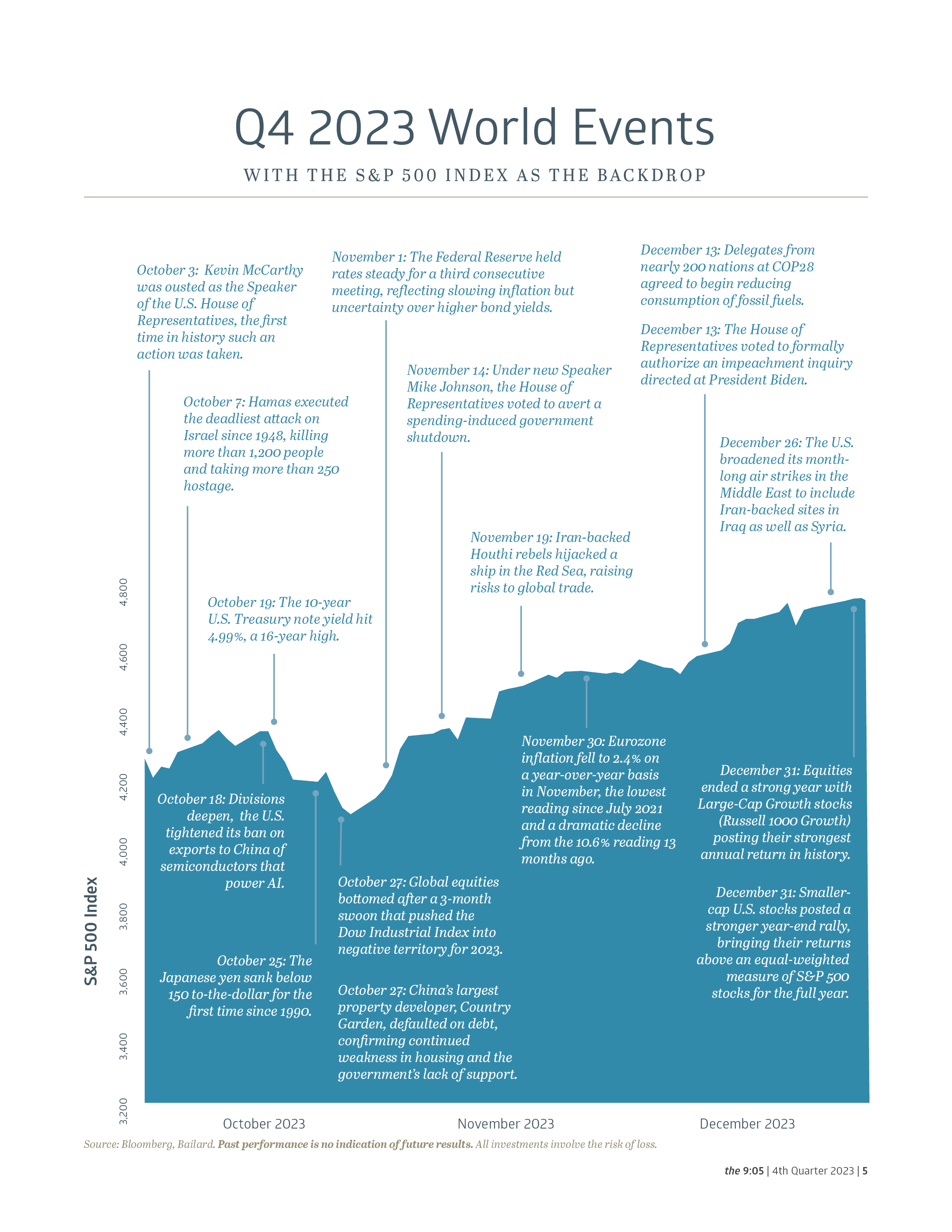

In the 4th quarter, global equity markets found a new pillar to build upon 2023’s already impressive investment results. Declining U.S. Treasury yields in the final two months of the year drove broad developed markets to within a hair’s breadth of EAFE’s all-time high. The year began with fears of global recession and high inflation in most major markets (excluding Japan). The year ended with “peak” optimism: that central banks, most critically the Fed, had brought inflation down to near normal levels without causing a recession. That optimism led to a broad expansion of global equity valuations in the 4th quarter. As we look to the new year, even though the residual effects of central banks’ tightening cycles may slow economic growth, a pivot toward lower rates could sustain valuations. And, despite lower economic growth, forecasters are looking for further earnings growth. In combination, 2024 could again be a rewarding one for international equity investors.

Bailard Achieves B Corp™ Certification

San Francisco, CA – January 18, 2024 – Bailard, Inc., an independent wealth and asset management firm, proudly announces its recent certification as a B Corporation™ (B Corp™). This achievement marks a significant stride in the firm’s dedication to values-driven practices that benefit its clients and employees, and the community.

“Our recent certification as a B Corporation reaffirms Bailard’s commitment to values-driven wealth and asset management, and the principles ingrained in our company since its founding over 50 years ago,” said Michael Faust, CFA, President of Wealth Management. “The rigorous certification process is a proof point that, at Bailard, we ‘walk the talk,’ too. Our dedication to making a positive impact is not just rhetoric but a reflection of the values that guide our team every day.”

Bailard’s certification places it among the distinguished cohort of over 3,500 certified B Corps worldwide, recognized for meeting B Lab’s stringent standards of verified social and environmental performance, public transparency, and legal accountability emphasizing the delicate balance between profit and purpose.

The firm integrates B Corp principles into various facets of its business, guiding clients in aligning portfolios with their values, fostering a strong and award-winning company culture, and championing responsible and impact investing. Bailard also actively pursues initiatives to enhance office efficiencies and, in 2019, established the Bailard Foundation to contribute to the betterment of the communities it serves.

CEO Sonya Mughal, CFA, emphasized, “Choosing to pursue B Corp Certification was a natural step for Bailard; it aligns seamlessly with the values that have guided us for decades. We can hold ourselves accountable through the independent verification and public transparency, and also lead by example as we prioritize a culture of responsible business practices and continuous improvement.”

For those seeking wealth and asset management aligned with values and a commitment to positive impact, Bailard invites you to explore the possibilities. Learn more about our B Corp journey at www.bailard.com/bcorp and discover how we’re redefining excellence in financial services.

About Bailard, Inc.

Founded in 1969, Bailard is an independent, value-driven asset and wealth management firm serving individuals, families, and institutions alike. Bailard has built a long‐term asset management track record across domestic and international equities, fixed income, and private real estate, as well as robust, in-house sustainable, responsible and impact investing expertise. Through it all, Bailard works with clients to align their financial goals with their values. Based in the San Francisco Bay Area with over $5.8 billion in assets under management as of 12/31/2023, Bailard is a majority employee-owned and women-led firm, a Certified B Corporation™, and a Principles of Responsible Investing signatory.

Bonds Are Back

Jeremy Wager-Smith, Fixed Income Portfolio Associate, examines the dynamic shifts and key trends that shaped the bond market in 2023.

A Dynamic Year

Interest rate volatility defined 2023 for fixed income markets. Markets skewed more reactionary than anticipatory, as the bond market digested a stronger-than-expected U.S. economy, an active Federal Reserve (Fed), regional bank turmoil, and a mountain of U.S. Treasury issuance.

The higher-for-longer interest rate narrative took hold by mid-year, as initial expectations of summer rate cuts faded, and a resilient U.S. labor market came into focus. Fed Chair Jerome Powell made clear the Fed’s commitment to bring inflation down to its 2% target as the Federal Open Market Committee (FOMC) elected to raise the Fed Funds target rate four times throughout the year, with the last hike occurring in July. This marked the eleventh interest rate hike of this cycle and brought the Fed Funds target rate to 5.50%, a level not seen since 2001. As expected, ultra-short yields rose in response to continued hikes and the Fed’s hawkish talk. 10-year U.S. Treasury bond yields peaked a bit later in mid-October at 4.99%—a level not seen since July of 2007—before dropping back down to close the year nearly unchanged. Looking forward to 2024, our outlook for bonds remains positive. We expect interest rate volatility to remain high, but at a more subdued level than in 2023.

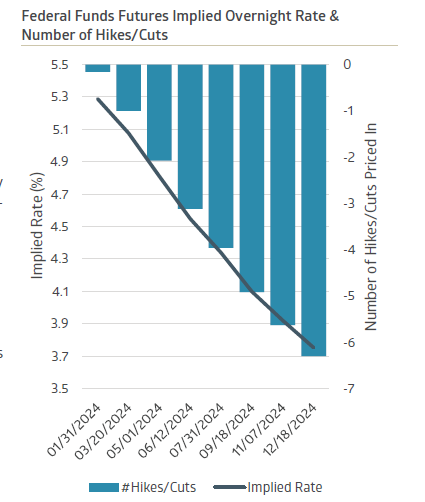

A Look Ahead at Federal Reserve & Monetary Policy

In our view, markets are pricing in an excessive number of rate cuts in 2024 and, thus, a more dovish Fed than we anticipate. CME Fed Funds futures (a series of derivatives used to hedge short-term interest rates) are pricing in a 2024-year-end effective Fed Funds rate of 3.75%. This level implies over 150 basis points of rate cuts by year-end, with cuts beginning in March and continuing throughout the year.

Absent a recession or deflationary shock, we expect rate cuts to begin later in the year, and, cumulatively, to be fewer than what markets are pricing in. With the blistering rally in intermediate- to longer-dated Treasuries through year-end, markets have partially eased financial conditions for the Fed. The Goldman Sachs Financial Conditions Index—which uses borrowing costs, equity ratios, and credit spreads to gauge financial tightness—concluded 2023 at its lowest year-to-date level after reaching a year-to-date peak in late October.

Meanwhile, headline inflation is continuing its choppy decline from last year’s decade high of 9.1% and, as seen in December’s seasonally-adjusted unemployment rate of 3.7%, the U.S. labor market remains resilient. This still-strong U.S. economic picture and favorable financial environment, coupled with the Fed’s tendency to do too little too late, suggests that broad-based financial distress would need to accelerate dramatically to warrant the significant easing of monetary policy expected by markets in 2024.

Yield Curve Inversion Continues

The yield curve remains inverted, but to a lesser degree than a year ago. Often cited as a harbinger of economic pain to come, yield curve inversion occurs when shorter-term U.S. Treasury bonds outyield longer-term U.S. Treasury bonds. The most widely adopted measure of yield curve inversion is the spread, or difference in yield, between 10-year and 2-year U.S. Treasury bonds. This spread closed 2023 at -37 basis points, after beginning the year at a wider level of -56 basis points. With our expectation that the Fed will begin to cut the Fed Funds rate by mid-year, we anticipate this spread narrowing throughout the year as the short end of the yield curve retreats.

Municipal Credit Expectations

Municipal bonds rebounded in 2023 after a difficult 2022, as the Bloomberg 1-15 Year Municipal Bond Index saw a healthy uptick of 5.26%. Strong demand coupled with slightly lower municipal issuance on a year-over-year basis contributed to municipals ending 2023 at their richest levels in 40 years relative to Treasury bonds.

The credit profile of many municipal issuers experienced significant tailwinds coming out of the pandemic. Propelled by strong tax receipts and ample federal assistance, municipalities bolstered their balance sheets and established rainy-day funds. Since then, the combination of higher debt-servicing costs, rising operating expenses, and markedly weaker-than-expected tax revenues will most likely result in weaker municipal credit conditions in 2024. To insulate portfolios from much of this expected deterioration, taxable investors could stand to gain by favoring higher quality credits and resilient revenue sources.

We continue to closely monitor the State of California’s fiscal situation. A wealth exodus and absence of federal pandemic stimulus, combined with an overreliance on cyclical personal income tax revenues and optimistic revenue forecasts, have left the state facing budget deficits for fiscal years 2023 and 2024. Although the state does face fiscal difficulties, with its AA2/AA- rating we remain comfortable holding the state credit. In our view, demand for all California in-state bonds should remain high as state tax rates create demand for double-tax exempt income.

The Trajectory of Corporate Bonds

Aggregate and corporate bond indices provided positive returns in 2023, with the Bloomberg U.S. Aggregate Bond Index increasing 5.53% and the ICE Bank of America 1-10 Year Corporate Bond Index posting a 7.33% gain. Investment grade corporate spreads, or the pickup in yield between a corporate bond and a comparable maturity US Treasury bond, narrowed in 2023. If a hard economic landing or recession can be avoided, we anticipate spreads for high quality bonds staying relatively tight and rangebound throughout the year even with an expected increase in 2024 investment grade issuance.

Regarding industry-specific expectations, we continue to steer clear of regional banks due to ongoing concerns about the impact of held-to-maturity securities on their balance sheets. Instead, we prefer larger, systemically important financial institutions. For tax exempt investors, we have a continued preference for a higher allocation in corporate and mortgage-backed securities relative to standard aggregate benchmarks. We believe that the current, attractive level of interest rates offers a buffer against possible weakness in the stock market.

1 Bloomberg – FFG4 COMB Comdty

2 Bureau of Labor Statistics

3 Yield Curve – Plotted series US Treasury bond yields. Organized from shortest to longest time to maturity.

4 Bloomberg

5 Bloomberg YTDMTOT Index

6 “S&P Downgrades California Bond Outlook Amid Budget Crunch” – The Center Square

7 Investment Grade – Corporate bonds rated Ba1/BB+ or higher

Economic Brief: The Abominable No-Man

From the legacies of iconic investors to the dynamic 2023 markets, Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist, Wealth Management, and Portfolio Manager, Sustainable, Responsible and Impact Investing) presents an insightful perspective on the economic climate, aided by the witticisms of Charlie Munger.

Legendary investor Charlie Munger passed away in late November, just a month shy of reaching the century mark. For 45 years, Munger served as the witty and characteristically caustic partner to Warren Buffett at Berkshire Hathaway. He was a surefire sound bite, adept at delivering zingers with a wry smile while on stage at Berkshire’s annual “Woodstock for Capitalists” shareholder meetings in his hometown of Omaha, Nebraska. Sometimes, he was funny: “Learning from other people’s mistakes is much more pleasant.” Often, he was insightful: “People calculate too much and think too little.” Undeniably, he was practical: “Don’t bail away in a sinking boat if you can swim to one that is seaworthy.” The vast collection of “Mungerisms” captures his concise yet astute speaking style, and lent Munger cult hero status amongst the investment crowd. Long before Twitter’s original 140-character limit, Munger endorsed brevity. In Berkshire’s 2022 letter to shareholders, Buffett acknowledged that “what it takes me a page to explain, (Charlie) sums up in a sentence.”

Legendary investor Charlie Munger passed away in late November, just a month shy of reaching the century mark. For 45 years, Munger served as the witty and characteristically caustic partner to Warren Buffett at Berkshire Hathaway. He was a surefire sound bite, adept at delivering zingers with a wry smile while on stage at Berkshire’s annual “Woodstock for Capitalists” shareholder meetings in his hometown of Omaha, Nebraska. Sometimes, he was funny: “Learning from other people’s mistakes is much more pleasant.” Often, he was insightful: “People calculate too much and think too little.” Undeniably, he was practical: “Don’t bail away in a sinking boat if you can swim to one that is seaworthy.” The vast collection of “Mungerisms” captures his concise yet astute speaking style, and lent Munger cult hero status amongst the investment crowd. Long before Twitter’s original 140-character limit, Munger endorsed brevity. In Berkshire’s 2022 letter to shareholders, Buffett acknowledged that “what it takes me a page to explain, (Charlie) sums up in a sentence.”

Munger liked to keep things simple. In fact, his favorite tool to tackle thorny issues was the humble checklist: “I’m a great believer in solving hard problems by using a checklist. You need to get all the likely and unlikely answers before you; otherwise, it’s easy to miss something important.” The checklist method was no guarantee of cracking the case, however. Munger said that if they lacked special insight into a company, they would set the investment aside as “too tough” and move on. Acknowledging one’s limitations is an important trait, something Munger referred to as staying within their circle of competence. However, both Buffett and Munger admitted they missed their share of investment opportunities this way, notably, in the technology sector. Further, the duo faulted themselves for “mistakes of omission,” where they failed to invest in a company such as Wal-Mart despite having a solid understanding of the business. Those called strikes didn’t hurt too badly: a $1,000 investment in Berkshire Hathaway made at the end of 1978 was worth nearly $3 million by year-end 2022.

It could be said that the hallowed performance track record assembled by the Oracles of Omaha was one percent inspiration, and ninety-nine percent contemplation. Both Munger and Buffett spent countless hours reading and thinking, and comparatively few hours taking action. Buffett reportedly playfully referred to Munger as “The Abominable No-Man” because Munger so frequently turned down potential investments. When they did decide to invest, it was typically in a big way, either buying a business outright or taking a significant stake in the company. Berkshire spent $1.3 billion buying shares of Coca-Cola several decades ago, and in 2022 received dividend payments of $704 million on their shares, which had by then appreciated to a $25 billion market value. The annual dividend yield calculated on their original cost had ballooned to a gaudy 54% – a testament to time, patience, and the power of dividend growth.

Checking it Twice

In honor of Charlie Munger, a simple checklist for U.S. equity investors in 2023 is presented at right. Essentially every item broke in favor of equities. First and foremost: inflation. The trend couldn’t have been much more favorable on that front. The Consumer Price Index (CPI) increased a worrisome 6.5% year-over-year in 2022, peaking at a 40-year-high of 9.1% mid-year. By November 2023, the CPI’s growth rate had slowed to 3.1%, within striking distance of the Federal Reserve’s 2% target.

Importantly for consumers (and politicians), the headliners of food and energy prices have improved significantly. Gasoline prices declined nearly 9% year-over-year as of November, while food prices rose just 2.9%. A surge in domestic oil supply helped to dampen energy prices. In fact, U.S. oil production established a new worldwide record of 13.2 million barrels per day in November, surpassing the previous highwater mark set by the U.S. in early 2020. Domestic output—led by shale oil drillers in the Permian Basin of Texas and New Mexico—is so strong that we are exporting as much crude oil, refined products, and natural gas liquids as Saudi Arabia or Russia produces.

The sharp deceleration in the rate of inflation enabled Fed officials at their December meeting to project three Fed Funds rate cuts in 2024 and four more in 2025, suggesting we may have seen the end of the Fed’s rate hiking campaign. This had visions of a soft landing dancing in investor’s heads, that magical scenario in which the Fed is able to quell inflation via higher borrowing rates without incurring a recession. Economist Paul Krugman went so far as to say, “So far, this has been ‘immaculate disinflation,’ requiring neither a recession nor a large rise in unemployment.” While communicating the Fed’s rate decision, chairman Jerome Powell noted that U.S. Gross Domestic Product (GDP) was on track to expand around 2.5% (inflation-adjusted) for 2023 as a whole. As for corporate earnings, the Standard & Poor’s 500 Index is estimated to have generated 8% to 9% growth per share in 2023. In both cases, that growth lands squarely in the sweet spot, neither overheated nor ice cold.

The sharp deceleration in the rate of inflation enabled Fed officials at their December meeting to project three Fed Funds rate cuts in 2024 and four more in 2025, suggesting we may have seen the end of the Fed’s rate hiking campaign. This had visions of a soft landing dancing in investor’s heads, that magical scenario in which the Fed is able to quell inflation via higher borrowing rates without incurring a recession. Economist Paul Krugman went so far as to say, “So far, this has been ‘immaculate disinflation,’ requiring neither a recession nor a large rise in unemployment.” While communicating the Fed’s rate decision, chairman Jerome Powell noted that U.S. Gross Domestic Product (GDP) was on track to expand around 2.5% (inflation-adjusted) for 2023 as a whole. As for corporate earnings, the Standard & Poor’s 500 Index is estimated to have generated 8% to 9% growth per share in 2023. In both cases, that growth lands squarely in the sweet spot, neither overheated nor ice cold.

In retrospect, the “recession that wasn’t” in 2023 failed to materialize primarily due to basic economic bedrocks: the employment and housing markets. Higher interest rates and still elevated inflation did pose challenges, as anticipated, but consumer spending didn’t wither in the face of those headwinds. Personal Consumption Expenditures (PCE) rose 2.7% year-over-year in November, a modest acceleration from the 2% to 2.5% growth range the series registered for much of the year. Consumers enjoyed the stability of a tight job market, with unemployment at just 3.7% in November, and average hourly earnings up 4%, topping the inflation rate. Further, housing prices have absorbed higher mortgage rates without too much trouble. Transactions are down: monthly existing home sales hit a 13-year low in October. Low inventory has aided prices, however. The S&P CoreLogic Case-Shiller National Home Price Index reflected a 4.8% year-over-year gain in October, a ninth-consecutive month of gains and establishing a new record high. The wealth effect theory—that people spend more as the value of their assets rises—seems intact.

Revenge Spend

To paraphrase music superstar Bruno Mars, consumers are dangerous with some money in their pockets. According to a Bloomberg article, Americans continued to splurge in 2023, shelling out for revenge travel, Taylor Swift tickets, and expensive restaurant meals. A lot of it was funded with debt, the article cautions, pushing credit card balances up to $1.08 trillion prior to the holiday season. Delinquency rates are only modestly above pre-pandemic levels, but the average annual percentage rate (APR) has spiked north of 20%, the highest on record. Some have identified a “silent recession” with millions of people struggling to keep up with student loans, car loans, pricey groceries, and higher housing costs. This doesn’t bode particularly well for consumer spending in 2024, although if the current trend of softening interest rates continues the impact could be dampened.

The term “revenge spending” has been around for several years and is commonly defined as elevated spending in the aftermath of a challenging event or time, such as the pandemic. Carnival Corporation has been a somewhat surprising beneficiary of this phenomenon. An early casualty during the pandemic, for obvious reasons, Carnival pulled in record revenues of $21.6 billion in 2023 and has already booked two-thirds of their occupancy for 2024 at “considerably higher prices.” Carnival noted they captured over 3.5 million new-to-cruise guests during 2023. The stock remains well below its pre-pandemic level, despite a 132% rally in 2023, with the company working to pay down its bloated debt load. After peaking north of $36 billion, Carnival has reduced its long-term debt to just above $30 billion, still exceeding its market capitalization of $23 billion. Although Carnival’s debt remains junk-rated by S&P Global, it did receive an upgrade in December by two notches to BB-. The pandemic’s reverberations are still being felt economically, both positively and negatively.

For equity investors, the banner year for U.S. large-cap indices begs the question of how much upside remains at present. The S&P 500 Index concluded 2023 trading at approximately 22x estimated trailing earnings per share, and nearly 20x estimated 2024 earnings. Valuations have been pushed higher in particular by the incredible surge in tech stocks. According to Bernstein Research, 18% of tech stocks now trade at greater than 10x revenues versus a historical average of 6%. At its year-end 2023 level, the S&P 500 arguably has already discounted the positive impact of lower rates in the year ahead, plus the assumed S&P 500 earnings growth of roughly 13%. That said, markets perpetually look forward and will attempt to start pricing in 2025 assumptions as the year progresses.

For equity investors, the banner year for U.S. large-cap indices begs the question of how much upside remains at present. The S&P 500 Index concluded 2023 trading at approximately 22x estimated trailing earnings per share, and nearly 20x estimated 2024 earnings. Valuations have been pushed higher in particular by the incredible surge in tech stocks. According to Bernstein Research, 18% of tech stocks now trade at greater than 10x revenues versus a historical average of 6%. At its year-end 2023 level, the S&P 500 arguably has already discounted the positive impact of lower rates in the year ahead, plus the assumed S&P 500 earnings growth of roughly 13%. That said, markets perpetually look forward and will attempt to start pricing in 2025 assumptions as the year progresses.

If you listen to prominent economist and strategist Ed Yardeni, there is plenty of upside left. His eponymous research firm believes we might be looking at a “Roaring 2020s” scenario, buoyed by wealthy and liquid households, a strong labor market, productivity gains from the ongoing high-tech revolution, and receding inflation, among other factors. An optimistic take, perhaps, but its longer-term focus would be endorsed by Charlie Munger. In his words: “Warren and I don’t focus on the froth of the market. We seek out good long-term investments and stubbornly hold them for a long time.” That approach seemed to work out okay.

1 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 104

2 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 46

3 Berkshire Hathaway 2022 shareholder letter, www.berkshirehathaway.com

4 Griffin, Tren. “Charlie Munger: The Complete Investor.” 2015. p. 6

5 “The United States is producing more oil than any country in history,” www.cnn.com, 12/19/2023

6 “Inflation, disinflation and vibeflation,” www.nytimes.com, 12/5/2023

7 “’Revenge Spending’ Drives US Credit Card Debt Past $1 Trillion,” www.bloomberg.com, 12/22/2023

8 “Carnival Corporation & PLC Reports Record Fourth Quarter And Full Year Revenues With Continued Strong Bookings And Earnings Momentum,”

www.carnivalcorp.com/investor relations, 12/21/2023

9 “The $19 Trillion Question – What to do with Tech in 2024?”, www.bernsteinresearch.com, 12/18/2023

10 “Ed Yardeni: 12 reasons stock investors will see the S&P 500 hit 5,400 in 2024,” www.marketwatch.com, 12/27/2023

11 Berkshire Hathaway 2022 shareholder letter, www.berkshirehathaway.com

The Rise of B Corps and Benefit Corporations

Focusing on the rise of B Corps and Benefit Corporations, Blaine Townsend, CIMC®, CIMA® (Director of Sustainable, Responsible & Impact Investing) sheds light on the shift towards a business paradigm that values employee, community, and environmental well-being alongside shareholder returns.

The role of corporations in society has always been hotly debated. In fact, Thomas Jefferson warned of the “aristocracy of our monied corporations” a century before the Supreme Court granted Southern Pacific Railroad (and, by extension, all corporations) the same rights as a “person.” Today, large companies drive almost every aspect of American life—from environmental outcomes to political influence. But smaller companies also play a huge role in the U.S. economy and labor force. With that outsized influence comes the opportunity to positively impact shareholders, employees, communities, and the planet. Since 2006, the Certified B Corporation™ framework has set out to guide (mostly smaller) companies in doing just that.

B Corps and Benefit Corporations: Understanding the Difference

The Certified B Corp is a manifestation of a broader movement supporting the idea of the “Benefit Corporation.” In short, a for-profit company that works for shareholders, but also makes an explicit commitment to have a positive impact on employees and other stakeholders. The common denominator between a B Corp™ and Benefit Corporation is the shared belief that maximizing profit is not the sole mission of a business.

There is a distinction, however: The Benefit Corporation is a legal status offered in 41 U.S. states and the District of Columbia. It is akin to a C Corp or LLC. A B Corp is a third-party certification that has been granted by the non-profit organization B Lab™. There is a lot of overlap between the two, and in both cases, companies are making it clear the fiduciary duty of its officers and directors also encompasses employees and other stakeholders.

In any state where the Benefit Corporation legal charter exists (like California), a Certified B Corp must also take the step to change their legal designation to a Benefit Corporation as part of the certification. While clothing/gear brand Patagonia is perhaps the best-known B Corp, Bailard, Inc. is one of the newest, having achieved its B Corp Certification in 2023. There are currently nearly 8,000 B Corps in over 90 countries. The movement is growing.

Small Businesses, Big Impact

A company can incorporate as a Benefit Corporation at its outset, or convert later by amending its governing documents and meeting certain legal requirements. Historically, very few publicly listed companies have incorporated as Benefit Corporations (perhaps as few as three). Most, like Bailard, are smaller, privately held companies. That is not a deficit in the power of the B Corp movement, however.

Despite the dominance of large corporations, smaller companies are pivotal in the U.S. economy and its society. According to the Small Business Association (SBA), businesses with fewer than 500 employees account for 99.7% of all U.S. companies. They employ over 40% of domestic workers and have generated over 60% of net new jobs in the U.S. since 1995. Small businesses account for 44% of all U.S. economic activity.

The Power of Certification

In fact, the power of smaller companies to reshape the global economy for a broader set of stakeholders was a foundational piece of B Lab’s founding philosophy. Although the B Corp process is industry-agnostic, B Lab touts that companies in 162 industries have been certified, often in sectors that need it most. An academic study found a positive correlation between the number of B Corps in an industry and the prevalence of “shareholder-centric” policies within that industry, such as high layoff rates or significant pay disparities. The poorer these metrics are, the more likely it is that companies within the industry will pursue B Corp Certification.

For companies already aligned with the B Corp mission, certification is often more about publicly affirming what has been a private commitment to specific values. For Bailard, undergoing the certification process was more like looking in a mirror than looking at a map. As an independent, majority employee-owned, woman-led, majority women- and minority-owned, and community-focused company, the B Corp Certification was an affirmation of the company’s long-standing core values. However, the process does require a willingness to be evaluated publicly. It also provides a structure to codify corporate policies. The process to get certified is not easy. According to B Lab, only 40% of certification applications are successful, underscoring the principle that a B Corp must genuinely “walk the talk.”

Once committed, B Corps have shown a 96% retention rate. However, even for those choosing not to fully complete the certification, B Lab can provide resources. B Lab reported that over 240,000 companies used its assessment tool, which helps companies look at their own practices. At the center of the process is the B Lab Impact Assessment, which requires companies to score at least 80 out of 200 points to be certified, covering Governance, Workers, Community, Environment, and Customers. A fee based on company revenue is paid to B Lab to go through the process. Gathering all the required information and providing the documentation can be daunting and may take a full year.

Demonstrating Real Benefits

Evidence suggests the values attributed to being a Benefit Corporation strengthen a business. For example, during the challenging year of 2020, only 4.5% of B Corps failed, compared to 12.5% of American businesses overall. B Corps also report higher employee retention rates and a competitive edge in recruiting. Additionally, there is a growing number of key professional service firms in the space that want to work with other B Corps. Numerous studies have shown that consumers are very interested in the values behind the brands they buy or the companies they hire. To that end, B Lab provides a search engine for finding B Corps for consumers or business networking.

In an era of “greenwashing,” B Corps have completed a third-party assessment of key employee and sustainability metrics. Being a B Corp gives more gravity to the expressed values of a firm. Multiple studies show that Millennial and Gen Z employees—who currently make up 50% of the U.S. workforce—consider a company’s values when making purchases or choosing where to work.

A Commitment Beyond Profit

The rise of B Corps and Benefit Corporations signifies a shift in corporate philosophy, as it clearly reflects a commitment to specific values. But it is also more than that. It is a commitment to the idea that building stronger ties with employees and more sustainable business practices is the right way to conduct business going forward. Businesses that treat their employees poorly, or ignore environmental or reputational risks, are seldom the backbone of the community or industry outperformers. Nobel Prize-winning economic professor Robert Shiller summed it up well: “The B Corp movement is, to me, a product of a general improvement in our understanding of economic behavior. Through greater appreciation of the real motives that drive and excite people, B Corporations provide a significant new opportunity for investors. I think they could make more profits than any other types of companies….”

This paradigm shift towards more socially responsible and sustainable business practices is not just a trend; it’s the future of business. B Corps and Benefit Corporations are leading the way, proving that success in business can also mean success for shareholders, employees, and society more broadly.

1 The state of Delaware uses the term Public-Benefit Corporation (PCB) instead of Benefit Corporation.

2 https://www.forbes.com/sites/forbesbusinesscouncil/2022/03/25/how-small-businesses-drive-the-american-economy/?sh=2cd4a0304169

3 https://hbr.org/2016/06/why-companies-are-becoming-b-corporations

4 https://www.inc.com/ali-donaldson/why-a-record-number-of-business-owners-are-embracing-b-corps.html

5 Ibid.

6 https://www.federalreserve.gov/econres/feds/files/2020089r1pap.pdf