Chief Executive: "How to Set Strategy at the Speed of Disruption"

In Chief Executive, Sonya Mughal, CFA, discusses how leadership teams can adapt strategy faster amid accelerating disruption across technology, geopolitics, markets, and talent.

Social Security: It’s about more than when you claim

Social Security is often treated as a timing decision. Should you claim early, or wait?

That’s part of the decision, but it’s not the whole story. Even for those who may not rely on it, Social Security is one of the few sources of income that lasts for life and adjusts for inflation. How it’s claimed can shape retirement income over many years, particularly for a surviving spouse.

Putting Social Security in perspective

Before getting into the decision itself, it’s worth addressing a common concern.

Social Security is not going away. While the trust fund is projected to be depleted in the early 2030s, that doesn’t mean benefits disappear. Ongoing payroll taxes are expected to continue funding a substantial portion of benefits, currently estimated at roughly 75%, and historically, Congress has stepped in to adjust as needed.

For planning purposes, it’s reasonable to assume Social Security will remain part of the picture.

Framing the trade-off

There isn’t a single right answer here. What makes sense depends on your health, your income needs, and the resources you have available.

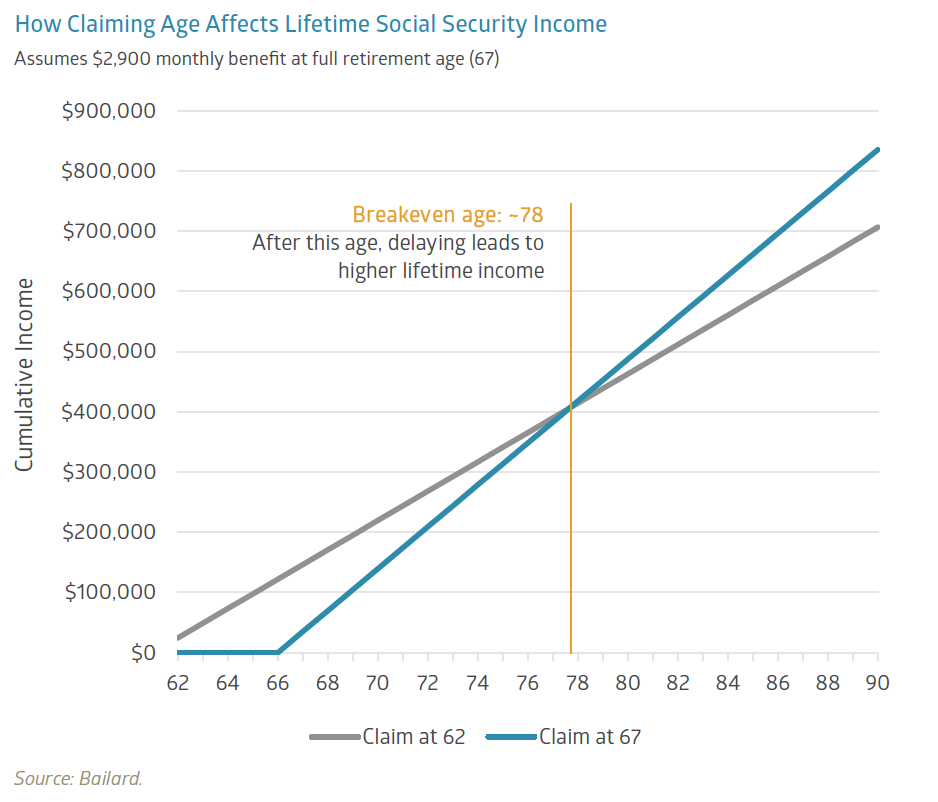

Health and family longevity are a natural place to start. If your health is poor or your family history suggests a shorter life expectancy, claiming benefits earlier may make sense. If you’re in good health, delaying benefits can meaningfully increase your monthly income over time. Claiming at age 62 can reduce benefits by up to 30% compared to waiting until full retirement age. On the other side, delaying beyond full retirement age can increase benefits by roughly 8% per year up to age 70.

One way to think about this trade-off is through the idea of a “breakeven age,” which compares total benefits over time based on when you claim.

In the example below, the breakeven point falls around age 78. If you live beyond that, waiting typically yields a higher total income. If not, claiming earlier may come out ahead.

The math may be helpful, but it’s only part of the story. It needs to fit within your overall plan, especially in how you’re drawing from other income sources. If you have flexibility early on, whether from taxable investments or retirement accounts, it may be easier to delay Social Security and increase your future benefit. When done thoughtfully, that approach can also help manage taxes and reduce required minimum distributions (RMDs) over time.

For couples

For married couples, the decision isn't just about one person.

For married couples, the decision isn't just about one person.

When one spouse has lower lifetime earnings, they may qualify for a spousal benefit of up to 50% of the higher-earner’s primary insurance amount (PIA). At the time of filing, Social Security evaluates both options and pays whichever is higher.

There are a few important nuances. Spousal benefits don’t increase beyond full retirement age, and claiming early reduces both the individual benefit and any spousal supplement.

Survivor benefits are where this becomes especially important. When one spouse passes away, the surviving spouse keeps the higher of the two benefits, including any increase from delayed retirement credits (which increase benefits for each year you wait beyond full retirement age, up to age 70). For many couples, that becomes the income floor on which the surviving spouse lives. When the higher earner delays, they increase their own benefit and, in turn, raise the income that remains in place for the surviving spouse.

Other situations to be aware of

Divorced individuals may also qualify for benefits based on a former spouse’s earnings record.

In general, the marriage must have lasted at least 10 years, the individual must be unmarried and age 62 or older, and their own benefit cannot exceed 50% of the former spouse’s PIA. In some cases, benefits may still be available even if the former spouse has not yet filed, as long as the divorce has been finalized for at least 2 years.

Widowed individuals may be eligible for survivor benefits as early as age 60, though those benefits are reduced if claimed before the survivor’s full retirement age. At full retirement age, the full survivor benefit becomes available.

There’s also some flexibility in how benefits are taken. In certain situations, it may make sense to start with a survivor benefit and switch to your own retirement benefit later, or the other way around, depending on which approach leads to higher lifetime income.

Taking a broader view

Social Security is one of the few sources of inflation-adjusted income that lasts for life. That makes it worth thinking about as more than just a timing play.

What matters is how it fits within your broader plan. Health, longevity expectations, income needs, and how your assets work together all play a role. Walking through a few scenarios and seeing how they unfold over time can help bring the right approach into focus.

# # #

Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Economic brief: AAPL…BA…CAT…

The ticker tape parade got its lofty beginnings high above Wall Street in late October 1886. In what was reportedly a spontaneous act, office workers tossed ticker tape out of their windows to celebrate the dedication of the Statue of Liberty. Pieces of ticker tape floated down amidst fog and rain as a crowd of nearly one million marched down to New York Harbor to watch the unveiling take place on what is now called Liberty Island. President Grover Cleveland spoke, months after tying the knot in the White House, and Lady Liberty was greeted with waving French and American flags, cannon blasts, and ringing church bells.

To date, lower Manhattan has hosted 209 ticker tape parades, according to the Downtown Alliance, most recently in 2024 for the WNBA champion New York Liberty.1 Perhaps the most famous parade through the Canyon of Heroes honored General Dwight D. Eisenhower in June 1945—following Germany’s World War II surrender—but the full list is a fascinating and somewhat eclectic walk through U.S. history, filled with champion athletes, adventurers, veterans, and visiting foreign dignitaries. In 1910, the first officially sanctioned parade was thrown for former president Teddy Roosevelt, upon the occasion of his return from a 15-month African safari!

Ticker tape is now a vestige of a bygone era, replaced both as a source of confetti and more consequentially as a means of communicating stock prices (via telegraph lines). In the late 1860s, the stock ticker machine revolutionized trading, enabling access to dramatically faster pricing data. It remained the standard for close to a century before being forced into retirement by computers, but its legacy lives on via the tickers (trading symbols) used to buy and sell stocks: the ubiquitous quotes crawling across the screen on CNBC and other financial networks. Commentators still refer to “the tape” when discussing stock prices and a review of the markets might be a “tale of the tape.” Some stocks are perhaps better known by the ticker (GOOGL, for example) than the company name (Alphabet).

Ticker tape is now a vestige of a bygone era, replaced both as a source of confetti and more consequentially as a means of communicating stock prices (via telegraph lines). In the late 1860s, the stock ticker machine revolutionized trading, enabling access to dramatically faster pricing data. It remained the standard for close to a century before being forced into retirement by computers, but its legacy lives on via the tickers (trading symbols) used to buy and sell stocks: the ubiquitous quotes crawling across the screen on CNBC and other financial networks. Commentators still refer to “the tape” when discussing stock prices and a review of the markets might be a “tale of the tape.” Some stocks are perhaps better known by the ticker (GOOGL, for example) than the company name (Alphabet).

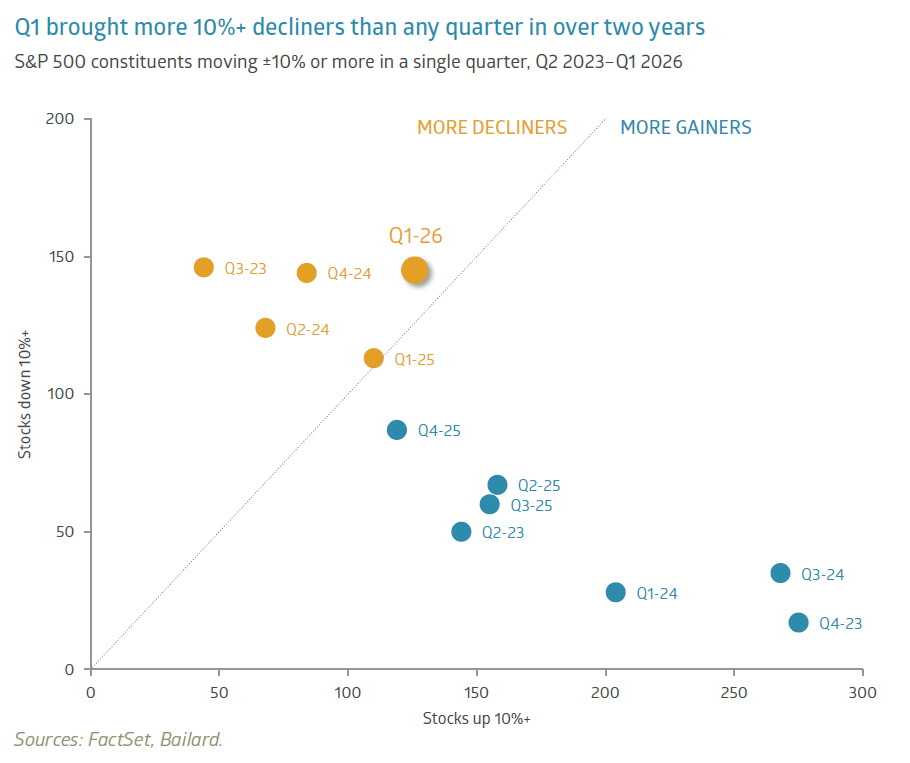

The current crop of Wall Street traders likely shredded some virtual ticker tape in the first quarter of 2026. Volatility picked up and not just the good (upward) kind. Within the Standard & Poor’s (S&P) 500 Index, 145 stocks declined by at least 10% in Q1, the highest level on that metric since 2023’s third quarter. At the other end of the spectrum, 126 stocks moved at least 10% higher, meaning that approximately 54% of the Index’s constituents experienced a 10% or greater price change for the full quarter. Both the Dow Jones Industrial Average (DJIA) and the NASDAQ Composite Index suffered a correction—a 10% decline from a recent peak—and these data points don’t fully capture the day-to-day volatility. In late February, analysts from Barclays PLC noted that single-stock volatility stood at about seven times that of the broader market, the widest divergence in at least 30 years.2 This was prior to the Iran war, in a market environment characterized by rapidly shifting sentiment on how AI will ultimately impact various industries. Lacking many answers on that front, investors rushed for the exits in certain areas (software) while piling into makers of memory chips and other groups perceived as near-term AI beneficiaries.

Straightjacket

Bombing Tehran did not settle the markets. It lit a fuse under commodity prices, sending the price of Brent crude oil soaring as high as $121 per barrel before closing the quarter up 69%. Only a few years removed from a punishing bout with inflation—which saw the Consumer Price Index (CPI) peak at roughly 9% year-over-year growth—markets expressed an immediate distaste for this development. The tape’s antagonistic relationship with elevated crude oil prices is nothing new. This unease seems likely to persist until the supply shock eases. Piper Sandler’s chief investment strategist, Michael Kantrowitz, put it bluntly: “It’s a single-variable market. If oil doesn’t go down, the market won’t go up – period.”3 Following a year in which gold stole the show, so-called black gold is headlining 2026 thus far and threatening to derail the promise of a stable price environment in which the Federal Reserve (the “Fed”) could further reduce its Fed Funds borrowing rate and spur economic growth.

In another echo of the post-pandemic economic landscape, supply disruptions have reemerged, with the potential to clog global growth. The Strait of Hormuz bottleneck affects roughly 25% of the world’s seaborne oil trade and almost 20% of global Liquefied Natural Gas (LNG) exports, according to the International Energy Agency (IEA).4 The impact extends far beyond energy, however. The Middle East plays a key role in supplying fertilizers, sulfur, methanol, helium, aluminum, and other non-oil commodities.5 Tariffs had already scrambled supply chains, but the Strait shutdown is exposing further vulnerabilities. Regarding AI, the Financial Times pointed out: “Investors have committed trillions of dollars to the technology, one of the most power-hungry inventions ever, on the assumption of ample energy supplies and a slick chip production line that can cross more than 70 borders before reaching the final consumer.”6 A prolonged impasse in the Gulf would act as a governor of sorts, limiting speed in a region that is an important gas pedal for the global economy.

Shortages are seemingly everywhere: labor, power, semiconductors…even mineral water? Coca-Cola announced that Topo Chico, its carbonated mineral water brand, won’t be available until later this year. The product is sourced from Monterrey, Mexico where Coca-Cola has encountered issues with the wells. Fed Chair Powell acknowledged in a recent talk at Harvard University that the Fed’s main tool—controlling interest rates—really only has an impact on demand, not supply.7 Thus, monetary policy has its limits in dealing with a supply shock such as the Gulf going offline. Instead, the Fed is focused on monitoring longer-term inflation expectations, which to this point have remained muted. As for actual inflation, the Federal Reserve Bank of Cleveland’s inflation “nowcast” estimates that CPI has moved up to around 3.4% year-over-year growth currently, roughly one percentage point higher than it was in February.8

The replacements

Policymakers also face a thorny task in evaluating the labor markets. The initial months of 2026 have seen a raft of layoff announcements, many of which are AI-related. Notably, Block, Inc. (symbol: XYZ), headquartered in Oakland, CA, announced it would lay off 40% of the company. CEO Jack Dorsey posted to X: “we’re already seeing that the intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working which fundamentally changes what it means to build and run a company, and that’s accelerating rapidly.”9 He was careful to emphasize that the decision was not made because the company is struggling, citing growing profits and profitability. Dorsey also predicted via a separate letter to shareholders that within the next year a majority of companies will reach the same conclusion and make similar structural changes. Minnesota-based logistics company C.H. Robinson has reduced its headcount by approximately 31% since 2022, replacing humans with hundreds of agentic AI agents that help process freight orders.10 The company says productivity has improved 40% over this timeframe.

Plenty of other companies have signaled intentions to significantly slash the workforce: Meta Platforms, Amazon, Oracle, and HSBC are just some of the downsizers. In January, U.S. employers announced more than 108,000 layoffs, the highest January level since 2009.11 Admittedly, certain industries have a bigger bullseye for the AI transition, and this trend hasn’t (yet) materially impacted aggregate labor statistics. It does, however, pose some hard societal questions in the longer term. A structurally higher unemployment rate could also weigh on consumer demand. In the meantime, corporations can benefit from reduced labor costs and downtime. The Fed recognized the potential for productivity gains in its latest “Summary of Economic Projections” by increasing the median estimate of longer-run real Gross Domestic Product (GDP) growth to +2.0% from +1.8% previously.

Higher turnover isn’t just affecting the low-end worker. According to The Wall Street Journal, roughly one Chief Executive Officer (CEO) in nine was replaced in 2025 across 1,500 of the largest publicly traded companies.12 That is the highest rate since at least 2010. To borrow from William Shakespeare: “Uneasy lies the head that wears a crown.” The heightened economic policy uncertainty could be a motivating factor for companies, along with the shifting sands caused by AI. Geopolitical concerns only add to a complicated decision matrix for corporate boards, particularly for firms with a global footprint.

Higher turnover isn’t just affecting the low-end worker. According to The Wall Street Journal, roughly one Chief Executive Officer (CEO) in nine was replaced in 2025 across 1,500 of the largest publicly traded companies.12 That is the highest rate since at least 2010. To borrow from William Shakespeare: “Uneasy lies the head that wears a crown.” The heightened economic policy uncertainty could be a motivating factor for companies, along with the shifting sands caused by AI. Geopolitical concerns only add to a complicated decision matrix for corporate boards, particularly for firms with a global footprint.

Equity markets have demonstrated resilience in the face of the volatility revival. A still healthy outlook for corporate profits deserves credit, with S&P 500 operating earnings per share growth projected at nearly 18% for 2026. If energy prices remain elevated, increased caution may be warranted, but the markets—like the Fed—are taking a wait-and-see approach overall despite the choppy waters. Wall Street is used to the tumult, after all, conditioned by many decades of upheaval and the occasional ticker tape parade to soften the blows.

# # #

1. “History of New York City’s Ticker-Tape Parades,” www.downtownny.com.

2. “Listless US Stock Market Masks Record Volatility Beneath Surface,” www.bloomberg.com, 2/21/2026.

3. “Wall Street Is Finishing the Worst Quarter for Stocks in Four Years,” www.wsj.com, 3/30/2026.

4. “Strait of Hormuz Factsheet,” www.iea.org, February 2026.

5. “The Strait of Hormuz crisis affects more than just oil. Here are 9 other commodities,” www.weforum.org, 4/1/2026.

6. “How the Iran war could derail the AI boom,” www.ft.com, 3/22/2026.

7. “Powell Says Private Credit Doesn’t Pose Systemic Risk,” www.bloomberg.com, 3/30/2026.

8. “Inflation Nowcasting,” www.clevelandfed.org, 4/3/2026.

9. “In a 600-word X post, Jack Dorsey justifies his decision to lay off 40% of Block’s workforce,” www.fastcompany.com, 2/27/2026.

10. “C.H. Robinson trims high-level managers as part of AI-driven cuts,” www.startribune.com, 3/30/2026.

11. “Layoffs in January were the highest to start a year since 2009, Challenger says,” www.cnbc.com, 2/5/2026.

12. “Companies Are Replacing CEOs in Record Numbers – and They’re Getting Younger,” www.wsj.com, 2/15/2026.

Past performance is no indication of future results. All investments involve the risk of loss. Please see the last page for important disclosures as well as index and category definitions.

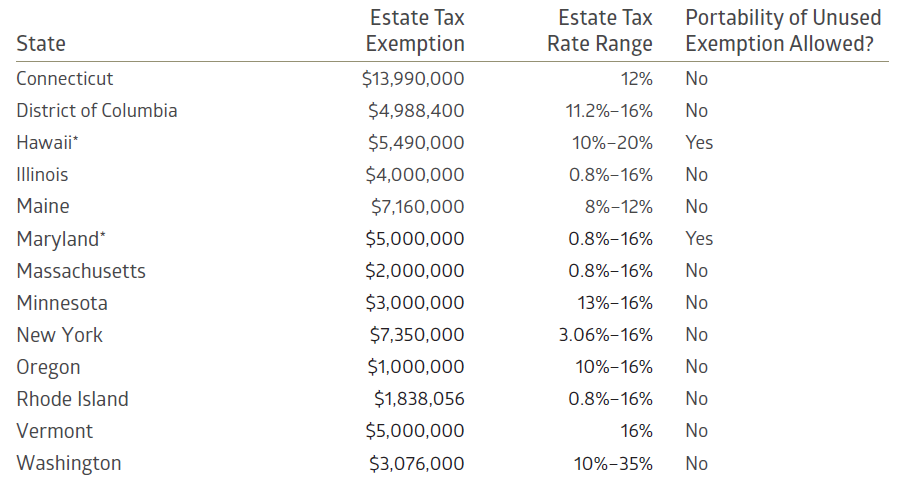

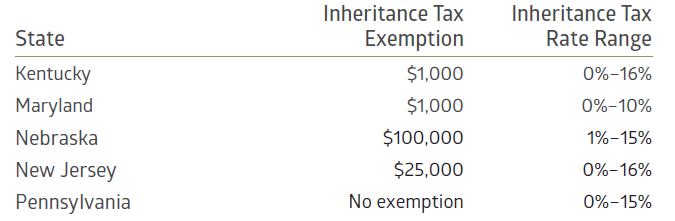

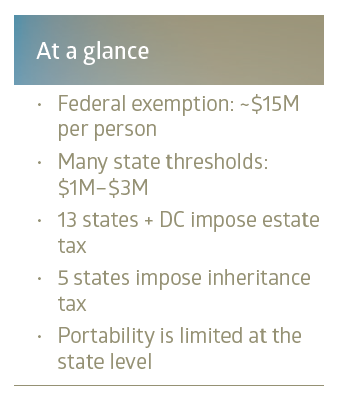

2026 state estate & inheritance tax overview

Several states impose estate or inheritance taxes at thresholds well below the federal exemption. Currently, 13 jurisdictions impose an estate tax, five states impose an inheritance tax, and Maryland imposes both. Because state rules and exemption levels change periodically, they should be confirmed before making planning decisions.

Estate tax states

Inheritance tax states

Inheritance tax rates and exemptions often vary depending on the beneficiary’s relationship to the decedent. Spouses are typically exempt, and many states provide favorable treatment for children or other lineal descendants, while higher rates may apply to extended family members or unrelated beneficiaries.

# # #

This summary is intended as a general reference point to support planning discussions. Exemption levels, tax rates, and rules may change periodically and should be verified before implementing planning strategies.

State taxes and the bigger picture in estate planning

Over the last several months, we’ve had a noticeable increase in questions about state estate and inheritance taxes. There’s good reason for that. Federal exemption levels have grown quickly, while many state thresholds have not kept pace.

Over the last several months, we’ve had a noticeable increase in questions about state estate and inheritance taxes. There’s good reason for that. Federal exemption levels have grown quickly, while many state thresholds have not kept pace.

As a result, these are not parallel systems. They operate differently, with lower thresholds, different rules, and outcomes that aren’t always obvious. That can change results more than expected.

The gap between federal and state planning

The federal estate tax exemption is now approximately $15 million per person. Many state exemptions sit far below that level, often in the $1 million to $3 million range.

That creates a disconnect. Many with moderate wealth may have no federal estate tax exposure, yet still face meaningful state-level taxes depending on where they live or what they own.

State systems also differ in how they treat married couples. While federal rules allow portability of a deceased spouse’s unused exemption, most states do not. Planning decisions that work well at the federal level may not translate cleanly to the state level.

Location drives the outcome

State tax exposure is not determined by a single factor.

Domicile is typically the starting point. The state considered your permanent home will often govern whether your estate is subject to tax. But other connections matter as well.

Owning real estate or tangible property in another state can create exposure there, even if you do not live in that state. In some cases, inheritance tax rules also depend on who receives the assets and where they reside. When there are multiple homes or long-standing ties to different states, these layers can overlap in ways that are not always intuitive.

How state rules vary

This exhibit highlights how varied these systems are: 2026 state estate & inheritance tax overview. A few patterns stand out:

- Several states impose estate taxes at relatively low thresholds, including as low as $1 million in some cases

- Tax rates can reach into the mid-teens or higher, depending on the state

- Only a small number of states allow portability between spouses

- A handful of states impose inheritance taxes, where the tax depends on who receives the assets rather than the size of the estate

The result is a patchwork. Similar balance sheets can face very different outcomes based solely on geography.

A different kind of tax: inheritance

A smaller group of states imposes an inheritance tax rather than, or in addition to, an estate tax. The distinction matters. Estate tax applies to the value of the estate itself, whereas inheritance tax is paid by the beneficiary, meaning the person receiving the assets is responsible for the tax.

Spouses are generally exempt. Children and other lineal descendants are often treated favorably. More distant relatives or unrelated beneficiaries may face higher rates. That makes beneficiary designations and trust structures an important part of the equation, particularly when planning across generations.

Liquidity can become a constraint

State estate and inheritance taxes are typically due within six to nine months after death. For estates that are primarily liquid, that may not present an issue. But when wealth is concentrated in real estate, private investments, concentrated stock positions, or closely held businesses, timing can become a constraint.

Without planning, decisions can be made under pressure, including the sale of assets at inopportune times.

Balancing planning trade-offs

Addressing state-level exposure often involves coordinating several moving pieces.

Trust structures, including credit shelter and QTIP trusts, can help align federal and state objectives. Charitable planning can also play a role, depending on overall goals and timing. At the same time, these decisions may affect income tax outcomes, including basis step-up considerations.

For married couples, the lack of portability in many states introduces an additional layer of complexity. Decisions made at the first death can influence both the surviving spouse’s tax exposure and flexibility.

In practice, planning becomes less about a single strategy and more about balancing trade-offs across tax, liquidity, and long-term goals.

Easy to overlook, important to address

State estate and inheritance taxes tend to sit outside the federal framework most planning focuses on. That makes them easy to overlook.

For those with multi-state ties, real estate holdings, or evolving residency, state estate and inheritance taxes can meaningfully affect outcomes. Reviewing state tax exposure alongside the broader plan helps ensure that structure, liquidity, and intent remain aligned over time.

# # #

Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Sonya Mughal Named Women in Wealth Advocate of the Year at 2026 Private Asset Management Awards

About Sonya Mughal

Sonya became Chief Executive Officer of Bailard in April 2021, after nearly three decades at the firm. She is the first woman and first person of color to lead the company. Her leadership is marked by consistency and fairness, along with a clear expectation that decisions be both thoughtful and well reasoned.

"Wealth management is stronger when more women are part of it. As advisors, as leaders, and frankly, as clients,” said Mughal. “I am deeply honored, but this truly belongs to the Bailard team. Nearly half of our senior leaders are women, and that is no accident. It is what happens when people are genuinely committed to doing what is right."

Women in Leadership at Bailard

As of December 31, 2025, 48% of Bailard's VPs and above are women. That figure speaks to steady hiring, promotion, and retention decisions over time.

One of the firm’s more tangible practices is pay transparency. Managers understand that compensation decisions must be clear and defensible. That discipline encourages open conversation and reduces ambiguity around advancement, an area where finance has not always been consistent.

For clients, that consistency supports stable teams and clear processes. For employees, it creates a more transparent path for growth.

“The conversations I have with clients are different here,” said Lena McQuillen, CFP®, Vice President and Director of Financial Planning at Bailard. “There is a level of trust that comes from working with a firm that genuinely walks the talk, and you really do get to make a difference in people’s lives.”

About the Private Asset Management Awards

The Private Asset Management Awards recognize firms and individuals across the private wealth management space. The 2026 awards ceremony brought together senior decision-makers from family offices, multi-family offices, private banks, and wealth management firms across the United States. Winners are selected by an independent panel of industry professionals.

In addition to Mughal’s individual recognition this year, Bailard’s Chief Investment Officer Dave Harrison Smith, CFA, was shortlisted for Manager or Investment Research Professional of the Year. The firm was also shortlisted in prior years for Best Philanthropic Initiative and Women in Wealth Advocate of the Year - Company.

About Bailard, Inc.

Bailard is an independent firm that has served individuals, families, and institutions since 1969 with comprehensive wealth management and disciplined asset management solutions. Our work is rooted in clear values, long-term thinking, and a steady commitment to putting clients first. Across the firm, we provide financial and wealth planning, portfolio management, and asset management strategies spanning domestic and international equities, fixed income, sustainable and responsible investing, private real estate, and customized mandates. The firm manages more than $7.7 billion in assets as of December 31, 2025.

Bailard is a Certified B Corporation™ and signatory to the UN Principles for Responsible Investing. We are built on accountability, compassion, and a long-term commitment to doing what’s right for our clients. Learn more at bailard.com, and explore career opportunities at bailard.com/careers.

# # #

Leadership statistics as of 12/31/2025. Bailard does not endorse or control, either expressly or implicitly, the content posted by any third party and disclaims all comments made or information provided by non-Bailard employees. These recognitions do not evaluate the quality of services provided to clients and are not indicative of Bailard’s future performance. There was no cost to enter. The Private Asset Management Awards 2026 judging process is designed to be rigorous and thorough to ensure all entries receive full consideration and that excellence in each of the categories is truly rewarded. A mix of leading wealth managers, advisors/consultants, service providers, and other industry experts make up the judging panel. Presented by With Intelligence, part of S&P Global, winners were announced in February 2026. Additional information is available here: https://awards.withintelligence.com/privateassetmanagementaward/en/page/2026-winners.

ComparisonAdviser: "How to Read a Financial Plan as a Client"

Lena McQuillen, CFP®, TPCP®, Vice President & Director of Financial Planning, weighs in on an article published by ComparisonAdviser.

How We’ve Stayed Steady

What stood out was the focus on execution. Decisions were made thoughtfully, and teams stayed engaged through uneven conditions. We continued to invest in our people and our processes rather than waiting for perfect clarity, and our independence gave us the space to be deliberate without the pressure to chase short-term outcomes.

Experience matters, and the colleagues leading our teams today have worked together for years. They’ve been through different cycles, learned alongside one another, and developed a shared way of working. When conditions shift, that experience shows up quickly in how decisions are made and how priorities are set.

Experience matters, and the colleagues leading our teams today have worked together for years. They’ve been through different cycles, learned alongside one another, and developed a shared way of working. When conditions shift, that experience shows up quickly in how decisions are made and how priorities are set.

That continuity is evident in our real estate platform. Nearly a year ago, Preston Sargent, longtime leader of Bailard’s real estate business, announced his intention to retire, allowing ample time to plan the transition with care. Effective January 1, Tess Gruenstein and James Pinkerton now serve as co-heads of the platform and as co-CEOs of the Bailard Real Estate Fund. Their partnership reflects years of working together, with complementary skills and a consistent approach to decision making. Alex Spotswood continues to drive acquisitions and portfolio management, and Preston remains involved as a strategic advisor, offering perspective shaped by decades of experience.

That same approach shows up across the firm. In 2025, Dave Harrison Smith, CFA, became Chief Investment Officer, drawing on his background and the collaborative way our investment teams operate. His promotion reinforced the direction already in place. In his first six months as CIO, Dave has helped bring even greater cohesion across the investment platform.

This all speaks to something simple. Decisions are being made by people who know the business, know the work, and know each other well. Trust is earned quietly, over time. Staying steady comes from the people in place and the way they work together.

# # #

Economic Brief: A Little Good News

Many years after hanging up his cleats in favor of a guitar, former linebacker Collins Obinna Chibueze still strikes a commanding presence under the bright lights. Standing 6'4", not counting the cowboy hat, the fast-rising singer better known as Shaboozey enjoyed a breakout year in 2024, earning him a “Best New Artist” nomination for last year’s Grammy Awards. The melodious Shaboozey moniker has its own football roots, dating back to when a high school coach slapped the name on his helmet as a phonetic reading of his surname. Shaboozey has been sounding it out ever since, blending country music with elements of hip hop, rock, and other influences. At their best, Shaboozey’s songs are playful and catchy while also introspective and questioning, built atop a bassline of human struggle.

His smash hit “A Bar Song (Tipsy)” spent 19 weeks as the #1 song on Billboard’s Hot 100 list and tied a record for the longest-running top hit in the chart’s history. It captured a mood that seems to persist today: “Gasoline and groceries, the list goes on and on, This nine-to-five ain’t workin’, why the hell do I work so hard?” That angst reverberates in another popular Shaboozey track called “Good News” that begins: “Man, what a hell of a year it’s been, Keep on bluffin’, but I just can’t win.” Although the song is a personal reflection it contains some deeply plaintive lyrics (“All I really need is a little good news”), which seem to match the melancholy we continue to see in consumer surveys. As one example, the University of Michigan’s Consumer Sentiment Index improved slightly in December yet had slumped ~29% over the past year and stood only marginally higher than its five-year low point—established in mid-2022 when overall U.S. inflation peaked at 9% year-over-year growth.

His smash hit “A Bar Song (Tipsy)” spent 19 weeks as the #1 song on Billboard’s Hot 100 list and tied a record for the longest-running top hit in the chart’s history. It captured a mood that seems to persist today: “Gasoline and groceries, the list goes on and on, This nine-to-five ain’t workin’, why the hell do I work so hard?” That angst reverberates in another popular Shaboozey track called “Good News” that begins: “Man, what a hell of a year it’s been, Keep on bluffin’, but I just can’t win.” Although the song is a personal reflection it contains some deeply plaintive lyrics (“All I really need is a little good news”), which seem to match the melancholy we continue to see in consumer surveys. As one example, the University of Michigan’s Consumer Sentiment Index improved slightly in December yet had slumped ~29% over the past year and stood only marginally higher than its five-year low point—established in mid-2022 when overall U.S. inflation peaked at 9% year-over-year growth.

It was undeniably a doozy of a year in 2025. Bloomberg columnist Clive Crook summarized it nicely: “Over the past 12 months, the U.S. has seen…every norm of economic policy—trade policy, fiscal policy, monetary policy—blithely tossed aside. At the same time, the U.S. economy stands at the bleeding edge of what might be as consequential an economic revolution as the transition from farming to manufacturing, or from manufacturing to services—except that the AI revolution could happen much faster.”1 Besides all that, 2025 was rather uneventful! The jump in economic uncertainty clearly did not dissuade the markets. It was, perhaps, another reminder that the stock market is not the economy. Investors heard sufficient good news to drive equity prices sharply higher for a third straight year. Critically, corporate profits did not disappoint: Standard & Poor’s (S&P) currently estimates that S&P 500 Index operating earnings advanced 13% per-share in 2025. That was the bottom line, but other tailwinds including lower interest rates, AI enthusiasm, and favorable tax policies also helped equities overcome numerous obstacles last year.

Amidst all the policy upheaval and a 43-day U.S. government shutdown—longest in history—investors learned to cope at times with a dearth of information from official government agencies. Beyond minding the information gaps, the August 2025 firing of Dr. Erika McEntarfer, commissioner of the Bureau of Labor Statistics (BLS), cast a shadow across the federal data landscape. Her dismissal immediately followed the Bureau’s July employment report in which the BLS sharply revised down its estimate of jobs added in May and June by a cumulative 258k. Whether or not the administration is correct that the “BLS is broken,” the optics of the decision did not go over well.2 In fact, handing McEntarfer a pink slip via social media hours after a disappointing jobs report may end up sowing more doubt. It prompted the Bloomberg Editorial Board to caution that “In so many words, this tells financial markets that official statistics are no longer to be trusted.”3 The ultimate consequences are unclear for the investment community as 2026 gets underway, but it may encourage decision-makers to rely more heavily on private sector data, where possible. Bloomberg’s Crook suggests that investors may be “flying blind” in an environment of heightened uncertainty and confusion over the state of the economy. For the financial markets, the adage “no news is good news” doesn’t typically apply.

Dot Com Club

A pivot to using more data from the private sector could easily start in Bentonville, Arkansas at Walmart’s global headquarters. The obvious reason: sheer scale. Walmart hauls in roughly 10% of all retail spending in this country, excluding automobiles.4 With around 2.1 million employees across 19 countries worldwide, Walmart amassed a staggering $681 billion of revenue in fiscal 2025—which in Gross Domestic Product (GDP) terms would put Walmart on par with countries such as Argentina and Sweden. Avoiding the company is a logistical challenge: 90% of the U.S. lives within 10 miles of a Walmart store.5 So when Walmart talks, the markets listen. In late November, Walmart reported its third quarter results, posting sales growth of ~6% and closer to a 7% advance for earnings per share (EPS). Perhaps more telling, outgoing CEO Doug McMillon said that U.S. customers and members are “still spending with upper and middle income households driving our growth.”6 McMillon acknowledged that lower income families have been under additional pressure, but also noted that like-for-like Q3 inflation was just 1.3% for Walmart US.

Technology has helped Walmart keep a lid on prices, consistent with their “Every Day Low Prices” mantra. According to CFO John David Rainey, the company’s supply chain investments have lowered delivery costs by 50% over the last two years. Tech workers now make up around a third of the corporate workforce.7 To compete with Amazon and other tech-forward retailers requires operating with the speed of a technology company. According to Bank of America, Walmart can now deliver within three hours to 95% of American households.8 Walmart has even introduced an artificial intelligence “retail companion” called Sparky on their website to answer product questions, synthesize reviews, and compare options. The focus on digital growth seems to be paying off. Walmart’s e-commerce business is now profitable and U.S. e-commerce sales have grown at >20% year-over-year in 10 of the last 11 quarters.

Technology has helped Walmart keep a lid on prices, consistent with their “Every Day Low Prices” mantra. According to CFO John David Rainey, the company’s supply chain investments have lowered delivery costs by 50% over the last two years. Tech workers now make up around a third of the corporate workforce.7 To compete with Amazon and other tech-forward retailers requires operating with the speed of a technology company. According to Bank of America, Walmart can now deliver within three hours to 95% of American households.8 Walmart has even introduced an artificial intelligence “retail companion” called Sparky on their website to answer product questions, synthesize reviews, and compare options. The focus on digital growth seems to be paying off. Walmart’s e-commerce business is now profitable and U.S. e-commerce sales have grown at >20% year-over-year in 10 of the last 11 quarters.

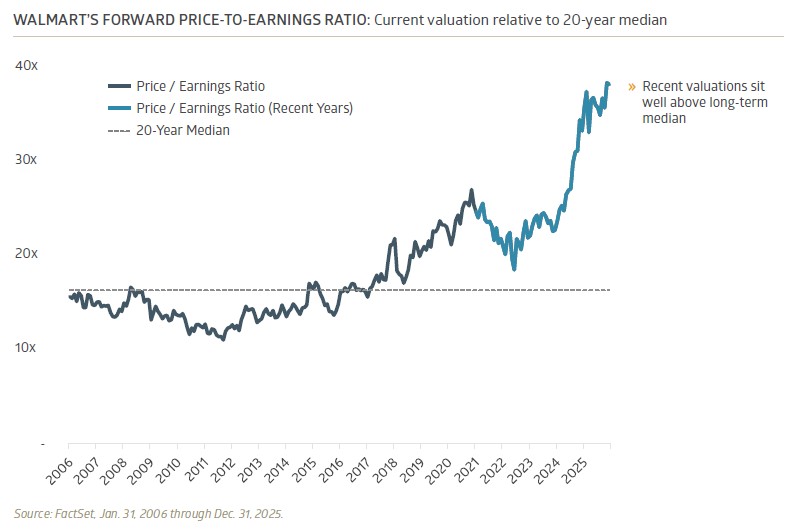

If Walmart as a tech company seems disorienting, consider that the world’s largest retailer just landed on the Nasdaq Stock Market. In December, after trading for over 50 years on the New York Stock Exchange, Walmart’s stock (WMT) migrated to the Nasdaq, joining companies such as Nvidia, Apple, Alphabet, and Microsoft. The exchange of choice for many tech companies, Nasdaq became the first U.S. stock market to trade online back in 1998. Walmart’s share price carries the sheen of a tech stock as well. After rising 23% last year, WMT finished 2025 trading at nearly 38x forward earnings, higher than many of its new Nasdaq peers.

Cold Brew

Although Walmart has managed to keep prices low via some alchemy of scale and technology, the overall inflation picture remains uncertain. Hot spots persist, including some high-profile areas. Electricity prices rose 6.9% year-over-year in November, per the BLS’s Consumer Price Index (CPI).9 Data centers are getting much of the blame, according to The Wall Street Journal, but hurricanes, wildfires, state renewable energy plans, and the replacement of aging or damaged grid equipment are all playing a role.10 California is feeling the pain more acutely than other states: power prices rose 35% inflation-adjusted over the 2019 to 2024 timeframe.

No area is getting more attention than health insurance costs. With the expiration of federal tax credits, the 24 million people that enrolled in coverage last year under the Affordable Care Act (ACA) will see their premiums increase significantly. San Francisco-based health policy organization KFF estimated that premium payments will more than double.11 For those covered under Medicare Part B, the 2026 standard monthly premium is going up nearly 10%. Employer-based health insurance is not immune, either. Mercer projects a total health benefit cost increase of 6.7% this year, pushing the average cost above $18,500 per employee.12 In 2025, Mercer’s annual survey found that the average cost of employer-sponsored health insurance rose 6%, driven in part by sharp growth in prescription drug spending with more companies including GLP-1 coverage.

At risk of burying the lead, though, coffee prices have been surging higher. For the many Americans who require a caffeine infusion to successfully back out of the garage each morning, this is a problem. Coffee prices soared 19% year-over-year, according to the November CPI report, and the restaurant point-of-sale company Toast calculates that the median price of a regular cup of coffee is about 20% higher than it was in early 2023.13 This has consumers trading down: cutting back on trips to the coffee shop and home-brewing instead. We can’t risk a caffeine crisis if this economy is to keep rolling.

At risk of burying the lead, though, coffee prices have been surging higher. For the many Americans who require a caffeine infusion to successfully back out of the garage each morning, this is a problem. Coffee prices soared 19% year-over-year, according to the November CPI report, and the restaurant point-of-sale company Toast calculates that the median price of a regular cup of coffee is about 20% higher than it was in early 2023.13 This has consumers trading down: cutting back on trips to the coffee shop and home-brewing instead. We can’t risk a caffeine crisis if this economy is to keep rolling.

Through all the noise, geopolitical tumult, and incertitude, Wall Street is uniformly optimistic. In fact, a year-end Bloomberg News survey found that all 21 strategists estimate the S&P 500 Index will post a fourth consecutive positive year in 2026.14 Wall Street analysts are estimating another strong year for corporate profits, as well, with S&P 500 earnings per share expected to increase by 14.8% on top of 2025’s already strong earnings growth.15 Again, the stock market is not the economy, but it does beg the question of whether everybody is gettin’ tipsy, to paraphrase Shaboozey. Another year of rising profits would certainly qualify as a little good news.

# # #

1 “Investors Are Flying Blind Into the ‘Golden Age,’ www.bloomberg.com, 12/26/2025.

2 “BLS Revisions Show President Trump Was Right – Again,” www.whitehouse.gov, 9/9/2025.

3 “Trusted Data Is a Vital Economic Asset,” www.bloomberg.com, 8/15/2025.

4 “How Walmart became a tech giant – and took over the world,” www.economist.com, 5/15/2025.

5 “Walmart, Inc.: Morgan Stanley Global Consumer & Retail Conference,” www.walmart.com, 12/2/2025.

6 “Walmart Inc. Q3 2026 Earnings Call,” www.walmart.com, 11/20/2025.

7 “Can Walmart Shed Its Discount Vibe?” www.nytimes.com, 6/23/2025.

8 “Heard on the Street: Should Walmart Really Be Trading Like a Tech Company?” www.wsj.com, 12/6/2025.

9 “Consumer Price Index for All Urban Consumers (CPI-U), Table 7,” www.bls.gov, 12/18/2025.

10 “Be Prepared to Keep Paying More for Electricity,” www.wsj.com, 12/29/2025.

11 “ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire,” www.kff.org, 9/30/2025.

12 “Mercer survey finds US employers and workers will face affordability crunch as health insurance cost is expected to exceed $18,500 per employee in 2026,” www.mercer.com, 11/18/2025.

13 “High Coffee Prices Are Changing How Consumers Take Their Daily Brew,” www.bloomberg.com, 12/16/2025.

14 “Every Wall Street Analyst Now Predicts a Stock Rally in 2026,” www.bloomberg.com, 12/29/2025.

15 FactSet, EPS One-Year Growth (%) estimated for year-end 2026, data retrieved 1/8/2026.

Specific investments described herein do not represent all investment decisions made by Bailard. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

CNBC: "Tech IPO hype gets drowned out on Wall Street by prospect of $1 trillion in debt sales"

Dave Harrison Smith, CFA, as source in a recent article published by CNBC.