Morning Macro with Dave - Hot CPI, cooler context

Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Hot CPI, cooler context

Dave Harrison Smith, CFA

Chief Investment Officer

May 19, 2026

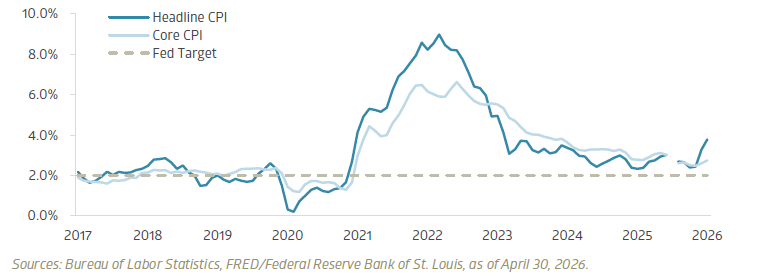

The pain of the post-pandemic surge of inflation remains fresh in investors’ minds. What was initially expected to be a transitory shock persisted far longer than many economists had estimated and eventually forced one of the most aggressive monetary-tightening cycles in more than 50 years. This, combined with the historical tendency for bouts of inflation to be followed by secondary or repeat waves, has left investors anxiously awaiting signs that the global energy crisis is beginning to seep into prices more broadly.

April’s inflation data came in hot and did little to quell concerns. Headline CPI rose 3.8% over last year, accelerating sharply for the second consecutive month. Core CPI, which excludes volatile food and energy prices, also came in above expectations, rising 2.8% from last year. On a monthly basis, headline CPI slowed to 0.6%, with the pace moderating modestly as energy price increases eased after a massive uptick in March. More concerning, however, was that monthly core CPI accelerated to 0.4%, a marked increase from March.

Headline and Core inflation remain elevated (2017-2026)

What drove the surprise

The headline numbers are challenging to digest, but the news may not be as bad as at first blush. A meaningful portion of the price increase was due to technical factors tied to shelter inflation. Due to the government shutdown last October, the Bureau of Labor Statistics did not collect semiannual rent-level data for a cohort and instead carried forward the previous month’s stale data. April’s report laps that temporary data, creating an artificial jump in shelter prices. Given shelter’s large weight in the CPI basket, the 0.6% monthly jump had a significant impact on overall inflation in April. Prior to this month, shelter prices had been rising at a relatively steady rate in the mid-to-high 2% range, indicating April’s figure was significantly inflated and suggesting that we are likely to return to a more normalized monthly pace in short order.

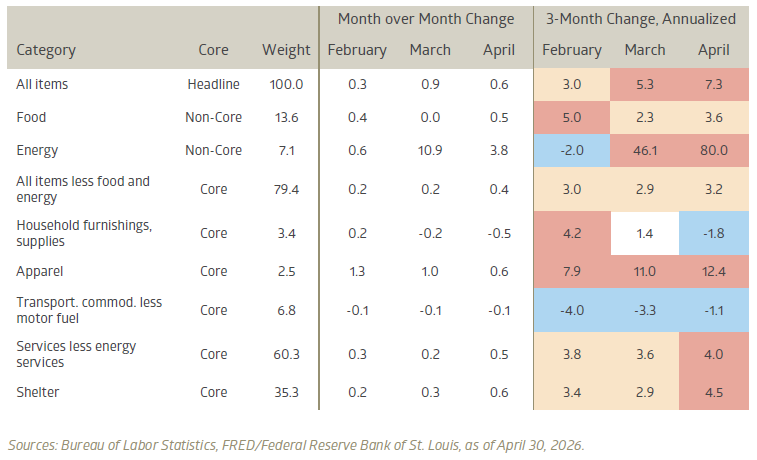

Select CPI components, month-over-month and 3-month annualized changes

Markets reprice inflation risk

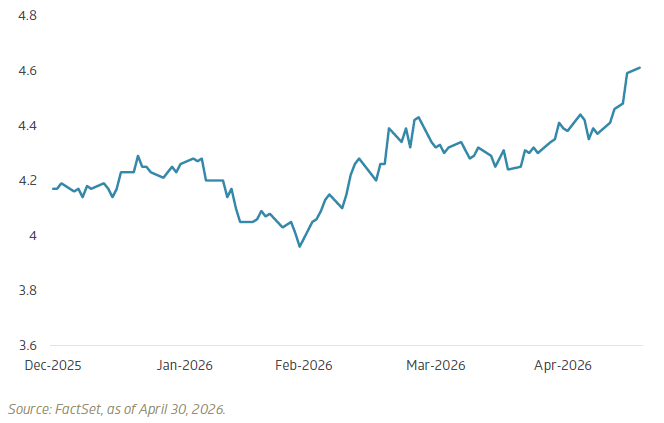

Still, the inflation print was a challenging one for bullish investors. Bond investors were quick to react, with the yield on the US 10-Year note rising to 4.62% on Friday. This represents a 45-basis-point increase since the start of the year (a basis point, “bp”, is 0.01%). Interest rate futures repriced meaningfully, as well, as the market positioning on futures now favors at least one rate hike by year-end. Outgoing Federal Reserve Chair Jerome Powell has consistently emphasized that interest rate tools are less effective against supply-driven inflation shocks such as the current energy crisis. Yet, we know that psychology matters, and that inflation fears tend to become self-reinforcing. The very prominent rise in gas prices may eventually seep into our collective psyche, and the slow creep of broad cost inflation may soon follow.

10-Year US Treasury yield (%) climbs on inflation fears

Duration matters

At the onset of the war in Iran, we admonished that the duration of the conflict would prove as important as the magnitude of the initial shock. The longer the crisis, the more painful the economic implications. We are beginning to see the effects of the conflict’s duration. Global governments have thus far relied on temporary mitigation measures to dull the pain, such as releasing oil from strategic reserves. We are beginning to discover the limits of these measures. Critically, inflation expectations appear to remain anchored despite price inflation beginning to filter into transportation, airline, and grocery prices. For now, at least, the market appears willing to accept that this bout of inflation is supply-driven and temporary. Just don’t call it transitory.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Quarterly International Equity Strategy Q1 2026

The quarter was a tale of two markets. January and February saw international equities continue their 2025 outperformance. In March, that trend gave way to a major geopolitical shock from military strikes in the Middle East. The effective closure of the Strait of Hormuz triggered a severe energy crunch, and related knock-on effects for countries and sectors.

Morning Macro with Dave - When talented people experiment

Morning Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

When talented people experiment

Dave Harrison Smith, CFA

Chief Investment Officer

May 12, 2026

When talented people are given room to experiment, it is striking how quickly creativity can compound.

We typically reserve the Morning Macro note for economic news, market developments, and the forces shaping portfolios and financial affairs. This week, we’re taking a slight detour to talk about something happening closer to home: Bailard’s inaugural Hackathon, which concluded with its first demo day yesterday.

Like many worthwhile ideas, this one had humble origins. In an early morning conversation fueled by too much caffeine, several team members found themselves discussing the extraordinary pace of recent technological change. Each week seemed to bring another leap forward in the capabilities of artificial intelligence. The question quickly became: how could Bailard embrace this wave of innovation in a thoughtful, hands-on way? How could we better understand what these modern AI tools can actually do?

We decided to form two internal teams. Each team’s structure was intentionally cross-functional, mixing coworkers who rarely work together and combining engineers with client-facing professionals and research analysts. The teams were not competing in any way. Instead, we wanted to pursue multiple projects, learn independently, and share ideas through regular check-ins along the way.

The assignment itself was intentionally broad: take modern AI tools, find a problem within Bailard, and build something cool. What followed over the next two weeks exceeded even our most optimistic expectations.

Conference rooms were quickly filled with sticky notes. Teams huddled over laptops, energetically sketching and debating. Prototypes circulated throughout the firm for feedback, then were iterated, adjusted, and reworked in unexpected ways. One of the tremendous benefits of recent developments in AI is the ability to rapidly prototype ideas, allowing teams to compress weeks of development into mere hours and enabling rapid testing and iteration.

At yesterday’s demo day, the energy was palpable. What began as a learning exercise had clearly evolved into something much larger: a demonstration of unleashed creativity and collaboration. New ideas emerged as the group saw what others had built. Prototypes were re-imagined as production applications. The number of “that’s so cool!” and “wow!” moments may have broken a company record.

Our goal at the outset was never to build polished, production-ready applications. Instead, it was to learn by doing and better understand both the capabilities and limitations of these emerging tools. The fact that both teams created several applications remarkably close to real-world deployment was an added benefit.

From here, we plan to step back and evaluate what comes next. But one conclusion is already clear: the teams’ capabilities advanced dramatically in a remarkably short period.

I left the demo day energized and deeply appreciative. Once again, I was reminded of the creativity, curiosity, and capability of my Bailard colleagues. Innovation requires room to experiment, collaborate, and occasionally surprise yourself. Given that opportunity, it is remarkable what talented people can build together.

I’m incredibly grateful to work alongside a team willing to learn, experiment, and push themselves in new ways. I can’t wait to see what we build next.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Chief Executive: "How to Set Strategy at the Speed of Disruption"

In Chief Executive, Sonya Mughal, CFA, discusses how leadership teams can adapt strategy faster amid accelerating disruption across technology, geopolitics, markets, and talent.

Monday Macro with Dave - A cooler labor market with steady underpinnings

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

A cooler labor market with steady underpinnings

Dave Harrison Smith, CFA

Chief Investment Officer

May 4, 2026

Cooling but stable

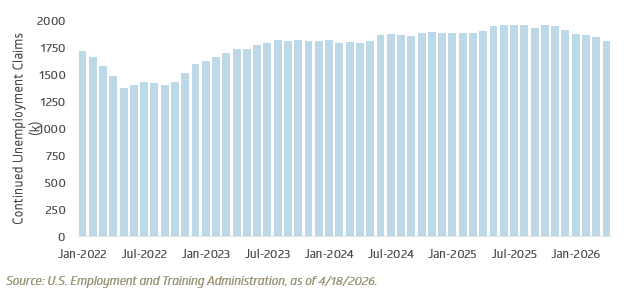

A central question for investors over the past year has been the health of the U.S. labor market. Concerns peaked in early 2025 as tariffs weighed on corporate activity and hiring slowed. Uncertainty resurfaced following the dismissal of Bureau of Labor Statistics head Erika McEntarfer after a July jobs report that included sizable revisions, raising questions around data reliability. Despite the noise, the underlying signal is one of stabilization at a relatively cool but constructive level.

Composite labor data support that view. Continuing unemployment claims, which reflect individuals receiving benefits after an initial claim, have trended modestly lower in recent months and reached their lowest level in two years in April. Flat to slightly declining claims point to a labor market that is no longer tightening but not meaningfully deteriorating either.

Data on net hires from private sources such as ADP show a similar pattern. Hiring has slowed but remains steady, with a three-month average of just over 49,000 net new jobs added monthly since August 2025. While well below the pace seen in 2024, this level is consistent with a more stable backdrop, particularly as labor force growth has slowed alongside lower net immigration.

All told, we have increased confidence in a cool but stable labor backdrop, which should remain broadly constructive for markets. That said, the aggregate data continues to mask pockets of weakness. New graduates, younger workers, and certain sectors are facing more pressure. Even so, from a broad macro perspective, the labor market appears relatively steady.

Continuing unemployment claims point to a stable labor market

Capital earnings remain strong

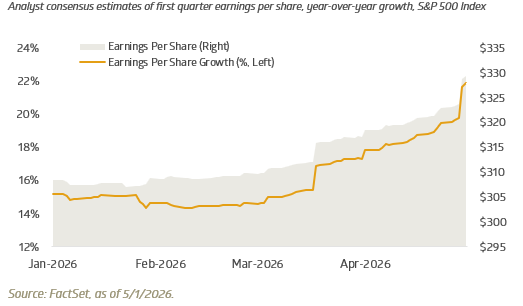

Far from steady and cool, corporate earnings are absolutely booming.

With 66 percent of the S&P 500 reporting first-quarter results, earnings per share are tracking to grow 25 percent year over year, the strongest pace in several years. Adjusting for other income in select technology companies, which reflects gains tied to private equity stakes, growth is still tracking at a solid 16 percent. Strength is most evident in Energy, Information Technology, and Industrials, supported by higher energy prices and early returns on investment in artificial intelligence.

S&P 500 earnings growth remains solid

Importantly, growth is not limited to a narrow group of companies. The median S&P 500 constituent is tracking to grow earnings before interest and taxes at 11.2 percent in the first quarter, pointing to broad-based strength. Earnings breadth remains an important support for markets, particularly given the increasingly concentrated nature of index performance.

With more than one-third of companies yet to report, including many small and mid-cap firms, we continue to monitor results closely. Risks remain, especially if elevated energy prices begin to weigh on consumer behavior and feed into core inflation. Even so, a key pillar of market support. corporate earnings growth. appears firmly intact.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Tax refunds rise 11%, providing important tailwind to consumers

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Tax refunds rise 11%, providing important tailwind to consumers

Dave Harrison Smith, CFA

Chief Investment Officer

April 27, 2026

Tax refunds provide a timely cushion

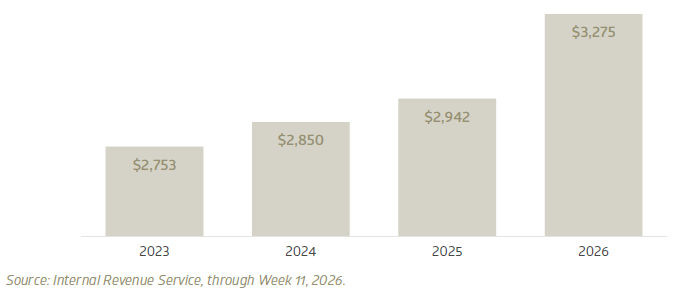

Tax Day is behind us, and the latest data from the IRS gives us a new read on a source of economic support: tax refunds. This year, the increase in average refund size is meaningful and provides a temporary tailwind for consumers. The average refund in 2026 rose to $3,275, a strong increase of 11.3% over last year. Total refunds rose to $296.1 billion, up $43.0 billion over last year.

Average refund per tax filing

These refunds have come at a critical time for the consumer. Gasoline prices remain elevated with national averages above $4.00, up nearly a full dollar from a year ago. This has acted as an additional tax on American consumers. To date, high-frequency spending data has been relatively resilient, suggesting consumers have absorbed the energy shock. Refunds have clearly played a role. The risk remains that, as the benefit of tax refunds wanes, consumers may feel more of the pinch and pull back their spending in unanticipated ways.

Capital spending remains a source of strength

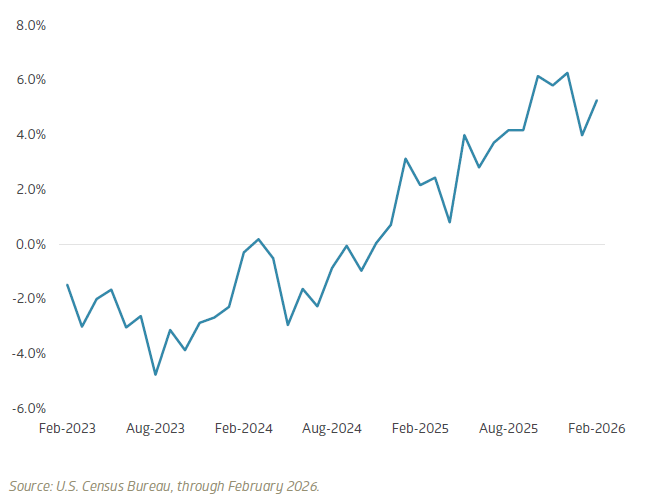

Consumer spending has been a steady pillar of U.S. economic strength in recent years. The other, undoubtedly, has been corporate investment. Data from the U.S. Census Bureau Durable Goods report highlights the trend. Growth in Non-Defense New Orders, often seen as a proxy for corporate capital expenditures, has continued to post strong monthly and annual growth in 2026, building on a trend that began to accelerate in 2024.

Non-defense new orders, core capital goods

Much of this boom can be attributed to robust investment in artificial intelligence, including data centers and equipment. The key question is durability. Over the coming weeks, we expect to receive several earnings reports that will provide an important signal about the trajectory of AI capital spending. Expectations are elevated, but recent updates from major infrastructure providers have broadly reinforced confidence in the continued build-out.

Energy prices remain the key risk

Overall, the early read is one of continued resilience in the face of global volatility. U.S. consumer data continues to suggest stability, with the benefit of tax refunds helping offset the pain of the energy shock. The labor market is cool but looks to be stabilizing. This, combined with strong capital spending, has supported the U.S. stock market. The durability of the consumer and capital spending is critical to continued strength. Continued elevated energy prices remain a key risk, as higher prices filter through to inflation expectations and erode spending.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Consumer resilience meets rising energy costs

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Consumer resilience meets rising energy costs

Dave Harrison Smith, CFA

Chief Investment Officer

April 20, 2026

Tracking the consumer spending response to higher gas prices

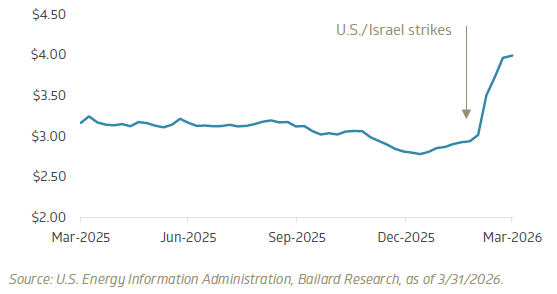

The early transmission of the war in Iran into the U.S. economy has been through gasoline prices. Prices rose a stunning 35.9% from late February through March. This move represents the largest five-week surge since the U.S. Energy Information Administration began tracking the data in 1991. Average national prices have remained elevated in April, hovering near $4.00 per gallon.

National U.S. regular retail gasoline price, trailing year

With several weeks of data now available, we can begin to track the early impacts on consumer spending trends. Studies have found that gasoline demand has historically been relatively inelastic; consumer demand for gasoline does not change significantly despite changes in gasoline prices. Instead, the adjustment typically comes through reallocation of wallet share, with consumers decreasing spend in other categories. Luxury goods and discretionary purchases in particular can come under pressure.

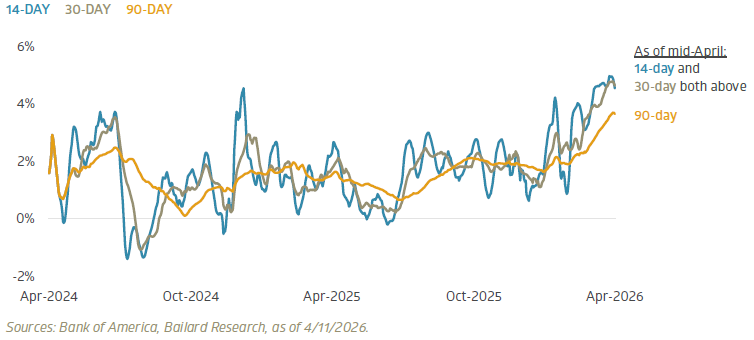

So far, the consumer spending reaction to higher gas prices has been limited. Analyzing near-real-time credit card spending data from Bank of America, overall spending remains resilient through mid-April, with both the 14-day and 30-day moving averages for total card spending above the 90-day average, suggesting a modest acceleration in spending behavior rather than a slowdown.

Credit card spending: 14-, 30-, and 90-day moving averages vs. prior year

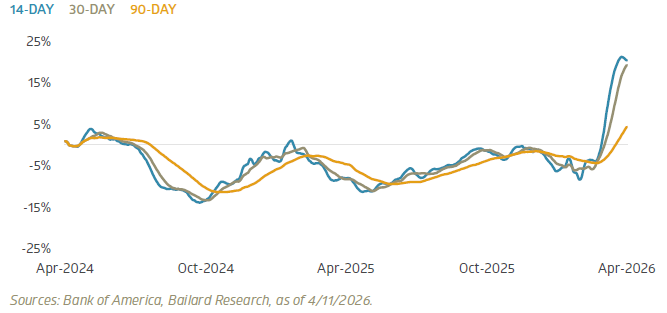

Unsurprisingly, spending at the pump has surged. The 14-day moving average of gasoline outlays is up more than 20% versus last year. Notably, this is below the average increase in gasoline prices, suggesting a modest change in consumer behavior.

Gasoline spending: 14-, 30-, and 90-day moving averages vs. prior year

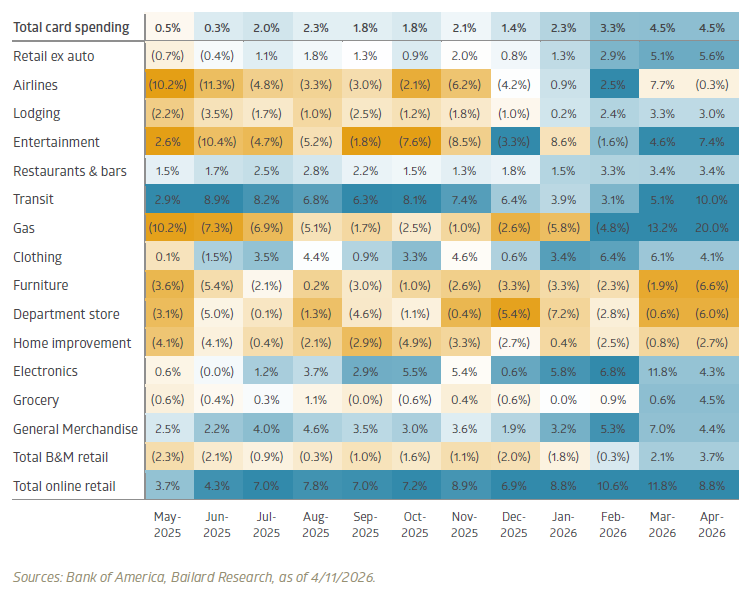

Other categories generally look on trend. Below we show the year-over-year change in average monthly spend, broken down into broad spending categories. Discretionary spending, including general merchandise, clothing, and entertainment categories, continues to track in line with prior trends. Online retail spending, as well, looks firm.

Notably, spending on airlines appears to be an exception. Airline spending reflects a sharp increase in March, followed by a significant slowdown in April. This may reflect a pull-forward in demand, with consumers anticipating rising airfares and booking summer trips early to lock in lower prices. Whether this proves to be a temporary shift or an early sign of demand destruction is an area to monitor going forward.

The broad takeaway is that consumers have remained resilient despite considerable geopolitical and economic volatility. The key question is the duration of that strength. The longer elevated energy prices persist, the greater the economic impact on both inflation and consumption, and the greater the risk that higher costs begin to erode relative resilience.

Retail category year-over-year change heatmap

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.