Bailard's SRII Issue Research & Outreach Library

The 2023 proxy season: More shareholder proposals, tougher proposals, and less support.

Monday Macro with Dave - Inflation picks up as labor market trends begin to diverge

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Inflation picks up as labor market trends begin to diverge

Dave Harrison Smith, CFA

Chief Investment Officer

April 13, 2026

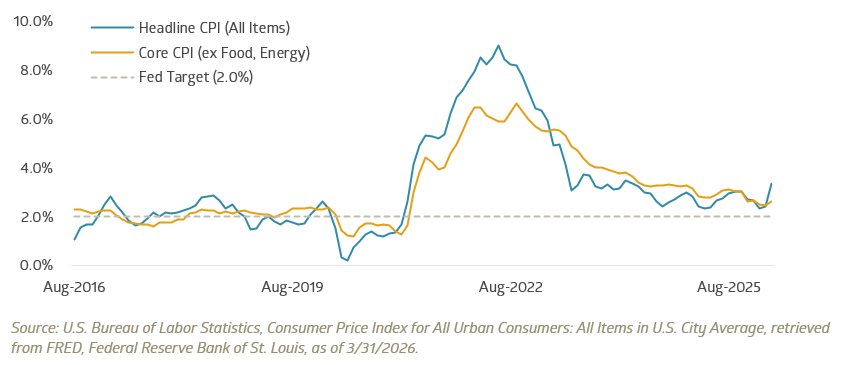

Headline inflation jumps but Core holds

On Friday, the Bureau of Labor Statistics released its March CPI report, among the first to reflect the impact of rising energy and gas prices following the strikes on Iran at the end of February.

At first glance, the report came in broadly in line with expectations or even slightly cooler than feared. Headline CPI jumped to 3.3% year-over-year, up from 2.4% the prior month. Core CPI, which excludes volatile food and energy prices, was slightly cooler than expected, aided by a decline in used-car prices.

Core and Headline CPI year-over-year change

The influence of the war in Iran was evident in the data, with energy prices increasing by 12.6% versus last year and gas prices rising by 21.2%. As expected, pass-through to core CPI was more limited, though signs of impact are beginning to emerge at the margin in the form of prices of delivery services and airfare, which rose 3.1% and 2.7% year over year, respectively.

The broad takeaway is that this report is unlikely to shift the Fed’s stance of holding interest rates at current levels. The pressure on consumers remains, with lower-income consumers particularly hard hit, given their higher share of gasoline spending. The longer the conflict extends, the greater the risk these costs transmit to slower spending growth and higher core inflation, as companies raise prices to offset higher input costs.

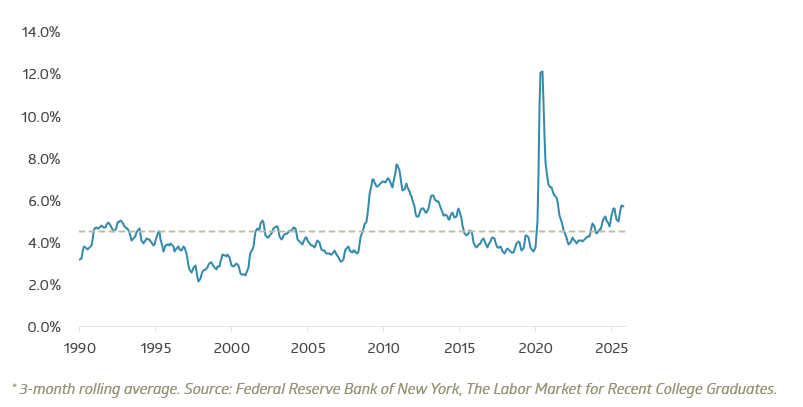

Labor market for early-career Americans showing weakness

Last week’s labor market data continued to indicate a stable yet cool job market. Beneath the surface, however, is an increasing divergence in prospects for early-career workers.

The Federal Reserve Bank of New York recently published new data dissecting unemployment trends for various cohorts of the U.S. labor force. Of particular note was the unemployment rate for new college grads, which has been steadily rising since 2022 and reached 5.6% at 2025 year-end. That level is significantly above historical average and elevated for non-recessionary periods.

Unemployment rate for recent college graduates, smoothed*

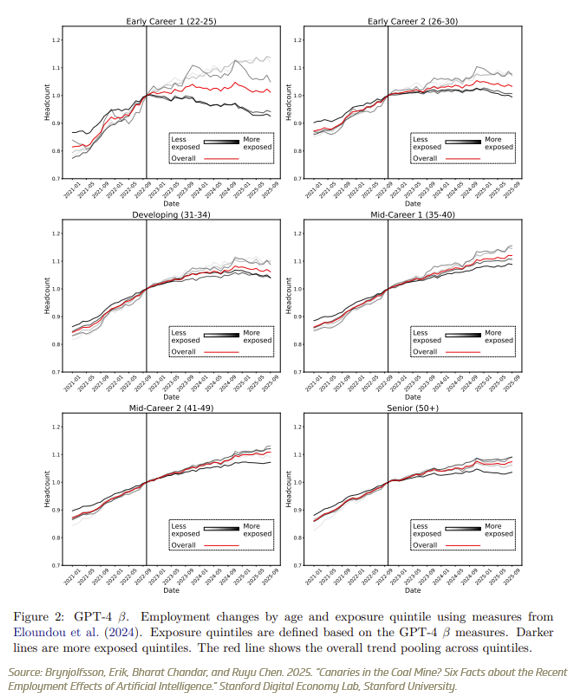

Concurrently, research from the Stanford Digital Economy Lab, published by Erik Brynjolfsson et al, examined the impact of artificial intelligence on labor. Their team focused on the growing divide between roles defined as more or less exposed to AI automation. Their findings point to a growing divergence in outcomes, specifically concentrated in early-career employees in AI-impacted roles.

Employment changes by age and level of exposure to AI, from Stanford Digital Economy Lab

For any of us with children, nieces, or nephews entering the workforce, these findings may come as no surprise. The job market is tough out there for this cohort of the American labor force. While the aggregate labor market looks relatively healthy, AI does appear to be impacting certain segments. The implications for our economy and society are worth monitoring closely.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Rising energy costs and a cooling-but-steady labor market

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy costs and a cooling-but-steady labor market

Dave Harrison Smith, CFA

Chief Investment Officer

April 6, 2026

Energy prices and consumer squeeze

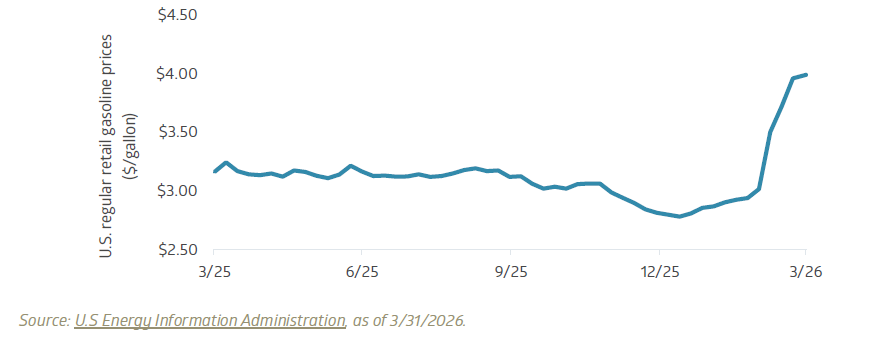

Gas prices are moving higher again today. This has been one of the clearest transmission channels from the war in Iran into US markets. The surge in March saw gas prices rise from a national average of $2.94 to $3.99. This five-week move represented a 35.9% increase, the largest five-week increase since the Energy Administration Agency began tracking the data in 1991. Price pressures have continued into April, further compounding this move.

Average national retail gasoline prices, regular blend

Consumer response to higher gas prices is a well-studied phenomenon. Studies have found that gas demand itself is relatively inelastic; in non-economist speak, that means consumers do not purchase more/less of a good if the price decreases/increases. Households still need to commute, families need to run errands, and folks still maintain daily routines. Rising gas prices have historically had little impact on driving behavior.

Where adjustment does occur is in the consumption basket, specifically in reduced purchasing behavior for non-discretionary goods. As gas prices rise, it pinches consumer wallets, particularly for lower- and middle-income households. Studies have shown that consumers reallocate spending away from areas such as leisure, out-of-home dining, and retail goods. This can explain some stock reactions in March as gas prices spiked, particularly among companies more exposed to these sectors and among lower-income households.

Consumer and retail spending have been a central pillar of U.S. economic growth over the last decade. The impact of changes in consumer spending can thus have a meaningful effect on growth, with the initial impact likely to be felt in discretionary spending. Further, the rapid shift threatens to dim consumer outlook on finances and erode consumer confidence. Any sustained pressure over a long period of time threatens to become a broader economic headwind.

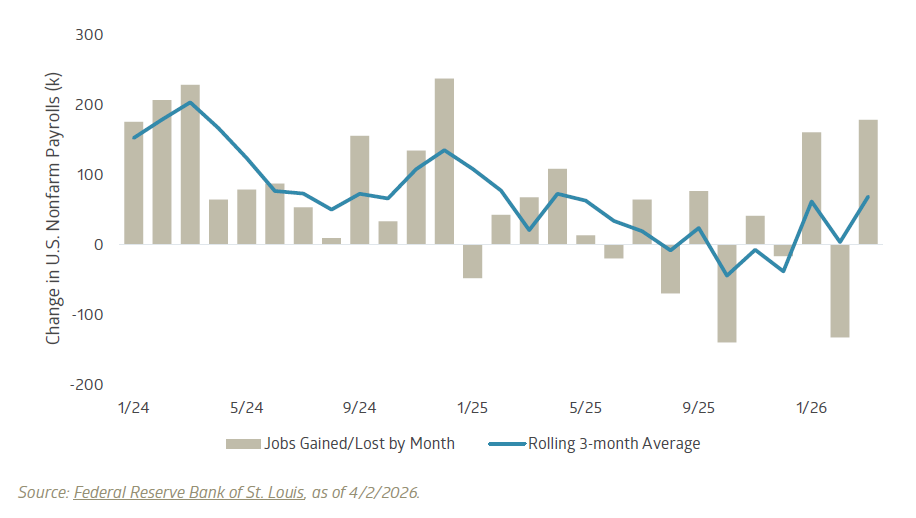

Jobs report: A strong number, though outlook remains uncertain

Last week, we highlighted a key data release: the Bureau of Labor Statistics Nonfarm Payrolls report, which many view as an estimate of net job creation in the U.S economy. February’s print, published in early March, had come in well below expectations, showing a decline of 133 thousand jobs versus expectations of a modest gain. We noted that this was in contrast to several other labor market indicators, such as continuing unemployment claims and private-sector employment estimates, which had indicated greater stability. As a result, we were focused on this data release to confirm or refute the February weakness

The March report surprised to the upside, with payrolls increasing by 178,000 jobs, well ahead of expectations of approximately 60,000.

Broadly, this data reinforces our view that the labor market is cooling but not cracking. The moving three-month average of jobs gained has turned modestly positive after a softer period in the second half of 2025. Importantly, this level of job creation should be consistent with a stable unemployment rate, currently in the low 4% range, particularly in the context of the country’s recent shift to lower net immigration and reduced population growth.

In isolation, this report would be encouraging for the Federal Reserve, suggesting that the labor market remains on solid footing. Yet the background is anything but static, and the high degree of uncertainty stemming from both the war in Iran and rapid advances in artificial intelligence raises the difficulty of forecasting the labor market outlook. Against this context, the takeaway is straightforward: this was a relatively strong report, even if the broader path remains uncertain.

Change in BLS Nonfarm Payrolls by month, rolling 3-month average

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Parsing signals from noise in job reports and the labor market

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Parsing signals from noise in job reports and the labor market

Dave Harrison Smith, CFA

Chief Investment Officer

March 30, 2026

Markets are increasingly pricing in a more prolonged Middle East conflict and sustained pressure on energy prices. Our focus remains on how that transmits through to markets and portfolios. A key starting point is the condition of the U.S. economy heading into the conflict.

This week’s data, including retail sales, ISM manufacturing, and labor reports from ADP, Challenger, and the Bureau of Labor Statistics (BLS), should help establish that baseline.

Last month’s Nonfarm Payrolls report from the BLS missed expectations by a wide margin, showing a decline of 92,000 jobs versus forecasts for a modest gain of 55,000. The release raised concerns about labor market weakness heading into the Iran conflict and briefly reignited discussion around “stagflation.” It also ran counter to the prevailing view that the labor market was cooling, but not breaking.

Payroll miss likely reflects strikes and weather, not a trend break

Importantly, the February BLS data included several one-time distortions, including labor strikes and severe weather. Other indicators, such as ADP data and unemployment claims, have shown more resilience in recent weeks. That said, layoffs have picked up at the margin, with announcements from UPS, Meta, and Amazon in the first quarter. The next BLS report, due Friday, will carry added weight.

Stagflation concerns in context

Concerns around stagflation have risen sharply in recent weeks. Defined as weak growth alongside elevated inflation, the concept remains anchored in the oil shocks of the 1970s.

Federal Reserve Chair Jerome Powell pushed back on that comparison following last week’s Federal Open Market Committee (FOMC) meeting, noting today’s backdrop of roughly 3% inflation and 4% to 4.5% unemployment stands in stark contrast to the double-digit levels seen in that era. As he put it, “I would reserve the term stagflation for a much more serious set of circumstances. That is not the situation we’re in.”

Still, the tension is real. The Fed’s dual mandate is being tested by an energy shock that could push inflation higher while weighing on growth. That dynamic has been enough to pressure equity valuations, even as earnings expectations remain strong. With valuations already elevated, there has been little room for error.

As Kenneth Rogoff noted in the Financial Times:

“Coming on top of the ongoing Ukraine and tariff wars, the Iran war is shaping up as the biggest stagflationary shock the world has seen in five decades.”

Rising deficits, rising yields, fewer hedges

Global bond yields have continued to trend higher since the onset of the Iran conflict. Last week saw the U.S. 10-year reach 4.44%, Germany’s bund rise to 3.10%, and Japan’s JGB to 2.34%, while the U.K. gilt was a modest exception, easing slightly to 4.92%.

Deficit concerns remain front and center. The U.S. was already projected to run deficits of 5% to 7% of GDP in the coming years. Add higher energy prices, geopolitical uncertainty, and policy constraints, and confidence in those projections has started to erode.

The result is a more challenging environment for diversification. Equities have faced valuation pressure, while bonds, typically viewed as a ballast, have also struggled as yields rise and prices fall. The Bloomberg Aggregate Index is down 2.49% month-to-date and 0.79% year-to-date. Modest in absolute terms, but notable given the volatility elsewhere.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Country Indices Flash Report – March 2026

U.S. and Israeli strikes on Iran disrupted shipping through the Strait of Hormuz, a key energy chokepoint. Equities fell, while oil and gas prices spiked. [[ READ MORE ]]

Monday Macro with Dave - Markets reprice on rapid policy shifts

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Markets reprice on rapid policy shifts

Dave Harrison Smith, CFA

Chief Investment Officer

March 23, 2026

Policy signals are driving market swings

Markets have swung sharply over the past 72 hours, driven less by fundamentals and more by policy signals.

Late Friday, oil prices surged on news of escalation in the Middle East, alongside President Trump’s threat of potential strikes on Iranian energy infrastructure. By early Monday, that tone reversed, with a pause on military action following reported discussions with Iranian counterparts. Iran has since pushed back, denying meaningful progress.

This kind of whiplash is not new. It echoes April 9, 2025, when markets sharply rebounded after a sudden tariff reprieve. The S&P 500 rose 9.5% in a single session. Policy-driven reversals can be abrupt and non-linear. A single tweet can move mountains.

Oil markets are still pricing a de-escalatory base case, with futures below $80 per barrel by year-end and closer to $70 by late 2027. That baseline remains vulnerable to escalation, infrastructure damage, or a more prolonged conflict.

Crude oil WTI futures pricing remains below escalation scenarios

Rising oil prices are already showing up in bond markets

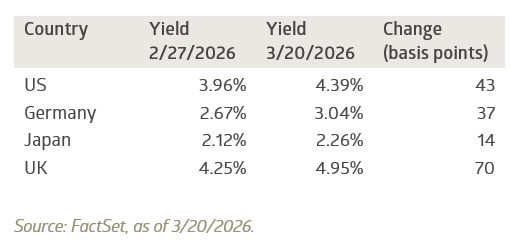

Higher energy prices raise the risk of persistent inflation. That, in turn, is pushing yields higher. Yields have moved higher across major economies as markets reprice a combination of higher inflation, elevated growth risk, and sustained fiscal deficits. As of last week, the U.S. 10-year reached 4.39%, with similar moves across Germany, Japan, and the UK.

Global 10-year yields have moved higher

Short-term yields tell the same story. Just one month ago, futures markets implied a 92% probability of at least one Fed cut, with 2–3 cuts as the most likely outcome. Today, that has shifted materially. Markets now imply a 70.9% probability of zero cuts, with roughly equal odds of either one cut or one hike.

At the start of the year, the expectation was for steady easing. That path now looks less certain. Sticky inflation, geopolitical risk, and the potential pass-through from higher energy prices are all pushing in the same direction.

The outlook has become less linear

The year began with a clear expectation of easing monetary policy. That view has been challenged.

Tighter policy and higher anticipated borrowing costs are starting to show up across equity valuations, bond markets, and investor sentiment. At the same time, uncertainty around inflation and geopolitics is narrowing the range of likely outcomes.

Instead of a clean easing cycle, markets are now adjusting to a more conditional path forward. Policy decisions and external shocks are playing a larger role than many expected at the start of the year.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Rising energy prices test the consumer and the Fed

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy prices test the consumer and the Fed

Dave Harrison Smith, CFA

Chief Investment Officer

March 16, 2026

Energy prices rise, consumer holds for now

The conflict in the Middle East continues, with no clear path to de-escalation. Oil has moved higher, with WTI crude closing Friday near $100 per barrel. U.S. gas prices have also risen sharply, with the national average reaching $3.80 per gallon, up from below $3.00 pre-conflict (source: gasbuddy.com).

Markets, for now, appear to be pricing in a relatively contained and short-lived disruption. Even in best-case scenarios, damage to Gulf infrastructure will likely take months to repair and return to full capacity. As a result, many analysts expect oil prices to remain elevated for much of 2026. Sustained higher energy prices feed into inflation and add pressure on consumers through rising fuel costs.

Encouragingly, the consumer entered March in solid shape. High-frequency spending data from Bank of America showed strong trends in February, and commentary from Visa and Mastercard was broadly constructive at recent investor conferences. Even discount retailer Dollar General reported strong earnings, noting that spending remains “pretty resilient from a consumer perspective.”

Historically, energy shocks act as a tax on consumers. The longer prices remain elevated, the greater the risk of demand shifting away from discretionary categories. The key question is durability.

Sticky inflation complicates the Fed’s path

The Federal Reserve faces a challenging backdrop. Energy prices have surged and will likely pressure inflation in the coming months. While the Fed has historically looked through supply-driven inflation and focused on underlying demand, inflation remains sticky and above target even before the recent escalation.

The February CPI release was mixed. Inflation has moderated but remains above the Fed’s 2% target, with core CPI rising at a 2.5% annualized pace. The read-through to the Fed’s preferred inflation gauge, PCE, may point to somewhat higher inflation given its different basket of goods. Importantly, this data does not yet reflect the recent increase in energy prices.

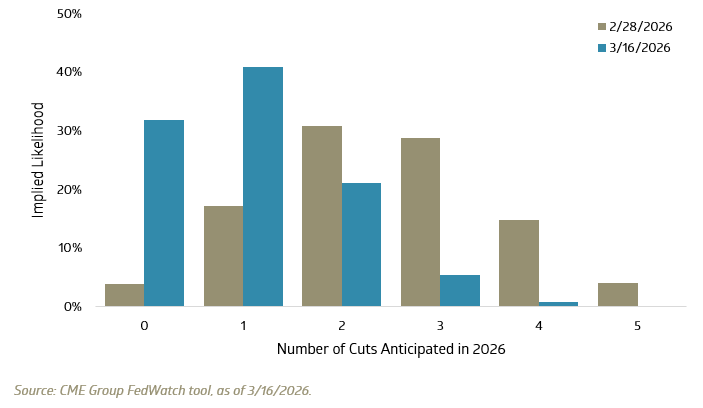

Inflation remains persistent, and markets have adjusted accordingly. Futures markets now price in between zero and one rate cut for the remainder of 2026.

Number of rate cuts expected in 2026, as implied by market futures

Market leadership shifts following the start of the conflict

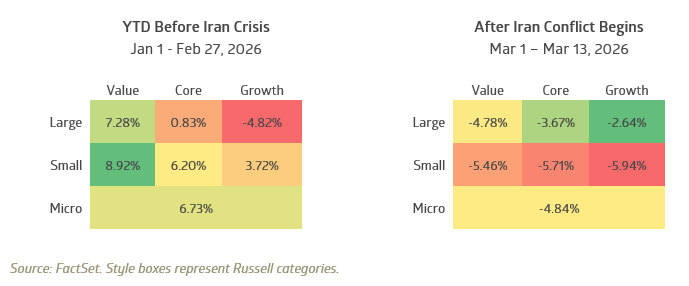

Market leadership has shifted alongside changing rate expectations and rising economic uncertainty. For the first two months of the quarter, small-cap and value stocks outperformed, with small-cap value rising nearly 9% through the end of February. Large growth, dominant in recent years, lagged, with the Russell 1000 Growth Index down 4.8%.

Style returns, before and after the start of the Iran conflict

As the conflict escalated, that leadership dynamic began to reverse. Large-cap growth stocks, while still negative, have held up relatively better. Small-cap stocks have lagged across growth, core, and value styles, reflecting greater sensitivity to economic growth and financial conditions.

The earlier strength in small-cap and value reflected a broadening of participation across U.S. equities. Markets are now re-pricing both economic growth and interest rate expectations in real time.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Oil Surges and Markets Reprice

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The Gulf erupts, oil surges, and markets reprice

Dave Harrison Smith, CFA

Chief Investment Officer

March 9, 2026

The Strait of Hormuz closes and oil surges 60%

The situation in the Middle East has devolved into a fierce and sprawling military conflict. Iran’s response to continued Israel/U.S. strikes has entangled a dozen other countries, with tens of thousands killed or injured, civilian infrastructure shuttered, and energy production and transportation facilities abruptly offline.

Over the past week, the conflict has broadened well beyond initial expectations. This is not a repeat of the targeted strike on Iran’s nuclear facilities in 2025. Iran’s response has drawn in a wide swath of major energy-producing countries. Critically, the Strait of Hormuz—through which roughly 20%/30% of global oil/natural gas supply flows—has effectively closed to shipping traffic. Production shutdowns across Kuwait and other countries reflect not just fear of direct strikes, but a breakdown in transportation and available storage capacity. Systemic complexity is amplifying the energy disruption in ways not fully anticipated.

The impact on oil prices has been dramatic and swift. West Texas crude has spiked from $66.96/barrel at the end of February to above $110 as of this writing. At an increase of over 60%, this places it among the largest six-day moves in three decades and second only, in dollar terms, to the immediate aftermath of the COVID shutdown in 2020. Average U.S. gasoline prices have risen more than $0.50 per gallon in a single week, with further increases likely. Jet fuel has surged as well, foreshadowing higher travel costs heading into summer. Businesses and consumers are reeling.

U.S. equities hold; international markets and bonds sell off

Beyond commodity prices, the financial market reaction has been significant. U.S. equities have been relatively resilient, reflecting the United States’ position as a major energy producer since the shale boom, with the S&P 500 Index down 2.0% and the Russell 2000 Index down 4.0% on the week. International markets have fared worse: the EAFE Index fell 6.7%, and Emerging Markets declined 6.9%, reflecting both the global growth risk from spiraling energy costs and the impact of a strengthening U.S. dollar, which has functioned as a safe-haven currency.

Government bonds have also broadly sold off, failing to provide refuge. Yields on the U.S. 10-Year Treasury increased to 4.15% last week, up from 3.96% at the end of February, while the 2-Year rose from 3.39% to 3.57%. These moves reflect elevated inflation fears and a reduced likelihood of Federal Reserve rate cuts. The market is now pricing in a single cut in 2026, down from the two to three cuts anticipated just last week.

Energy price shocks create a complex dynamic. Headline inflation rises directly; so too does core inflation, as fuel and electricity costs are absorbed into the production costs of goods and services broadly. At the same time, sustained energy price increases tend to compress consumer spending, particularly among lower-income households, where food and fuel represent a disproportionate share of the budget. Our research suggests this segment of the economy is already under meaningful financial stress, and the current shock will deepen that pressure.

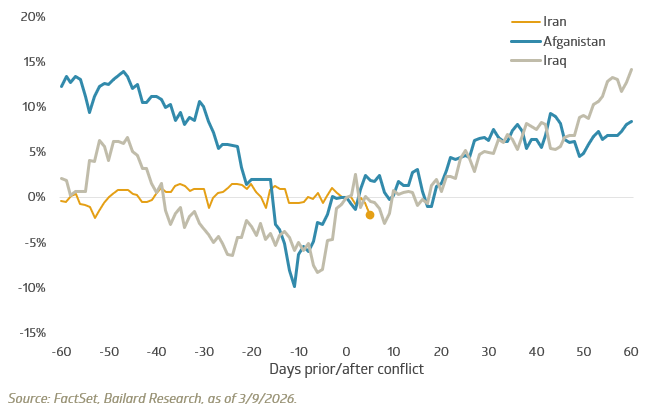

What history says about markets after geopolitical shocks

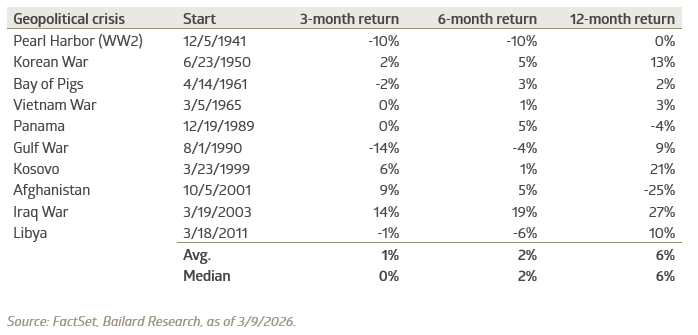

The news flow remains difficult, and volatility is elevated. A key question worth considering: how much risk is already priced into current market levels? The history of geopolitical events offers useful and heartening context. Past events have often followed a similar pattern: an initial repricing as uncertainty spikes, followed by stabilization and recovery as the situation becomes more legible to markets. The S&P 500 has frequently produced positive returns over the three-, six-, and twelve-month periods following major geopolitical crises, illustrating how quickly these shocks can be absorbed into market expectations.

Market returns following major geopolitical crises

Looking at recent Middle East conflicts specifically, the S&P 500 posted positive average returns over each of these time horizons, rising 11.5%, 12%, and 1% over 1-, 3-, and 12-month periods, respectively. The sample size is limited, and each conflict’s surrounding economic and geopolitical environment is different. This history is best understood as descriptive context, not a forward-looking projection.

S&P 500 Index price return around onset of select conflicts

We remain focused on where risk is concentrated and where dislocations may be surfacing opportunity. Our emphasis on quality across strategies is designed to provide relative resilience in periods like this. We continue to evaluate exposure in areas most sensitive to sustained energy cost increases—across regions, sectors, and individual companies—while remaining alert to the pricing anomalies that fear and volatility tend to create.

In our experience, periods of acute uncertainty often obscure the eventual recovery. When markets begin to anticipate stabilization, recoveries can unfold quickly and well in advance of any formal resolution. In periods of elevated uncertainty, patience and discipline remain among the most durable investment advantages.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Escalation Abroad & Stress in Credit

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Escalation Abroad and Emerging Stress in Credit

Dave Harrison Smith, CFA

Chief Investment Officer

March 2, 2026

The Middle East explodes into war

Over the weekend, the region collapsed into a situation investors had feared. The U.S. and Israel conducted a barrage of strikes against Iran, while Iran retaliated against not only Israel but also against Qatar, the UAE, Saudi Arabia, Kuwait, Bahrain, and even a U.K. base in Cyprus. In short order, the region descended into a multi-front conflict with potential global consequences.

I won’t repeat the military or humanitarian details; those are readily available elsewhere. Instead, I’ll focus on what it may mean from a financial perspective.

Oil and energy prices will be the primary conduit through which we see economic and market impact. Iran produces roughly 3 million barrels of oil per day, about 3% of global production. The country also sits on the critical Strait of Hormuz, the chokepoint waterway through which an estimated 15% to 20% of global oil supply flows by tanker. Traffic through the Strait has already slowed to a trickle as shipping companies and insurers evaluate risks. While some disruption could be mitigated in the short term via pipelines and alternative ports, they simply cannot fully replace Hormuz volume. A lengthy shutdown would have significant repercussions for global energy prices.

Thus far, the initial market reaction looks textbook, if subdued. Traditional safe havens including gold, the U.S. dollar, and the Japanese yen are higher, while risk assets such equities are modestly lower. Defense and energy stocks are surging. Oil has traded in the mid-$70s to low-$80s per barrel range, up roughly 5% to 13% from recent levels. Airline stocks are notable underperformers, as a wide corridor of Middle Eastern airspace has been shuttered and one of the world’s busiest airports, Dubai International, was hit by a missile strike. Investors may wonder why the market reaction has not been more severe. That may reflect some prior anticipation of a conflict, as seen in the recent decline in safe haven 10-year U.S. Treasury yields from 4.26% at the start of February to 3.96% last week.

This is clearly a major geopolitical event. The human cost will be enormous, and the path of nations will be determined. Economically, the trajectory for risk assets will depend on both the duration and severity of global disruption. Elevated energy prices feed into inflation in the near-term and higher gas prices crimp consumer spending, particularly among lower-income households where financial stress is already visible. A swift resolution could lead to a return to normalcy. This morning, though, an off-ramp seems unlikely.

Block, formerly Square, announced it will slash workforce by nearly 50%, citing AI productivity gains

This adds fuel to an already contentious debate on the impact of AI on the job market. Block CEO Jack Dorsey was direct: “A significantly smaller team using the tools we’re building can do more and do it better…I don’t think we’re early to this realization. I think most companies are late. Within the next year, I believe the majority of the companies will reach the same conclusion and make similar structural changes.”

There are important caveats. Block expanded aggressively after the pandemic, growing from roughly 2,000 employees to 10,000. While many peers course corrected and reduced payroll in 2023/2024, Block has maintained its elevated employee count. The company has also been criticized by Wall Street for under-earning relative to peers, with adjusted operating margins in the low 20% range against a peer group running 35% to 40% or more.

So, we question: is this actually AI-driven workforce replacement or a company-specific rationalization dressed up with an AI narrative?

The true answer is likely nuanced. One fact worth mentioning: software job postings on Indeed are actually up 11% year over year. The picture is clearly more complicated than at first blush but the implications to our world are significant.

Private credit back in the news… another cockroach in the system

We have previously written about recent implosions in the private credit space, including First Brands and Tricolor. Those collapses caused significant write-downs at several large investment firms and regional banks. At the time, JP Morgan CEO Jamie Dimon commented that there were likely more ‘cockroaches’ in the system.

Last week, the industry found another one. U.K.-based mortgage provider MFS abruptly collapsed amid fraud allegations that the lender had ‘double pledged’ collateral. Investors in MFS include Elliot Management, with a roughly $200 million investment, as well as Barclays, Jefferies, and Apollo Global.

This impact may extend beyond the headline. Over the last five years, investor capital has flooded private credit chasing high yields and strong returns. Our concern is that investment firms loosened underwriting criteria in a rush to deploy capital. Combined with growing pressure in private equity, where many portfolios have considerable exposure to AI-disrupted software firms, there is potential for significant write-downs. Insurance companies and pension funds have deep exposure to both private equity and private credit.

Black swan, systematic events rarely announce themselves politely. This is an area we are monitoring closely.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Country Indices Flash Report – February 2026

Japanese Prime Minister Takaichi convincingly won a snap general election. Her party’s two-thirds lower-house majority—the first post-war instance achieved without a coalition partner—gives her broad latitude to shape policy.