Rising energy prices test the consumer and the Fed - Morning Macro with Dave

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy prices test the consumer and the Fed

Dave Harrison Smith, CFA

Chief Investment Officer

March 16, 2026

Energy prices rise, consumer holds for now

The conflict in the Middle East continues, with no clear path to de-escalation. Oil has moved higher, with WTI crude closing Friday near $100 per barrel. U.S. gas prices have also risen sharply, with the national average reaching $3.80 per gallon, up from below $3.00 pre-conflict (source: gasbuddy.com).

Markets, for now, appear to be pricing in a relatively contained and short-lived disruption. Even in best-case scenarios, damage to Gulf infrastructure will likely take months to repair and return to full capacity. As a result, many analysts expect oil prices to remain elevated for much of 2026. Sustained higher energy prices feed into inflation and add pressure on consumers through rising fuel costs.

Encouragingly, the consumer entered March in solid shape. High-frequency spending data from Bank of America showed strong trends in February, and commentary from Visa and Mastercard was broadly constructive at recent investor conferences. Even discount retailer Dollar General reported strong earnings, noting that spending remains “pretty resilient from a consumer perspective.”

Historically, energy shocks act as a tax on consumers. The longer prices remain elevated, the greater the risk of demand shifting away from discretionary categories. The key question is durability.

Sticky inflation complicates the Fed’s path

The Federal Reserve faces a challenging backdrop. Energy prices have surged and will likely pressure inflation in the coming months. While the Fed has historically looked through supply-driven inflation and focused on underlying demand, inflation remains sticky and above target even before the recent escalation.

The February CPI release was mixed. Inflation has moderated but remains above the Fed’s 2% target, with core CPI rising at a 2.5% annualized pace. The read-through to the Fed’s preferred inflation gauge, PCE, may point to somewhat higher inflation given its different basket of goods. Importantly, this data does not yet reflect the recent increase in energy prices.

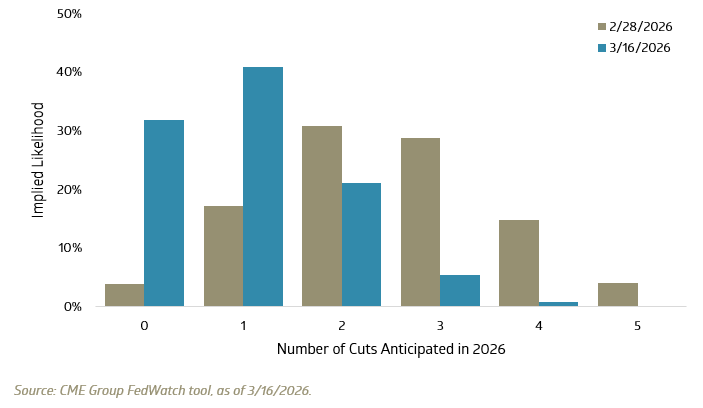

Inflation remains persistent, and markets have adjusted accordingly. Futures markets now price in between zero and one rate cut for the remainder of 2026.

Number of rate cuts expected in 2026, as implied by market futures

Market leadership shifts following the start of the conflict

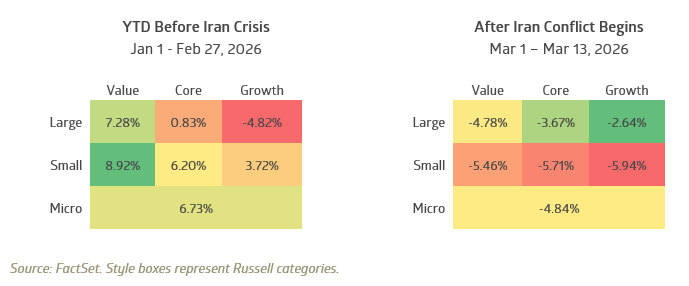

Market leadership has shifted alongside changing rate expectations and rising economic uncertainty. For the first two months of the quarter, small-cap and value stocks outperformed, with small-cap value rising nearly 9% through the end of February. Large growth, dominant in recent years, lagged, with the Russell 1000 Growth Index down 4.8%.

Style returns, before and after the start of the Iran conflict

As the conflict escalated, that leadership dynamic began to reverse. Large-cap growth stocks, while still negative, have held up relatively better. Small-cap stocks have lagged across growth, core, and value styles, reflecting greater sensitivity to economic growth and financial conditions.

The earlier strength in small-cap and value reflected a broadening of participation across U.S. equities. Markets are now re-pricing both economic growth and interest rate expectations in real time.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Oil Surges and markets reprice - Morning Macro with Dave

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The Gulf erupts, oil surges, and markets reprice

Dave Harrison Smith, CFA

Chief Investment Officer

March 9, 2026

The Strait of Hormuz closes and oil surges 60%

The situation in the Middle East has devolved into a fierce and sprawling military conflict. Iran’s response to continued Israel/U.S. strikes has entangled a dozen other countries, with tens of thousands killed or injured, civilian infrastructure shuttered, and energy production and transportation facilities abruptly offline.

Over the past week, the conflict has broadened well beyond initial expectations. This is not a repeat of the targeted strike on Iran’s nuclear facilities in 2025. Iran’s response has drawn in a wide swath of major energy-producing countries. Critically, the Strait of Hormuz—through which roughly 20%/30% of global oil/natural gas supply flows—has effectively closed to shipping traffic. Production shutdowns across Kuwait and other countries reflect not just fear of direct strikes, but a breakdown in transportation and available storage capacity. Systemic complexity is amplifying the energy disruption in ways not fully anticipated.

The impact on oil prices has been dramatic and swift. West Texas crude has spiked from $66.96/barrel at the end of February to above $110 as of this writing. At an increase of over 60%, this places it among the largest six-day moves in three decades and second only, in dollar terms, to the immediate aftermath of the COVID shutdown in 2020. Average U.S. gasoline prices have risen more than $0.50 per gallon in a single week, with further increases likely. Jet fuel has surged as well, foreshadowing higher travel costs heading into summer. Businesses and consumers are reeling.

U.S. equities hold; international markets and bonds sell off

Beyond commodity prices, the financial market reaction has been significant. U.S. equities have been relatively resilient, reflecting the United States’ position as a major energy producer since the shale boom, with the S&P 500 Index down 2.0% and the Russell 2000 Index down 4.0% on the week. International markets have fared worse: the EAFE Index fell 6.7%, and Emerging Markets declined 6.9%, reflecting both the global growth risk from spiraling energy costs and the impact of a strengthening U.S. dollar, which has functioned as a safe-haven currency.

Government bonds have also broadly sold off, failing to provide refuge. Yields on the U.S. 10-Year Treasury increased to 4.15% last week, up from 3.96% at the end of February, while the 2-Year rose from 3.39% to 3.57%. These moves reflect elevated inflation fears and a reduced likelihood of Federal Reserve rate cuts. The market is now pricing in a single cut in 2026, down from the two to three cuts anticipated just last week.

Energy price shocks create a complex dynamic. Headline inflation rises directly; so too does core inflation, as fuel and electricity costs are absorbed into the production costs of goods and services broadly. At the same time, sustained energy price increases tend to compress consumer spending, particularly among lower-income households, where food and fuel represent a disproportionate share of the budget. Our research suggests this segment of the economy is already under meaningful financial stress, and the current shock will deepen that pressure.

What history says about markets after geopolitical shocks

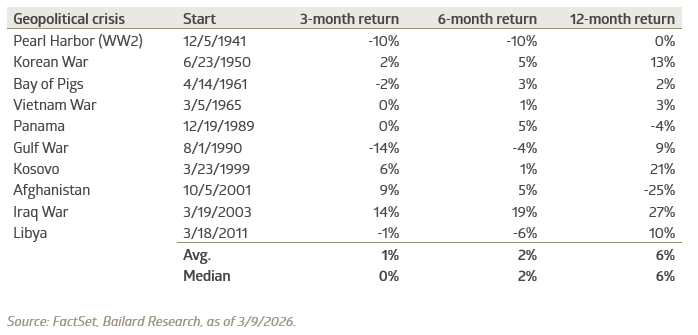

The news flow remains difficult, and volatility is elevated. A key question worth considering: how much risk is already priced into current market levels? The history of geopolitical events offers useful and heartening context. Past events have often followed a similar pattern: an initial repricing as uncertainty spikes, followed by stabilization and recovery as the situation becomes more legible to markets. The S&P 500 has frequently produced positive returns over the three-, six-, and twelve-month periods following major geopolitical crises, illustrating how quickly these shocks can be absorbed into market expectations.

Market returns following major geopolitical crises

Looking at recent Middle East conflicts specifically, the S&P 500 posted positive average returns over each of these time horizons, rising 11.5%, 12%, and 1% over 1-, 3-, and 12-month periods, respectively. The sample size is limited, and each conflict’s surrounding economic and geopolitical environment is different. This history is best understood as descriptive context, not a forward-looking projection.

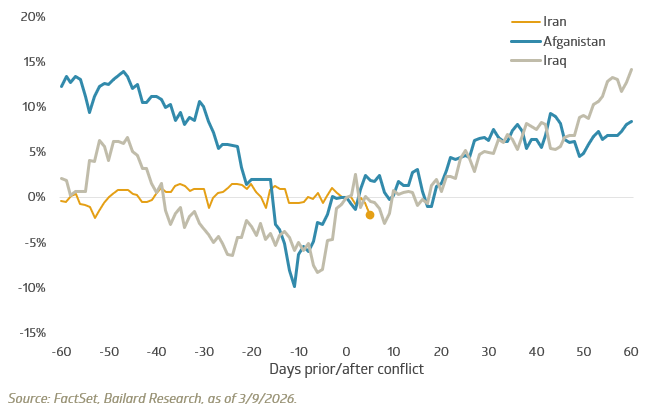

S&P 500 Index price return around onset of select conflicts

We remain focused on where risk is concentrated and where dislocations may be surfacing opportunity. Our emphasis on quality across strategies is designed to provide relative resilience in periods like this. We continue to evaluate exposure in areas most sensitive to sustained energy cost increases—across regions, sectors, and individual companies—while remaining alert to the pricing anomalies that fear and volatility tend to create.

In our experience, periods of acute uncertainty often obscure the eventual recovery. When markets begin to anticipate stabilization, recoveries can unfold quickly and well in advance of any formal resolution. In periods of elevated uncertainty, patience and discipline remain among the most durable investment advantages.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Country Indices Flash Report – February 2026

Japanese Prime Minister Takaichi convincingly won a snap general election. Her party’s two-thirds lower-house majority—the first post-war instance achieved without a coalition partner—gives her broad latitude to shape policy.

Sonya Mughal Named Women in Wealth Advocate of the Year at 2026 Private Asset Management Awards

About Sonya Mughal

Sonya became Chief Executive Officer of Bailard in April 2021, after nearly three decades at the firm. She is the first woman and first person of color to lead the company. Her leadership is marked by consistency and fairness, along with a clear expectation that decisions be both thoughtful and well reasoned.

"Wealth management is stronger when more women are part of it. As advisors, as leaders, and frankly, as clients,” said Mughal. “I am deeply honored, but this truly belongs to the Bailard team. Nearly half of our senior leaders are women, and that is no accident. It is what happens when people are genuinely committed to doing what is right."

Women in Leadership at Bailard

As of December 31, 2025, 48% of Bailard's VPs and above are women. That figure speaks to steady hiring, promotion, and retention decisions over time.

One of the firm’s more tangible practices is pay transparency. Managers understand that compensation decisions must be clear and defensible. That discipline encourages open conversation and reduces ambiguity around advancement, an area where finance has not always been consistent.

For clients, that consistency supports stable teams and clear processes. For employees, it creates a more transparent path for growth.

“The conversations I have with clients are different here,” said Lena McQuillen, CFP®, Vice President and Director of Financial Planning at Bailard. “There is a level of trust that comes from working with a firm that genuinely walks the talk, and you really do get to make a difference in people’s lives.”

About the Private Asset Management Awards

The Private Asset Management Awards recognize firms and individuals across the private wealth management space. The 2026 awards ceremony brought together senior decision-makers from family offices, multi-family offices, private banks, and wealth management firms across the United States. Winners are selected by an independent panel of industry professionals.

In addition to Mughal’s individual recognition this year, Bailard’s Chief Investment Officer Dave Harrison Smith, CFA, was shortlisted for Manager or Investment Research Professional of the Year. The firm was also shortlisted in prior years for Best Philanthropic Initiative and Women in Wealth Advocate of the Year - Company.

About Bailard, Inc.

Bailard is an independent firm that has served individuals, families, and institutions since 1969 with comprehensive wealth management and disciplined asset management solutions. Our work is rooted in clear values, long-term thinking, and a steady commitment to putting clients first. Across the firm, we provide financial and wealth planning, portfolio management, and asset management strategies spanning domestic and international equities, fixed income, sustainable and responsible investing, private real estate, and customized mandates. The firm manages more than $7.7 billion in assets as of December 31, 2025.

Bailard is a Certified B Corporation™ and signatory to the UN Principles for Responsible Investing. We are built on accountability, compassion, and a long-term commitment to doing what’s right for our clients. Learn more at bailard.com, and explore career opportunities at bailard.com/careers.

# # #

Leadership statistics as of 12/31/2025. Bailard does not endorse or control, either expressly or implicitly, the content posted by any third party and disclaims all comments made or information provided by non-Bailard employees. These recognitions do not evaluate the quality of services provided to clients and are not indicative of Bailard’s future performance. There was no cost to enter. The Private Asset Management Awards 2026 judging process is designed to be rigorous and thorough to ensure all entries receive full consideration and that excellence in each of the categories is truly rewarded. A mix of leading wealth managers, advisors/consultants, service providers, and other industry experts make up the judging panel. Presented by With Intelligence, part of S&P Global, winners were announced in February 2026. Additional information is available here: https://awards.withintelligence.com/privateassetmanagementaward/en/page/2026-winners.

Reuters: "US software stocks slammed on mounting fears over AI disruption, lose $1 trillion in week"

Dave Harrison Smith, CFA, as source in a recent article published by Reuters.

Morningstar: "What to Know About the Software Stock Selloff"

Dave Harrison Smith, CFA, as source in a recent article published by Morningstar.

Country Indices Flash Report – January 2026

U.S. asset leadership continued to slide from its early-2025 peak. Gold briefly hit record highs above $5,400/oz as the Fed held rates steady, foreign currencies rallied, and more than 80% of country equity indexes outperformed the U.S. in January. [Read more…]

CNBC: "Tech IPO hype gets drowned out on Wall Street by prospect of $1 trillion in debt sales"

Dave Harrison Smith, CFA, as source in a recent article published by CNBC.