Country Indices Flash Report – March 2022

In one month Russia went from the largest equity market in Eastern Europe to being excluded from all the standard indexes. Warmongering despotism will do that regardless of your resource wealth. For context, in 2006, Russia was a larger component of global indices than China.

Closing Brief - Bailard’s View on the Economy: We Didn’t Start the Fire

Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) shares his perspective on the changing economic landscape both at home and abroad.

March 31, 2022

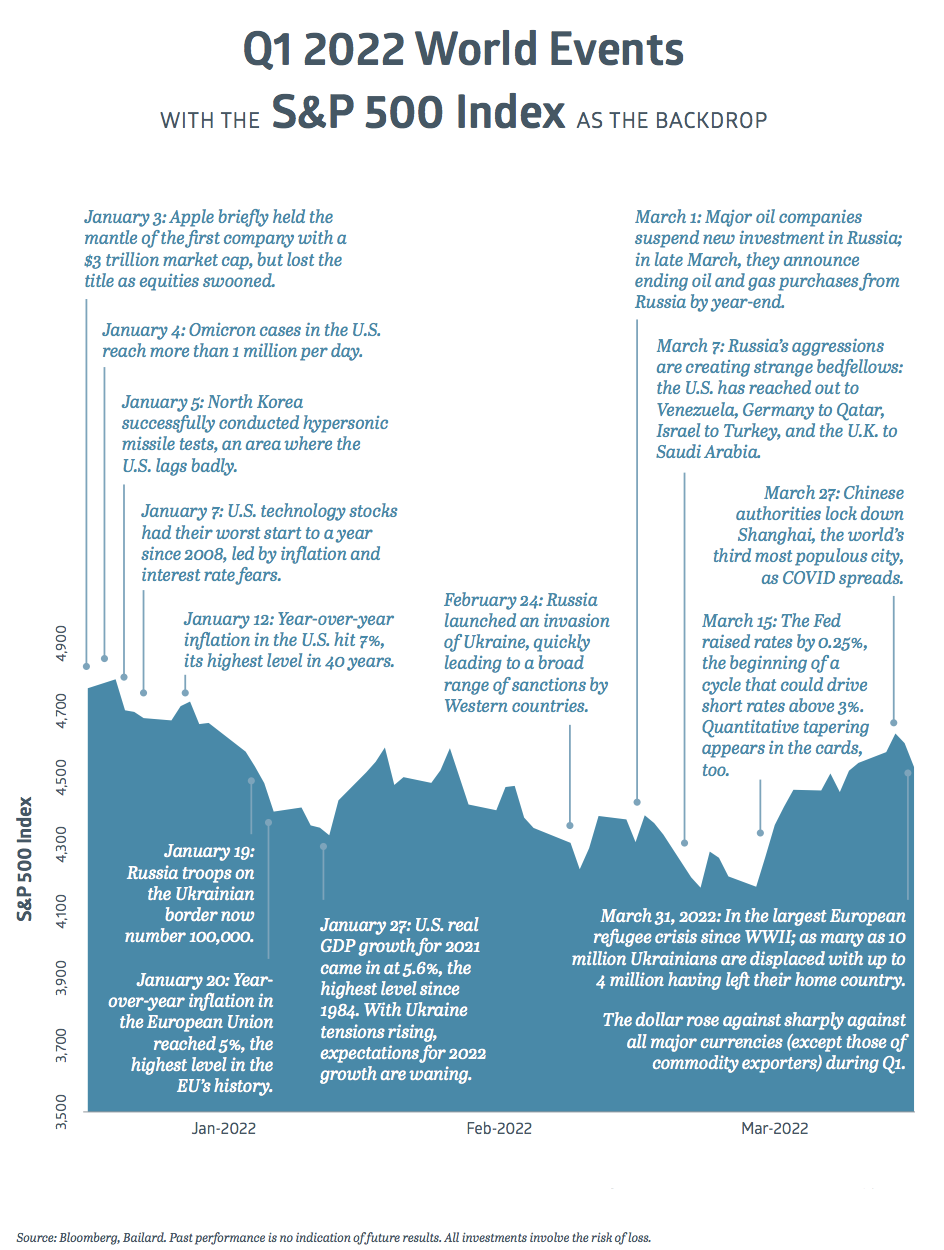

Billy Joel’s Grammy-nominated hit “We Didn’t Start the Fire” was released in September 1989, months after the Soviet Union ended a nearly decade-long occupation of Afghanistan and amidst the steady crumbling of the once formidable USSR empire. At a staccato pace, the song journeys through a historical period that happened to roughly cover the Cold War era, a little over four decades of tumult and strife interwoven with great strides for humanity. Over 30 years later, watching Russian tanks roll into Ukraine—a former Soviet republic—one could imagine the song’s timeline stretching forward to encompass a new set of globally momentous events. The fire is clearly still burning, as another Cold War (or worse) seemingly gets underway.

Geopolitical risk is nothing new to the markets, but to see a brutal, unsparing ground war unfold in the digital era is nonetheless highly disconcerting and a shock to the interconnected global economy. It has the potential for long-lasting ramifications: generational-type economic setbacks for Russia and perhaps even enabler countries. Larry Fink, BlackRock’s long-tenured CEO, put it simply in his 2022 letter to shareholders: “…the Russian invasion of Ukraine has put an end to the globalization we have experienced over the last three decades.”1 Whether permanent shifts occur in cross-border economic activity remains to be seen. In the short-term, companies and nations are scrambling to distance themselves from Russia. Importantly, the European Union pledged to cut natural gas imports from Russia by two-thirds over the course of 2022, and phase out entirely by 2027.2

We have been through a lot over the past 24 months, yet largely we’ve been here before in some form, whether it’s Russia invading or Afghanistan changing hands or even the flu pandemic a century ago. Today’s particular mixture of unstable elements may be new, but Billy Joel’s lyrics are in a sense timeless, a reminder that progress is at best a rocky road. The financial markets seemed to recognize this in the first quarter, reacting more negatively to news of higher inflation and interest rates than bombs and bloodshed. In fact, the major U.S. equity indices traded higher from the point Russia invaded on February 24 until the quarter ended. The S&P 500 Index gained 5.6% price-only in that timeframe, trimming its Q1 loss after a tech-driven selloff to begin 2022, and adding a data point in favor of the old “buy on the cannon” adage.

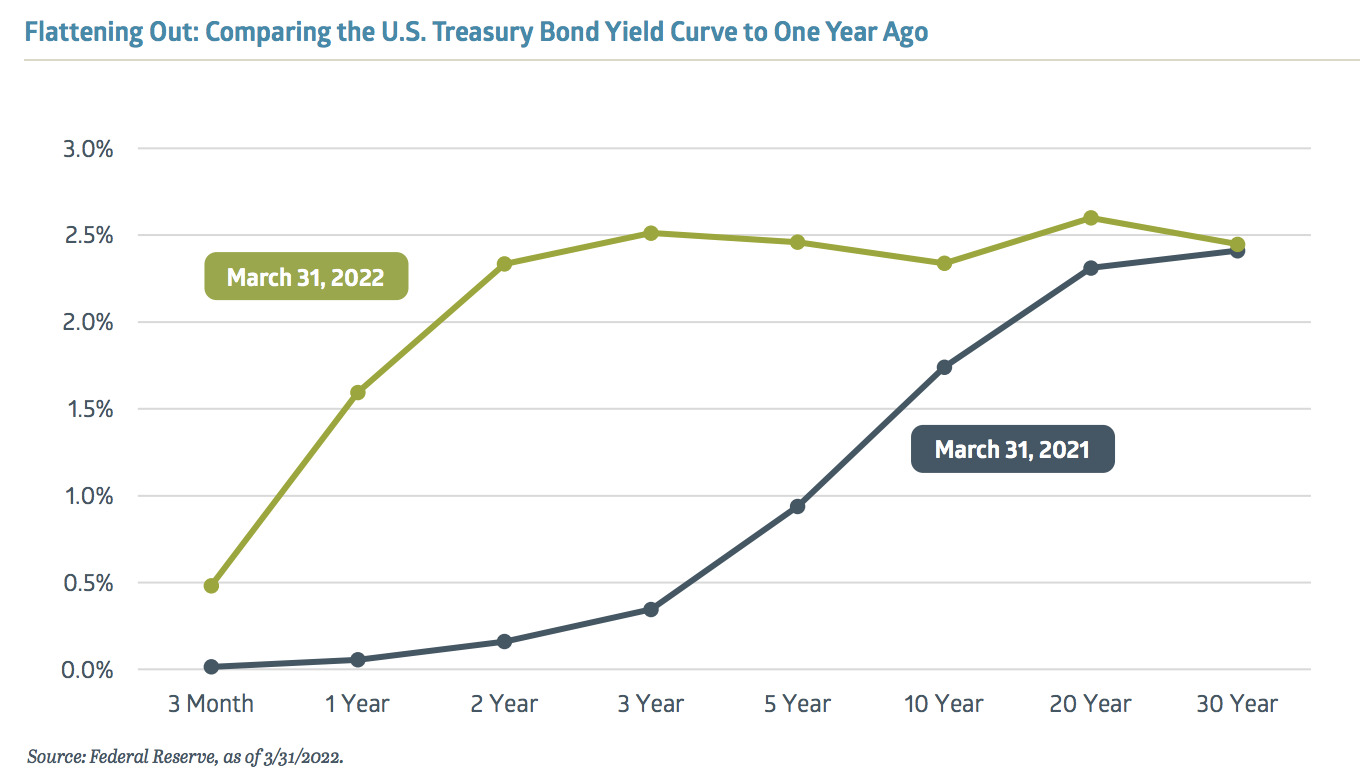

Markets are sending largely cautionary signals as geopolitical turmoil swirls and investors attempt to divine the future for inflation and interest rates. The U.S. Treasury yield curve – which is more of a straight line at present from two years out – had just 0.11% separating the 30-year and 2-year notes when Q1 finished. Some parts of the curve have inverted recently, meaning the yield offered for the shorter maturity (2-year, e.g.) was higher than the longer maturity (10-year, e.g.). Historically, an inverted yield curve is a recession warning sign, albeit an imperfect one. Investors who fled to the relative safety of bonds suffered historically poor returns in the first quarter as rates moved higher: the Bloomberg U.S. Aggregate Bond Index declined 5.9%, its largest quarterly loss since 1980.3

Equity investors were more ambivalent, but ultimately all the major equity indices declined, with international markets faring modestly worse than domestic ones. Value easily outperformed Growth, a continuation of a trend we saw in 2021 within the U.S. mid-cap and small-cap categories, but a reversal for large-cap. Only two S&P 500 sectors rose in the first quarter: Energy and Utilities. West Texas Intermediate (WTI) crude oil jumped 33% to $100 per barrel, taking the Energy sector along for the ride, after reaching a closing high of almost $124 earlier in March. Higher crude oil prices translate into elevated input costs across the economy, a headwind for other sectors. Utilities are typically viewed as steady businesses that hold up relatively well in economic slowdowns. Therefore, it wasn’t particularly encouraging to see either of those sectors atop the Q1 leaderboard. In addition, the S&P 500 Banks industry group sank 8.1% on a price-only basis, a sign that investors may be assigning a higher probability to a more severe economic slowdown. The Conference Board estimates that U.S. Real GDP (Gross Domestic Product) growth will slow to 3.0% in 2022 from 5.7% last year.4

Shrinkflation

The Consumer Price Index (CPI) rose 7.9% in February relative to one year earlier, with Core CPI (ex-food & energy) not far behind at an increase of 6.4%. Inflation hadn’t run this hot since January 1982, and higher gasoline prices accounted for about one-third of February’s increase. Global supply chain struggles persist, complicated further by war in Ukraine. One bit of good news, at least to economists, is that April 2021 marked the last month of less than 5% year-over-year CPI growth readings, setting up for at least tougher comparisons as 2022 unfolds. That will be of little consolation, however, if inflation continues to become entrenched across the economy.

Of chief concern is wage inflation, which grew at 5.6% year-over-year in February, according to the Bureau of Labor Statistics. Fed Chairman Jerome Powell admitted in March that the job market is “tight to an unhealthy level,” with more than 1.7 job openings for every unemployed person. The March 2022 unemployment rate was just 3.6%, nearly identical to the pre-pandemic February 2020 rate of 3.5%. There are encouraging signs regarding labor force participation. The participation rate for the key 25 to 54 years-old demographic continued to edge higher, hitting 82.5 in March, just below the 83.0 level from February 2020. For the 55+ years old cohort, the labor participation rate is likewise heading north, easing some of the “great resignation” worries. If these trends continue, wage inflation should moderate and avoid the dreaded wage-price spiral.

In the meantime, companies continue to find ways to combat rising costs. Last year, Frito-Lay reduced its standard-size Doritos bag by half an ounce, or the equivalent of five chips. The price of the bag remained $4.29, however. The term for this is shrinkflation, referred to as inflation’s “devious cousin” by NPR.5 This practice of package downsizing is common in the food industry, and has been for a long time. Nabisco dropped two ounces from its family size Wheat Thins box, a loss of 28 crackers, and akin to a 14% price increase. Although not a new phenomenon, shrinkflation tends to increase with cost pressures. When online news organization Quartz reached out to Frito-Lay about the scaled-down Doritos bag, a representative said: “Inflation is hitting everyone…we took just a little bit out of the bag so we can give you the same price and you can keep enjoying your chips.”6 That sounds like a win-win proposition, until you get to the bottom of the bag and find yourself five chips short of satisfied.

Finally Fed Up

We have liftoff, at last. In March, the Federal Reserve took its first step toward normalizing monetary policy by increasing the target Fed Funds rate to the 0.25% to 0.50% range. This came two years after the Fed slashed the lower end of the target range to 0% in response to the pandemic onset. Prior to the pandemic, the Fed had cut three times in 2019 despite acknowledging at the time that the “labor market remains strong” and with inflation stable – although arguably too low given the Fed’s 2% inflation objective.7 The bias has clearly been to support economic growth and allow inflation to move higher, the latter of which was formalized in 2020 via the Fed’s new “average inflation targeting” policy.

With inflation now at a 40-year high, naturally there are questions. To be fair to the Fed, they couldn’t anticipate the pandemic and the supply chain issues that have resulted. However, it does seem as though the Fed could have moved off their “zero interest rate policy” (ZIRP) last year, with the economy in recovery mode and vaccine adoption reasonably widespread. Maintaining the Fed Funds rate at zero is really meant for emergency periods, economically speaking, and the Fed has perhaps been too cavalier about using this approach. They now run the risk of policy error with inflation running ahead of their ability to tame it.

The current expectation is that the Fed raises aggressively over the remainder of 2022, at all six remaining meetings, taking the target range up to 2.25% to 2.50%. Will this be enough to cool down inflation? The bond market thinks so: current rates for inflation-linked U.S. Treasuries imply annual inflation of 3.4% over five years compared to 5.6% over the next year.8 Chairman Powell pointed to several “soft landings” of the past, instances where rates were raised without tipping the economy into recession. Raymond James economist Scott Brown noted that tighter monetary policy won’t do much to help the supply chain, but demand should be slowed, and with aggressive Fed action required the economy may slow more than intended.9

A high inflation, slow growth economic environment would likely prove challenging for equity and bond investors alike. Corporate earnings have been resilient thus far, with S&P 500 Index operating earnings projected to climb 8% this year to $225 per share. Based on that estimate, the Index traded at a still lofty 20x forward earnings when Q1 wrapped up. With inflation running hot and interest rates presumably heading higher, we should see U.S. large-cap valuations go lower, leaving it up to corporate profits to maintain pace. Equity valuations in other categories remain more favorable, with the S&P MidCap 400 Index, S&P SmallCap 600 Index, and MSCI EAFE Index all clustered around 14x forward earnings. The MSCI Emerging Markets Index trades at closer to 12x earnings.

Following three straight years of strong returns, equities may need a breather in 2022. The odds of a recession are on the rise yet remain low in the short-term. New fires will break out as the world is turning, testing the altered global economy’s resilience and the tools we have to fight them.

1 “Larry Fink’s 2022 Chairman’s Letter,” www.blackrock.com, 3/24/2022

2 “Will the Ukraine War Spell the End of Globalization?”, www.nytimes.com, 3/30/2022

3 “Bond Market Suffers Worst Quarter in Decades,” www.wsj.com, 3/31/2022

4 “The Conference Board Economic Forecast for the US Economy,”www.conference-board.org, 3/10/2022

5 “Beware of ‘Shrinkflation,’ Inflation’s Devious Cousin,” www.npr.org, 7/6/2021

6 “How companies are hiding inflation without charging you more,” www.qz.com, 3/10/2022 7 “Federal Reserve issues FOMC statement,” www.federalreserve.gov, 10/30/2019

8 Source: Bloomberg, US Breakeven 1 Year and the US Breakeven 5 Year indices, as of 3/31/2022

9 “Weekly Economic Monitor – Soft Landings Are Hard,” www.raymondjames.com, 3/25/2022

Bailard Becomes CDP Investor Signatory

- Strengthens firm’s formal commitment to ESG

- Adds to existing environmental commitments including to Principles for Responsible Investment (PRI) and Climate Action 100+

FOSTER CITY, Calif. – March 15, 2022 – Bailard, Inc., an independent, values-driven wealth and asset management firm in the San Francisco Bay Area, is pleased to announce that it has furthered its commitment to mitigating climate change risk in its portfolio and driving corporate climate disclosure by becoming an investor signatory to CDP (formerly known as the Carbon Disclosure Project), the non-profit that runs the global environmental disclosure system.

As an investor signatory, Bailard joins a group of 680+ financial institutions, with over $130 trillion in assets, requesting disclosures using CDP’s climate change, deforestation, and water security questionnaires, which are fully aligned with the recommendations issued by the Task Force on Climate-related Financial Disclosures (TCFD). Additionally, the membership affords Bailard access to the most up-to-date research from the world’s largest corporate environmental dataset, which it will use to inform its investment process and its corporate engagement activities. Last year, over 3,100 public companies reported environmental data to investors through CDP’s disclosure system.

Bailard is already a signatory to the Principles for Responsible Investment (PRI) and the Climate Action 100+. With this CDP signature, Bailard builds upon its formal commitment to Environmental, Social, and Governance (ESG).

“Companies differ drastically on carbon performance, climate goals, and the disclosure of related information. To reach alignment with the Paris Accords and achieve net-zero, we need climate change-informed investment decision-making, backed by accurate carbon emissions disclosure from all economic players,” said Blaine Townsend, CIMC®, CIMA®, Executive Vice President and Director of Sustainable, Responsible and Impact Investing at Bailard.

Townsend continued, “CDP is driving transparency, accountability, and action through the carbon data it gathers from thousands of companies, cities, states, and regions around the world. Bailard is committed to being a climate leader through our investment approach, our corporate engagement, and our client engagement in support of carbon disclosure and climate action.”

“Our signature to the CDP reflects our dedication to ensuring we are functioning as a good actor in our industry,” said Sonya Mughal, CFA, CEO of Bailard. “We are a company committed to our values—on behalf of the individuals, families, and institutions we serve, as well as with respect to our own corporate engagement.”

About Bailard, Inc.

Founded in 1969, Bailard is an independent asset and wealth management firm serving individuals, families, and institutions alike. Bailard has built a long‐term asset management track record across domestic and international equities, fixed income, and private real estate, as well as robust, in‐house ESG expertise. These investment capabilities are combined with financial, tax, and estate planning to provide sophisticated and comprehensive wealth management. Through it all—and in line with its core principles and strong ESG mindset—Bailard works with clients to align their financial goals with their values.

With over $5.5 billion under management, Bailard is a majority employee‐owned and women‐led firm, and a Principles of Responsible Investing (PRI) signatory. A values‐driven firm based in the San Francisco Bay Area, Bailard has its own private charitable foundation and is deeply committed to its core values of accountability, compassion, courage, excellence, fairness, and independence.

All information as of 12/31/2021. Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

About CDP

CDP is a global non-profit that runs the world’s environmental disclosure system for companies, cities, states and regions. Founded in 2000 and working with more than 680 investors with over $130 trillion in assets, CDP pioneered using capital markets and corporate procurement to motivate companies to disclose their environmental impacts, and to reduce greenhouse gas emissions, safeguard water resources and protect forests. Over 14,000 organizations around the world disclosed data through CDP in 2021, including more than 13,000 companies, worth over 64% of global market capitalization, and over 1,100 cities, states and regions. Fully TCFD aligned, CDP holds the largest environmental database in the world, and CDP scores are widely used to drive investment and procurement decisions towards a zero carbon, sustainable and resilient economy. CDP is a founding member of the Science Based Targets initiative, We Mean Business Coalition, The Investor Agenda and the Net Zero Asset Managers initiative. Visit cdp.net or follow us @CDP to find out more.

Chat with the CIO

A Reckoning of Global Priorities: The Changing Calculus of Climate Change and Geopolitics

Bailard’s Director of Sustainable, Responsible and Impact Investing Blaine Townsend, CIMC®, CIMA® chats with Chief Investment Officer, Eric P. Leve, CFA.

March 31, 2022

Eric P. Leve, CFA: Blaine, you and I share a deep passion for understanding how fundamental, long-term issues affect changes in human behavior and investment markets. Sometimes these bigger themes can cause major changes in the short term, and this certainly feels like one of those times. There has been a profound reckoning in the last decade, that the sources of energy that we use to power our world matter. Today, we face a challenge that most of us have tried to ignore: the fine balance between our clean energy aspirations with our economic, technological, and resource endowments amid the geopolitical reality of the dynamics between energy producing and consuming nations.

Blaine Townsend, CIMC®, CIMA: You’re hitting upon an “inconvenient truth.” In an ideal world, investors wouldn’t support an energy company that derives its revenue from nations without democratic institutions. But what does one do when your allies with deep democratic values (Germany would be my prime example here) desperately need those resources not just to “keep the lights on” but, more critically, to keep its people from freezing in winter? The recent actions of Russia in Ukraine will have profound effects on how the world thinks about its energy transition and a heightened appreciation of the need for energy independence.

Transitioning from unsavory suppliers is one step, but doing it quickly probably means a greater use of “dirty” energy sources. That said, in the long run, the conflict is likely to accelerate innovation and adoption of cleaner alternative solutions.

Eric: For Germany to decrease its energy dependence on Russia, it needs to wean itself from the Nord Stream I gas pipeline, which for the past ten years has supplied 30% of the nation’s natural gas. Russia also provides more than 50% of Germany’s coal. What we’re currently hearing is that Germany’s ambitious goal is to end imports of Russian oil and coal this year, and natural gas by 2024. The key here is that nations can’t simply flip a switch and change their energy infrastructure. If their systems are geared toward natural gas usage, it is hard to quickly transition to new sources, so generally this means finding new sources of natural gas. But, some power plants can make the switch of their fuel source from natural gas to coal. Since coal is found in many places, and is easier to transport than natural gas, we will likely see increased use of coal burning to generate needed power in Europe in the short term.

Indeed, the immediate solutions to this puzzle will likely have offsetting effects from an environmental perspective. Governments should, and may, push their populations to decrease energy use in the near term. For those old enough to remember 1973, they’ll recall gasoline rationing and lower speed limits, along with raising thermostats in the summer and lowering them in winter. But so far this hasn’t happened. European leaders have simply reduced government duties on fossil fuels to lessen the pain on consumers. It may be that, in this time of populism in Europe, leaders may not have the gumption to burden their peoples. With many consumers at wits end after two years of pandemic constraints, asking for more sacrifices may be politically toxic.

The more obvious near-term solution is that governments across Western Europe will likely seek oil, gas, and coal supplies from any sources they can. An uncomfortable silver lining is that the world’s biggest energy consumer is currently using a lot less. China was already expecting sharply lower economic growth this year than last, but with the huge spike in COVID across the country and the virtual lockdown of the world’s third most populous city (Shanghai), China’s energy consumption will be much lower than normal.

This leaves more resources for the rest of the world, putting a (small) damper on price increases.

Blaine: It is seminal events in history that propel rapid change. Russia’s hopes of restoring a Greater Russia may lead nations seeking energy security to forge new alliances. Neighbors, allies, and frenemies will quickly react to the heightened risk of an unpredictable and militaristic supplier.

In quick order, Germany has pivoted to a potential new gas deal with the world’s largest exporter of liquefied natural gas, Qatar. For now, this seems like a relatively healthy move away from dependency on a dangerous autocratic government toward a nation looking to build bridges with the west, and one becoming a global, rapidly-modernizing autocracy. A broader, multinational sourcing of fuels will provide Germany, and Europe in general, a more dependable flow of natural gas as they transition to next-generation solutions. Indeed, we may look back upon this era as one that helped created a broader array of multilateral relationships among countries that previously shared few bonds.

Eric: Looking beyond Germany, the needs and resources of the countries of Europe vary dramatically. Nations such as France and Sweden generate much of their domestic energy from nuclear power, more than 40% and 30%, respectively. Sweden generates almost one-half of its electricity from hydroelectric sources and about 17% from wind. Denmark generates 45% of its energy from wind. But 45% of Poland’s energy comes from coal and much of the rest from natural gas, both primarily imported from Russia.

As a transitional solution to even more sustainable solutions, nuclear could play a key role across much of the European continent. But instead of the large-scale plants that take years and decades for approval and construction, a new generation of nuclear plants called small modular reactors (SMRs) can be constructed in as little as 500 days. These plants have much smaller physical footprints and use their nuclear fuel more effectively, leading to much less spent fuel needing to be sequestered. A single one of these SMRs can provide energy for more than 300,000 homes. Still, we are seeing countries such as the United Kingdom push for the newer-generation large scale nuclear plants as a step to wean themselves off imported natural gas.

But Blaine, I’d argue that the more exciting potential outcome of this crisis is the potential for an accelerated path to truly local and sustainable forms of energy generation.

Blaine: And so we get to a critical point. As the “trade cold war” with China over the past few years motivates countries and companies to depend less on foreign suppliers and bring manufacturing closer to home, Russia’s aggressions will likely accelerate the transition to renewable energy sources, many of which can be produced domestically, depending on one’s geography and geology. This will not be easy. It will require multitrillion-dollar global investments. The acceleration of this transition is one reason we continue to be supportive of companies that benefit from this broad infrastructure transition.

And it is this longer-term scenario that is exciting for me. In the same manner that World War II led to the formation of the United Nations and to historic capital spending globally, or how increased globalization and increased trade did the same in the early 2000s, we are on the brink of an historic, secular investment in alternative fuels that now has a critical catalyst. Primary capital expenditures for energy have been falling globally for eight years since the previous oil price spike above $100 per barrel. But now we have dual needs: increasing natural gas and other carbon-based energy infrastructure in the intermediate term, while at the same time developing next-generation energy sources that support longer-term goals of net zero emissions. These efforts can create energy independence for a broader range of countries.

Global expenditures for these two efforts may quickly surpass the previous peak of energy infrastructure spending of about $2 trillion annually in order to supply the world’s still growing energy needs. Goldman Sachs estimates that it will take $56 trillion of investment through 2050 to build a credible, global clean energy infrastructure. It is a tragedy that the invasion of a sovereign nation has been required to jumpstart this, but it isn’t all that dissimilar to the revolution in automobile gas efficiency spurred by the 1973 ArabIsraeli War and OPEC’s oil embargo against the United States. History books 30 years from now may see this as the moment that resource-rich autocratic nations began to lose their stranglehold over the world and the moment that the net-zero movement got teeth.

Eric: Blaine, thanks so much for sharing your insights. As Winston Churchill said, “never let a good crisis go to waste.”