Country Indices Flash Report – January 2025

2024’s political upheavals continued in the new year with Canadian Prime Minister Justin Trudeau’s resignation. His Liberal Party will select a new leader for elections later this year; they significantly trail the Conservatives in polls.

Quarterly International Equity Strategy Q4 2024

Non-U.S. equities faced meaningful headwinds in a quarter of political intrigue among some of the world’s most critical democracies. Many central banks continued to lower short-term interest rates, reducing one strain on borrowers and the economy. At the same time, those same actions put downward pressure on currencies with only the Israeli shekel rising against the greenback in the quarter. Still, lower rates relative to the U.S. may be the driver of value recognition; even with earnings growth that isn’t keeping up with U.S. companies’, foreign stocks appear better than fairly priced.

Quarterly Technology Equity Strategy Q4 2024

The Bailard Technology Strategy posted a 4q24 total return of 3.06% net of fees, trailing both the cap-heavy benchmark index (S&P North American Technology Index) and the competitor-comprised benchmarks. The Morningstar U.S. Open End Technology Category returned 5.94% and the Lipper Science and Technology Fund Index returned 5.86%, while the S&P North American Technology Index generated 5.92% return and the Nasdaq-100 Index returned 4.93%.

Quarterly Small Value Strategy Q4 2024

A surprisingly hawkish tone from the Federal Reserve board in December suggesting that they plan to keep interest rates “higher for longer” drove market participants back into the arms of large cap growth stocks. Fear of a slower economy with persistent inflation and higher interest rates in the short term countered earlier enthusiasm for smaller cap stocks driven by the potential for a lower regulatory burden under the Trump administration starting in 2025.

Planning for Generational Wealth: Maximizing Tax Efficiency

Lena McQuillen, CFP®, Vice President and Director of Financial Planning, outlines the distinctions between Traditional and Roth retirement strategies, when each is most effective, the implications of new laws, and ways to share these insights with your family.

For those who have already built their wealth, the focus shifts to preserving it, optimizing its use in retirement, and empowering future generations to achieve financial success in a tax-efficient manner. Many readers will have already made key decisions about their retirement accounts—such as 401(k)s, 403(b)s, or 457(b)s—during their working years. Now, the opportunity lies in maximizing those decisions to enhance your family’s financial well-being. Just as you’ve built and managed your wealth, you can pass on the knowledge and strategies to help your family achieve similar success. The choice between Traditional and Roth accounts remains pivotal, offering different advantages for optimizing outcomes both now and in the future. Understanding these options can help refine your strategy and empower your heirs, equipping them with the tools to build on your financial legacy.

Understanding the Basics

A Traditional 401(k) allows contributions on a pre-tax basis, reducing taxable income during your working years. Over time, these funds grow tax-deferred, but taxes are owed on withdrawals. Required minimum distributions (RMDs) begin at age 73 (or age 75 if born in 1960 or later), impacting your taxable income in retirement.

Roth 401(k) contributions, made with after-tax dollars, offer a different advantage: earnings grow tax-free, and qualified withdrawals are not taxed if the account has been open for at least five years and withdrawals are made after age 59½. Additionally, Roth accounts bypass RMDs, allowing assets to grow tax-free indefinitely—a benefit particularly valuable for estate planning. For families managing wealth across generations, Roth accounts can provide a powerful vehicle for tax-free growth over your lifetime.

How Much Can You Contribute?

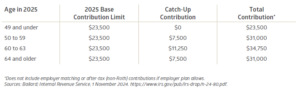

The SECURE 2.0 Act has introduced new opportunities for optimizing retirement accounts. In 2025, enhanced catch-up contributions allow individuals aged 60 through 63 to contribute up to $11,250 beyond the $23,500 base limit. If your children or grandchildren are early in their careers, encouraging them to maximize contributions to their own accounts can set the stage for long-term financial security.

Additionally, employers now have the option to match contributions to Roth accounts, providing additional flexibility for wealth transfer and reinforcing the value of maximizing contributions to these accounts early.

How Much Should You Contribute?

- While contributing the maximum may no longer apply to you personally, consider how these strategies can be leveraged for your family: For Children and Grandchildren: Encourage them to maximize Roth contributions early in their careers, reaping the benefits of tax-free growth over decades. Highlight the importance of contributing enough to qualify for employer matching funds—essentially free money that accelerates their savings—to make the most of their retirement plans. Also encourage them to evaluate their living expenses relative to their salary for a sustainable savings rate that balances immediate needs with long-term goals.

- Managing Your RMDs: Strategically converting portions of Traditional accounts to Roth during years with lower taxable income can reduce the impact of future RMDs. For your heirs, guiding them in understanding how RMDs may affect inherited accounts and encouraging early planning can optimize their tax efficiency, supporting a smoother transfer of wealth.

- Integrating Contributions: Use your resources to gift or match contributions to family members’ retirement accounts, fostering their financial independence. Consider offering a dollar-for-dollar match on your grandchild’s Roth IRA contributions. For instance, if they contribute $3,000 from their summer job earnings, you match it with another $3,000 (up to their total earnings or annual limit, whichever is less). This not only incentivizes their savings habit but also allows them to maximize tax-free growth potential from a young age, leveraging decades of compounding.

These actions not only benefit your family but also extend the tax-efficient strategies that have supported your success. If contributing the maximum feels daunting to your younger loved ones, suggest they start small. Gradually increasing the allocation as income rises or debts are paid off can ease the transition while building wealth consistently.

Factors to Consider: Maximizing Family Wealth

When planning for your family’s financial future, understanding the role of Traditional and Roth accounts is critical. These tools offer unique advantages that can help optimize your wealth strategy and leave a lasting legacy.

Traditional Pre-Tax Accounts

Traditional Pre-Tax Accounts

Traditional 401(k) accounts are effective for managing current cash flow but require thoughtful tax planning to maximize their benefits and minimize liabilities. By reducing adjusted gross income (AGI), they can also provide additional flexibility for managing tax brackets. Converting funds to Roth accounts during low-income years can mitigate RMD impacts and leave more tax-efficient assets to heirs.

Roth Accounts

Roth 401(k)s offer significant flexibility for legacy planning. Contributions grow tax-free, withdrawals are not taxed, and they provide a strategic tool for multi-generational wealth transfer. Encouraging younger family members to prioritize Roth contributions amplifies these benefits.

Splitting Contributions Between Pre-Tax and Roth Accounts

Allocating contributions across pre-tax and Roth accounts provides flexibility to adapt to tax law changes or shifting financial priorities. This approach helps families draw funds in the most tax-efficient manner. Additionally, starting in 2026, catch-up contributions for high earners must be directed to Roth accounts, highlighting the importance of considering both account types in your overall strategy.

An Example of Strategic Allocation in Action

Meet Chloe and Nathan: Recently retired professionals, Chloe and Nathan transitioned from high-earning careers to focusing on wealth preservation and supporting their family’s financial growth. With significant Traditional and Roth retirement accounts, their approach emphasizes tax efficiency and legacy planning.

- Strategic Conversions: During low-tax years, they convert portions of their Traditional 401(k) accounts to Roth accounts. This minimizes future RMDs, maximizes tax-free growth, and provides greater flexibility for drawing retirement income.

- Legacy Planning: Chloe and Nathan prioritize leveraging their Roth accounts to create tax-efficient wealth transfer opportunities. This strategy enables their heirs to benefit from tax-free growth while supporting the family’s long-term financial goals.

- Mentoring the Next Generation: They mentor their adult children on the importance of early saving and tax diversification, particularly through Roth contributions, fostering strong financial habits and long-term independence.

Chloe and Nathan’s thoughtful strategy not only secures their retirement but also sets up their family for financial success, illustrating how retirement planning evolves with life’s stages.

Next Steps

Managing wealth in retirement involves more than sustaining your lifestyle; it’s about building a foundation for future generations to thrive financially. Consider these steps:

- Evaluate Family Tax Strategies: Collaborate with your Investment Counselor to optimize tax efficiency for both current and future generations. For individuals in a higher tax bracket now, contributing to a Traditional 401(k) may make the most sense. Conversely, for those currently in a lower tax bracket, Roth contributions may be more advantageous.

- Foster Financial Education: Use your experience to mentor younger family members on the value of Roth accounts, tax diversification, and long-term planning. Estimate retirement income needs and work with your Investment Counselor to model various scenarios. This includes understanding the impact of diverse income sources such as Social Security and investments.

- Reassess Regularly: Life events, tax law changes, and shifting priorities necessitate periodic adjustments to any strategy. Annual check-ins help keep your plan aligned with financial objectives.

For those no longer contributing to a 401(k), integrating these practices helps you leave a legacy that supports your family’s financial success while minimizing tax burdens.

Conclusion

Choosing between a Traditional pre-tax 401(k) or a Roth 401(k) is not a one-size-fits-all decision; it depends on your unique financial situations, long-term goals, and tax environment. As you transition into retirement, the focus shifts from building wealth to preserving it and empowering your family. Thoughtful planning and informed choices today lay the groundwork for a secure tomorrow. Working closely with a trusted partner helps to ensure that your legacy not only supports your heirs but also instills financial independence and security for generations to come.

Estate Planning Gold: Insights from Warren Buffet's 2024 Letter

Join Director of Estate Strategy, Dave Jones, JD, LLM, CFP®, as he explores Warren Buffett’s timeless insights on estate planning, highlighting actionable principles to guide thoughtful and purposeful generational wealth strategies.

On November 25, 2024, just days before Thanksgiving, Warren Buffett released a letter to shareholders of Berkshire Hathaway Inc.1 Unlike the usual updates on business operations or investments, this letter carried a heartfelt message filled with timeless wisdom on estate planning. Buffett shared reflections on mortality, responsibility, simplicity, and transparency—principles that are as practical as they are profound. For those tasked with managing generational wealth, his insights provide not only lessons but a roadmap for purpose-driven planning. As we begin the new year, let’s examine these lessons and consider how they might inspire our own approach to estate planning.

Acknowledge Mortality

“Father time always wins. But he can be fickle—indeed unfair and even cruel—sometimes ending life at birth or soon thereafter while, at other times, waiting a century or so before paying a visit. To date, I’ve been very lucky, but, before long, he will get around to me.”

In reflecting on the passage of time, Buffett addresses an essential truth: none of us can escape it. Planning for the future is both prudent and necessary. While reflecting on his own life and luck, he emphasizes the importance of taking proactive steps to ensure that his estate planning is handled responsibly. For Buffett, this means facing mortality head-on and making thoughtful decisions about the future.

The new year is an ideal time to consider your own plans. How can you prepare now to give your loved ones clarity and peace of mind when the time comes?

Choose the Right Successor(s)

“[T]omorrow’s decisions are likely to be better made by three live and well-directed brains than by a dead hand. As such, three potential successor trustees have been designated. Each is well known to my children and makes sense to all of us.”

Choosing the right successors is a cornerstone of Buffett’s estate planning philosophy. His selection of capable trustees—respected by both himself and his family—emphasizes the importance of communication, collaboration, and accountability. By involving his children in the process, Buffett fosters alignment and clarity.

For your own estate, think about the individuals who could best carry out your wishes. Are they prepared to handle the responsibilities you’re entrusting to them? Clear communication and thoughtful choices now can make all the difference later.

Give Responsibly

“[Susie] left $10 million to each of our three children, the first large gift we had given to any of them. These bequests reflected our belief that … wealthy parents should leave their children enough so they can do anything but not enough that they can do nothing.”

This sentiment encapsulates Buffett’s philosophy of responsible giving. While financial security is a gift, excess can stifle ambition and purpose. By leaving “enough to do anything but not enough to do nothing,” Buffett fosters independence and encourages his heirs to carve out their own paths in life.

Not every family will relate to or need such a framework, but it’s a principle worth reflecting on. What balance will empower your loved ones without diminishing their drive? This new year, evaluate how your legacy can support growth and self-reliance.

Make It Simple

“I change my will every couple of years – open only in very minor ways – and keep things simple. Over the years, Charlie [Munger] and I saw many families driven apart after the posthumous dictates of the will left beneficiaries confused and sometimes angry.”

Simplicity is a hallmark of Buffett’s estate planning philosophy. Complexity breeds confusion, resentment, and potential conflict among beneficiaries. By keeping his will straightforward and regularly updated, Buffett avoids potential disputes and provides clarity.

As you think about your own plans, ask yourself: Could someone easily understand and implement your wishes? Simplicity may be the key to preserving harmony within your family.

Be Transparent and Flexible

“I have one further suggestion for all parents, whether they are of modest or staggering wealth. When your children are mature, have them read your will before you sign it.

Be sure each child understands both the logic for your decisions and the responsibilities they will encounter upon your death. If any have questions or suggestions, listen carefully and adopt those found sensible. You don’t want your children asking ‘Why?’ in respect to testamentary decisions when you are no longer able to respond.

Over the years, I have had questions or commentary from all three of my children and have open adopted their suggestions. There is nothing wrong with my having to defend my thoughts. My dad did the same with me….”

Transparency is perhaps Buffett’s most transformative principle. By discussing his will openly with his children, he fosters alignment, understanding, and a shared sense of purpose. This collaborative approach strengthens familial bonds and preempts conflicts that could arise later.

While not all family dynamics allow for such openness, it’s worth considering where possible. Honest conversations about your intentions can reduce misunderstandings and increase trust. As we move into a new year, could greater transparency in your plans create more unity and clarity?

Final Thoughts

Warren Buffett’s 2024 letter provides a compelling framework for intentional, values-driven estate planning. By acknowledging mortality, giving responsibly, keeping things simple, and prioritizing transparency, Buffett offers a model for creating a legacy that balances financial security with purpose.

As you reflect on your plans for the year ahead, take inspiration from Buffett’s insights. Estate planning isn’t just about transferring wealth—it’s about fostering unity, empowering future generations, and making meaningful impact. May the new year bring clarity and peace to your planning.

1 Berkshire Hathaway Inc. News Release. 25 November 2024. https://www.berkshirehathaway.com/news/nov2524.pdf

Bailard Clears Redemption Queue and Expands Team for 2025 Growth

Bailard advances its efforts to seize opportunities in the evolving real estate market. With a disciplined investment approach and an expanded team, the Bailard Real Estate Fund is positioned for growth in the year ahead…

Economic Brief: It Don't Mean a Thing, If It Ain't Got That Swing

This quarter, Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) delves into the paradoxes of momentum investing, inflation’s persistent influence, and the resilience of the U.S. economy in an era of shifting market dynamics.

Contrarians are not having a moment. Those resolute and hardy investors who row against the tide of popular opinion—shunning trendy stocks and embracing the unloved—found themselves sinking in 2024. A tidal wave of capital flowed into the fashionable set of equities, largely comprised of companies with a plausible artificial intelligence (AI) story. Winners kept on winning, resulting in a historic rout for momentum investing. In fact, the Standard & Poor’s (S&P) 500 Momentum Index had its best year relative to the overall S&P 500 Index since 1999. It soared 46%, including dividends, outpacing the benchmark S&P 500 by 21 percentage points.

and embracing the unloved—found themselves sinking in 2024. A tidal wave of capital flowed into the fashionable set of equities, largely comprised of companies with a plausible artificial intelligence (AI) story. Winners kept on winning, resulting in a historic rout for momentum investing. In fact, the Standard & Poor’s (S&P) 500 Momentum Index had its best year relative to the overall S&P 500 Index since 1999. It soared 46%, including dividends, outpacing the benchmark S&P 500 by 21 percentage points.

Launched a decade ago—but recalculated back to 1994—the S&P 500 Momentum Index includes the top quintile of the S&P 500 based on trailing 12-month price performance. The Index is rebalanced on a semi-annual basis. As investment concepts go, it does not get any simpler than selecting stocks solely based on price strength. It also challenges conventional thinking: buy low, sell high. Nonetheless, momentum investing has worked over longer timeframes (see Chart 1), although the approach can suffer painful reversals and has not outperformed in more than two consecutive years since the late 1990s. Academics have struggled to pinpoint why momentum investing succeeds. The performance edge is well-documented with a long track record. A 1993 article in the Journal of Finance is cited as the pioneering study on momentum.1 The authors presented data showing that buying recent stock winners and selling losers produced significantly higher short-term returns than the overall U.S. stock market during the 1965 to 1989 time period. This ongoing performance anomaly could be partly attributed to behavioral factors such as FOMO (fear of missing out) and a bandwagon effect.2 The “Big Mo” might also reflect fundamental strength (rising sales, e.g.) already embedded in prices that can persist in the short-term.

Akin to a snowball rolling downhill, momentum investing is driving ever-larger market capitalizations and a more concentrated U.S. large-cap stock market. As one example, the four largest holdings in the S&P 500 Momentum Index—Amazon.com, NVIDIA, Broadcom, and Meta Platforms—carry a combined market capitalization of $8.2 trillion, greater than the cumulative market cap of roughly the bottom 64% of the S&P 500. Morgan Stanley equity strategist Mike Wilson touched on the intersection between momentum and market concentration in a December note. “Another consideration is the growing propensity of investors to use price momentum as a key factor in their investment strategy. Rebalancing has also been de-emphasized as many investors have let their winners run, given the lack of mean reversion in the past several years. This all helps to explain the extreme concentration we’re seeing in many equity markets, not just in the United States.”3

To borrow from Sir Isaac Newton, momentum is the product of mass times velocity, so perhaps this makes some sense. We have exceptionally large companies moving at a fast pace and creating the momentum that helped lift the S&P 500 Index to a greater than 20% return in 2024 for the third time in the last four years. These market moves have been underpinned by robust asset flows into U.S. equities. According to The Wall Street Journal, investors added over $1 trillion to U.S.-based exchange-traded funds (ETFs) last year, shattering the previous record set in 2021.4 Not surprisingly, momentum ETFs were a popular choice. Invesco’s S&P 500 Momentum ETF pulled in over $3 billion of net purchases over the first 11 months of 2024—incredible growth considering the fund now has around $4 billion under management.5 The hot money trades seeking instant gains may prove ill-timed if the AI trade falters, but until then investors are siding with inertia. As the late New York Yankee great Yogi Berra once said: “Nobody goes there anymore. It’s too crowded.”

The Real Return

A leading kryptonite candidate for the equity markets could be higher-than-expected interest rates. The post-COVID inflation shock still reverberates today, even though the Consumer Price Index (CPI) year-over-year growth rate peaked in mid-2022. As of November 2024, the CPI growth rate was down to 2.7%, a full point below the 50-year average of 3.7%. Price growth has clearly decelerated, but not reversed, and the cumulative impact has made life uncomfortable for policymakers. There is a compelling argument that inflation cast a deciding vote in the recent presidential election. U.S. Federal Reserve Chair Jerome Powell acknowledged in his December press conference that inflation “remains somewhat elevated relative to our two percent longer-run goal.”6 This comment followed after the Fed’s decision to cut the Federal Funds target range to an upper limit of 4.5%, marking a third consecutive easing from its peak of 5.5%.

Any enthusiasm for the (expected) rate cut was quickly doused when Fed watchers realized that the updated Federal Open Market Committee (FOMC) projections implied only two additional rate cuts in 2025. Questioned on this in the press conference, Powell flagged the uncertain inflation outlook. He continued: “And, you know, the point of that uncertainty is it’s kind of common sense thinking that when the path is uncertain you go a little bit slower. It’s not unlike driving on a foggy night or walking into a dark room full of furniture. You just slow down.” An apt metaphor with wonderful imagery, but investors were not impressed. The S&P 500 Index traded down 2.95% in response, the second-worst trading session of 2024 and one of only four greater than 2% daily declines for the year.

Rate anxiety is real. With a more cautious FOMC outlook, the 10-year U.S. Treasury Note yield rose 78 basis points,7 or 0.78%, during the fourth quarter, finishing at 4.57%. The S&P 500 Equal Weighted Index declined 2.3% price-only in Q4, perhaps illustrating the perceived impact of higher rates on the average (smaller) S&P 500 company. Further down the market cap spectrum, the S&P SmallCap 600 Index declined 1.0% over the final quarter of 2024. Ebbing inflation will obviously continue to be a key to interest rate stability in 2025. Without further disinflation progress, bond investors may require a higher real, or inflation-adjusted, return. Longer-term rates may rise regardless, considering our country’s inconvenient $36 trillion (and counting) debt load. This has some analysts watching the horizon for the return of the “bond vigilantes,” those disaffected bond traders who sell bonds—driving yields higher—to signal unhappiness with fiscal and/or monetary policies.

Over the last 30 years, as seen in Chart 2, the median spread between the 10-year U.S. Treasury Note yield and the Fed Funds target rate has been 121 bps. At year-end 2024 the spread was a miniscule 8 bps. The most straightforward path to normalize that relationship is further easing by the FOMC, combined with a steady 10-year yield. However, as the Fed would say, this will all be data dependent. Inflation will need to cool further, which would allow the FOMC to proceed on its intended rate cut plan. Any missteps could result in higher long-term yields, harming not only the bond market, but equities as well. With the S&P 500 Index trading at nearly 22x projected 2025 operating earnings—versus a long-term median of approximately 17x—there is not a lot of room for error.

Steady as She Goes

Although inflation dominated headlines again in 2024, particularly during the run-up to the presidential election, overall U.S. economic growth has been resilient. Gross Domestic Product (GDP) grew at a roughly 3% inflation-adjusted rate over the middle six months of 2024, and is estimated to have decelerated to a still solid 2.4% growth rate in Q4.8 The ongoing struggle to foster economic gains for a wider swath of the population continues. While the service economy chugs along, the goods-producing sector remains stuck in neutral. The Institute for Supply Management (ISM) reported that economic activity in the manufacturing sector declined for a ninth consecutive month in December.9 ISM’s survey has actually indicated a manufacturing contraction for 25 of the last 26 months, although the December reading did include some green shoots with new orders and production both in expansion territory.

The U.S. economy is much more dependent on services than goods, of course. In 2023, over 67% of Personal Consumption Expenditures (PCE) went to services, with goods accruing the other 33%.10 According to BlackRock’s Rick Rieder, head of global asset allocation, we may be needlessly worrying about whether the economy will experience a hard or soft landing. Instead, he suggests we think about the U.S. economy as a satellite: “Satellites don’t land. They just get tired over time, and they need a bit more energy…The Fed raises rates 500 basis points, and it doesn’t make a difference, and it’s because the service economy is not cyclical. Goods are hugely cyclical.”11

1 “Momentum Investing: It Works, But Why?”, www.anderson-review.ucla.edu/momentum, 10/31/2018.

2 “Momentum Investing: what it is, why it works and what to buy,” www.moneyweek.com, 6/15/2018.

3 “What Is Breadth Telling Us?”, Morgan Stanley Research Sunday Start, 12/22/2024.

4 “A Record-Shattering $1 Trillion Poured Into ETFs This Year,” www.wsj.com, 12/30/2024.

5 “Investors Are Looking to Momentum ETFs in 2024,” www.etftrends.com, 11/29/2024.

6 “Transcript of Chair Powell’s Press Conference,” www.federalreserve.gov, 12/18/2024.

7 A basis point (bp) is 0.01%.

8 GDPNow, www.atlantafed.org, 1/3/2025.

9 “Manufacturing PMI® at 49.3%,” www.ismworld.org, 1/3/2025.

10 “Gross Domestic Product (Third Estimate), Third Quarter 2024,” www.bea.gov, 12/19/2024.

11 “DealBook: R.T.O. battle,” www.nytimes.com, 10/12/2024.