Monday Macro with Dave - Parsing signals from noise in job reports and the labor market

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Parsing signals from noise in job reports and the labor market

Dave Harrison Smith, CFA

Chief Investment Officer

March 30, 2026

Markets are increasingly pricing in a more prolonged Middle East conflict and sustained pressure on energy prices. Our focus remains on how that transmits through to markets and portfolios. A key starting point is the condition of the U.S. economy heading into the conflict.

This week’s data, including retail sales, ISM manufacturing, and labor reports from ADP, Challenger, and the Bureau of Labor Statistics (BLS), should help establish that baseline.

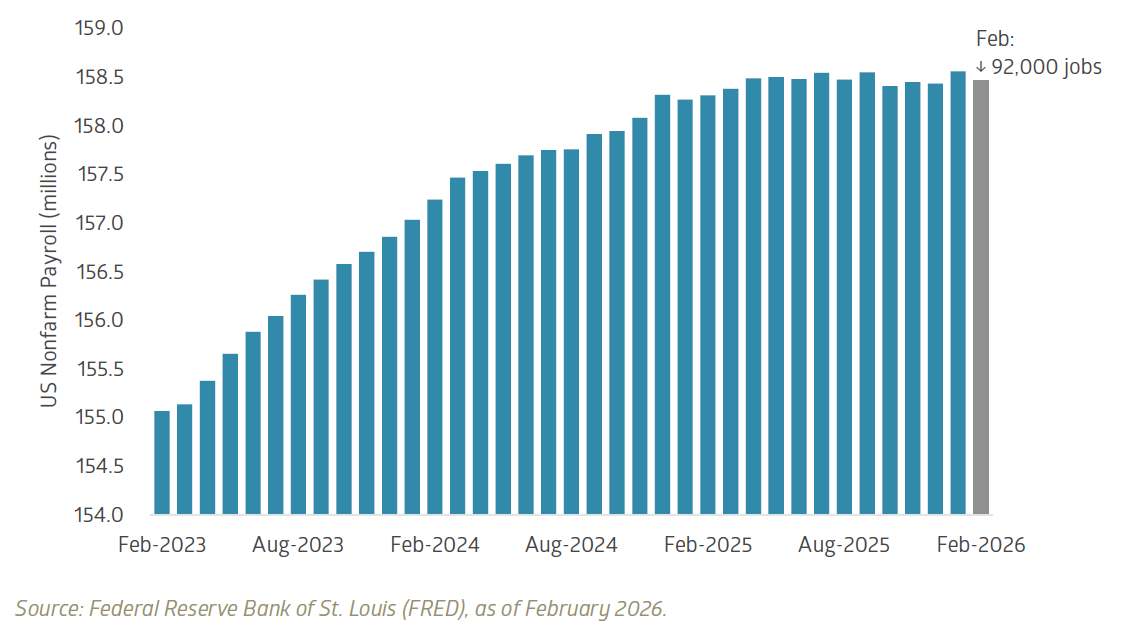

Last month’s Nonfarm Payrolls report from the BLS missed expectations by a wide margin, showing a decline of 92,000 jobs versus forecasts for a modest gain of 55,000. The release raised concerns about labor market weakness heading into the Iran conflict and briefly reignited discussion around “stagflation.” It also ran counter to the prevailing view that the labor market was cooling, but not breaking.

Payroll miss likely reflects strikes and weather, not a trend break

Importantly, the February BLS data included several one-time distortions, including labor strikes and severe weather. Other indicators, such as ADP data and unemployment claims, have shown more resilience in recent weeks. That said, layoffs have picked up at the margin, with announcements from UPS, Meta, and Amazon in the first quarter. The next BLS report, due Friday, will carry added weight.

Stagflation concerns in context

Concerns around stagflation have risen sharply in recent weeks. Defined as weak growth alongside elevated inflation, the concept remains anchored in the oil shocks of the 1970s.

Federal Reserve Chair Jerome Powell pushed back on that comparison following last week’s Federal Open Market Committee (FOMC) meeting, noting today’s backdrop of roughly 3% inflation and 4% to 4.5% unemployment stands in stark contrast to the double-digit levels seen in that era. As he put it, “I would reserve the term stagflation for a much more serious set of circumstances. That is not the situation we’re in.”

Still, the tension is real. The Fed’s dual mandate is being tested by an energy shock that could push inflation higher while weighing on growth. That dynamic has been enough to pressure equity valuations, even as earnings expectations remain strong. With valuations already elevated, there has been little room for error.

As Kenneth Rogoff noted in the Financial Times:

“Coming on top of the ongoing Ukraine and tariff wars, the Iran war is shaping up as the biggest stagflationary shock the world has seen in five decades.”

Rising deficits, rising yields, fewer hedges

Global bond yields have continued to trend higher since the onset of the Iran conflict. Last week saw the U.S. 10-year reach 4.44%, Germany’s bund rise to 3.10%, and Japan’s JGB to 2.34%, while the U.K. gilt was a modest exception, easing slightly to 4.92%.

Deficit concerns remain front and center. The U.S. was already projected to run deficits of 5% to 7% of GDP in the coming years. Add higher energy prices, geopolitical uncertainty, and policy constraints, and confidence in those projections has started to erode.

The result is a more challenging environment for diversification. Equities have faced valuation pressure, while bonds, typically viewed as a ballast, have also struggled as yields rise and prices fall. The Bloomberg Aggregate Index is down 2.49% month-to-date and 0.79% year-to-date. Modest in absolute terms, but notable given the volatility elsewhere.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Country Indices Flash Report – March 2026

U.S. and Israeli strikes on Iran disrupted shipping through the Strait of Hormuz, a key energy chokepoint. Equities fell, while oil and gas prices spiked. [[ READ MORE ]]

Monday Macro with Dave - Markets reprice on rapid policy shifts

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Markets reprice on rapid policy shifts

Dave Harrison Smith, CFA

Chief Investment Officer

March 23, 2026

Policy signals are driving market swings

Markets have swung sharply over the past 72 hours, driven less by fundamentals and more by policy signals.

Late Friday, oil prices surged on news of escalation in the Middle East, alongside President Trump’s threat of potential strikes on Iranian energy infrastructure. By early Monday, that tone reversed, with a pause on military action following reported discussions with Iranian counterparts. Iran has since pushed back, denying meaningful progress.

This kind of whiplash is not new. It echoes April 9, 2025, when markets sharply rebounded after a sudden tariff reprieve. The S&P 500 rose 9.5% in a single session. Policy-driven reversals can be abrupt and non-linear. A single tweet can move mountains.

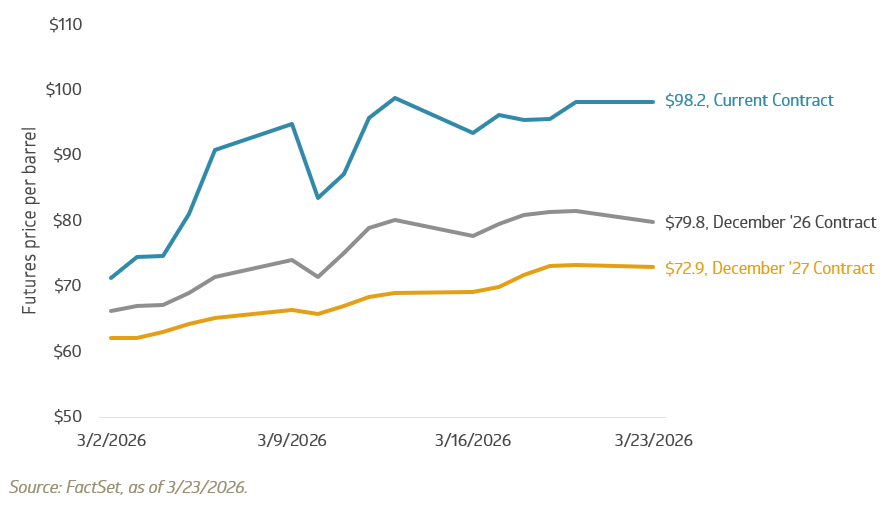

Oil markets are still pricing a de-escalatory base case, with futures below $80 per barrel by year-end and closer to $70 by late 2027. That baseline remains vulnerable to escalation, infrastructure damage, or a more prolonged conflict.

Crude oil WTI futures pricing remains below escalation scenarios

Rising oil prices are already showing up in bond markets

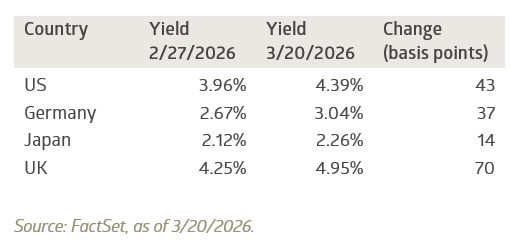

Higher energy prices raise the risk of persistent inflation. That, in turn, is pushing yields higher. Yields have moved higher across major economies as markets reprice a combination of higher inflation, elevated growth risk, and sustained fiscal deficits. As of last week, the U.S. 10-year reached 4.39%, with similar moves across Germany, Japan, and the UK.

Global 10-year yields have moved higher

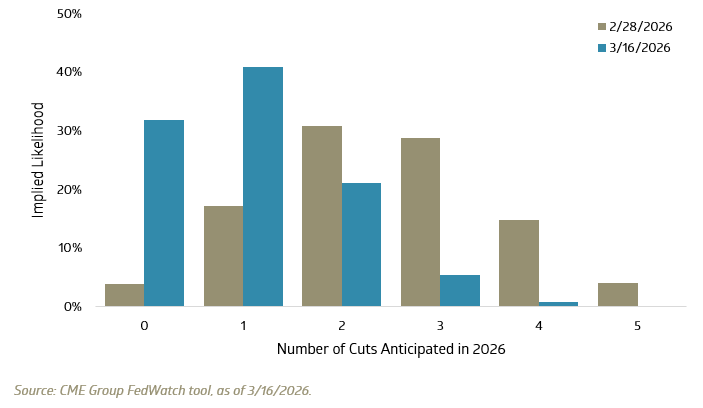

Short-term yields tell the same story. Just one month ago, futures markets implied a 92% probability of at least one Fed cut, with 2–3 cuts as the most likely outcome. Today, that has shifted materially. Markets now imply a 70.9% probability of zero cuts, with roughly equal odds of either one cut or one hike.

At the start of the year, the expectation was for steady easing. That path now looks less certain. Sticky inflation, geopolitical risk, and the potential pass-through from higher energy prices are all pushing in the same direction.

The outlook has become less linear

The year began with a clear expectation of easing monetary policy. That view has been challenged.

Tighter policy and higher anticipated borrowing costs are starting to show up across equity valuations, bond markets, and investor sentiment. At the same time, uncertainty around inflation and geopolitics is narrowing the range of likely outcomes.

Instead of a clean easing cycle, markets are now adjusting to a more conditional path forward. Policy decisions and external shocks are playing a larger role than many expected at the start of the year.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Rising energy prices test the consumer and the Fed

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Rising energy prices test the consumer and the Fed

Dave Harrison Smith, CFA

Chief Investment Officer

March 16, 2026

Energy prices rise, consumer holds for now

The conflict in the Middle East continues, with no clear path to de-escalation. Oil has moved higher, with WTI crude closing Friday near $100 per barrel. U.S. gas prices have also risen sharply, with the national average reaching $3.80 per gallon, up from below $3.00 pre-conflict (source: gasbuddy.com).

Markets, for now, appear to be pricing in a relatively contained and short-lived disruption. Even in best-case scenarios, damage to Gulf infrastructure will likely take months to repair and return to full capacity. As a result, many analysts expect oil prices to remain elevated for much of 2026. Sustained higher energy prices feed into inflation and add pressure on consumers through rising fuel costs.

Encouragingly, the consumer entered March in solid shape. High-frequency spending data from Bank of America showed strong trends in February, and commentary from Visa and Mastercard was broadly constructive at recent investor conferences. Even discount retailer Dollar General reported strong earnings, noting that spending remains “pretty resilient from a consumer perspective.”

Historically, energy shocks act as a tax on consumers. The longer prices remain elevated, the greater the risk of demand shifting away from discretionary categories. The key question is durability.

Sticky inflation complicates the Fed’s path

The Federal Reserve faces a challenging backdrop. Energy prices have surged and will likely pressure inflation in the coming months. While the Fed has historically looked through supply-driven inflation and focused on underlying demand, inflation remains sticky and above target even before the recent escalation.

The February CPI release was mixed. Inflation has moderated but remains above the Fed’s 2% target, with core CPI rising at a 2.5% annualized pace. The read-through to the Fed’s preferred inflation gauge, PCE, may point to somewhat higher inflation given its different basket of goods. Importantly, this data does not yet reflect the recent increase in energy prices.

Inflation remains persistent, and markets have adjusted accordingly. Futures markets now price in between zero and one rate cut for the remainder of 2026.

Number of rate cuts expected in 2026, as implied by market futures

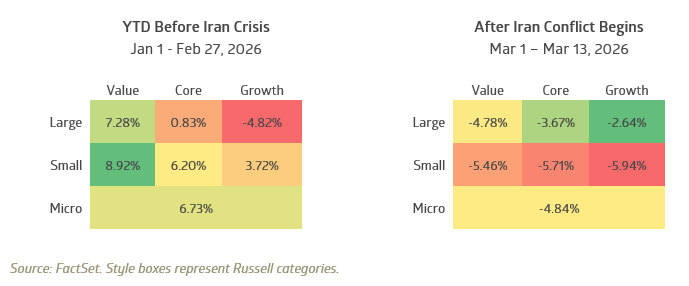

Market leadership shifts following the start of the conflict

Market leadership has shifted alongside changing rate expectations and rising economic uncertainty. For the first two months of the quarter, small-cap and value stocks outperformed, with small-cap value rising nearly 9% through the end of February. Large growth, dominant in recent years, lagged, with the Russell 1000 Growth Index down 4.8%.

Style returns, before and after the start of the Iran conflict

As the conflict escalated, that leadership dynamic began to reverse. Large-cap growth stocks, while still negative, have held up relatively better. Small-cap stocks have lagged across growth, core, and value styles, reflecting greater sensitivity to economic growth and financial conditions.

The earlier strength in small-cap and value reflected a broadening of participation across U.S. equities. Markets are now re-pricing both economic growth and interest rate expectations in real time.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Oil Surges and Markets Reprice

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

The Gulf erupts, oil surges, and markets reprice

Dave Harrison Smith, CFA

Chief Investment Officer

March 9, 2026

The Strait of Hormuz closes and oil surges 60%

The situation in the Middle East has devolved into a fierce and sprawling military conflict. Iran’s response to continued Israel/U.S. strikes has entangled a dozen other countries, with tens of thousands killed or injured, civilian infrastructure shuttered, and energy production and transportation facilities abruptly offline.

Over the past week, the conflict has broadened well beyond initial expectations. This is not a repeat of the targeted strike on Iran’s nuclear facilities in 2025. Iran’s response has drawn in a wide swath of major energy-producing countries. Critically, the Strait of Hormuz—through which roughly 20%/30% of global oil/natural gas supply flows—has effectively closed to shipping traffic. Production shutdowns across Kuwait and other countries reflect not just fear of direct strikes, but a breakdown in transportation and available storage capacity. Systemic complexity is amplifying the energy disruption in ways not fully anticipated.

The impact on oil prices has been dramatic and swift. West Texas crude has spiked from $66.96/barrel at the end of February to above $110 as of this writing. At an increase of over 60%, this places it among the largest six-day moves in three decades and second only, in dollar terms, to the immediate aftermath of the COVID shutdown in 2020. Average U.S. gasoline prices have risen more than $0.50 per gallon in a single week, with further increases likely. Jet fuel has surged as well, foreshadowing higher travel costs heading into summer. Businesses and consumers are reeling.

U.S. equities hold; international markets and bonds sell off

Beyond commodity prices, the financial market reaction has been significant. U.S. equities have been relatively resilient, reflecting the United States’ position as a major energy producer since the shale boom, with the S&P 500 Index down 2.0% and the Russell 2000 Index down 4.0% on the week. International markets have fared worse: the EAFE Index fell 6.7%, and Emerging Markets declined 6.9%, reflecting both the global growth risk from spiraling energy costs and the impact of a strengthening U.S. dollar, which has functioned as a safe-haven currency.

Government bonds have also broadly sold off, failing to provide refuge. Yields on the U.S. 10-Year Treasury increased to 4.15% last week, up from 3.96% at the end of February, while the 2-Year rose from 3.39% to 3.57%. These moves reflect elevated inflation fears and a reduced likelihood of Federal Reserve rate cuts. The market is now pricing in a single cut in 2026, down from the two to three cuts anticipated just last week.

Energy price shocks create a complex dynamic. Headline inflation rises directly; so too does core inflation, as fuel and electricity costs are absorbed into the production costs of goods and services broadly. At the same time, sustained energy price increases tend to compress consumer spending, particularly among lower-income households, where food and fuel represent a disproportionate share of the budget. Our research suggests this segment of the economy is already under meaningful financial stress, and the current shock will deepen that pressure.

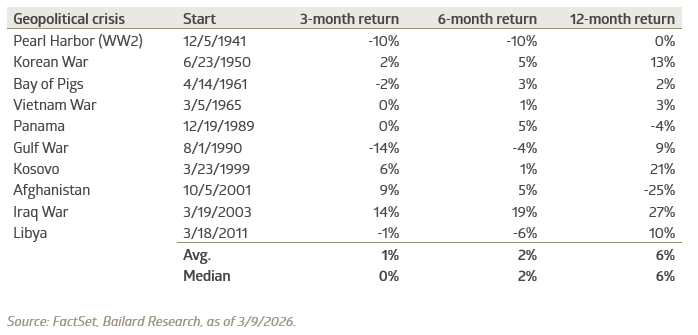

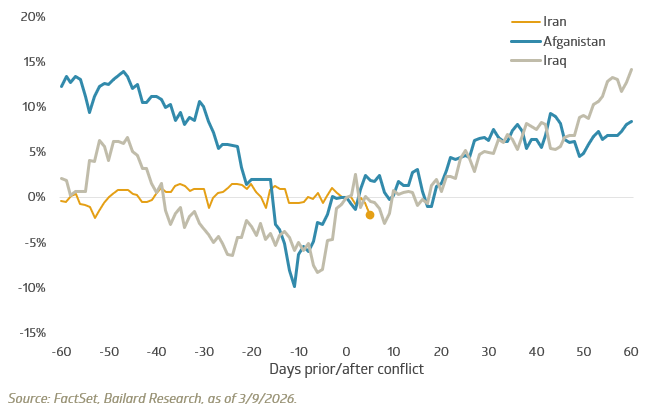

What history says about markets after geopolitical shocks

The news flow remains difficult, and volatility is elevated. A key question worth considering: how much risk is already priced into current market levels? The history of geopolitical events offers useful and heartening context. Past events have often followed a similar pattern: an initial repricing as uncertainty spikes, followed by stabilization and recovery as the situation becomes more legible to markets. The S&P 500 has frequently produced positive returns over the three-, six-, and twelve-month periods following major geopolitical crises, illustrating how quickly these shocks can be absorbed into market expectations.

Market returns following major geopolitical crises

Looking at recent Middle East conflicts specifically, the S&P 500 posted positive average returns over each of these time horizons, rising 11.5%, 12%, and 1% over 1-, 3-, and 12-month periods, respectively. The sample size is limited, and each conflict’s surrounding economic and geopolitical environment is different. This history is best understood as descriptive context, not a forward-looking projection.

S&P 500 Index price return around onset of select conflicts

We remain focused on where risk is concentrated and where dislocations may be surfacing opportunity. Our emphasis on quality across strategies is designed to provide relative resilience in periods like this. We continue to evaluate exposure in areas most sensitive to sustained energy cost increases—across regions, sectors, and individual companies—while remaining alert to the pricing anomalies that fear and volatility tend to create.

In our experience, periods of acute uncertainty often obscure the eventual recovery. When markets begin to anticipate stabilization, recoveries can unfold quickly and well in advance of any formal resolution. In periods of elevated uncertainty, patience and discipline remain among the most durable investment advantages.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Monday Macro with Dave - Escalation Abroad & Stress in Credit

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Escalation Abroad and Emerging Stress in Credit

Dave Harrison Smith, CFA

Chief Investment Officer

March 2, 2026

The Middle East explodes into war

Over the weekend, the region collapsed into a situation investors had feared. The U.S. and Israel conducted a barrage of strikes against Iran, while Iran retaliated against not only Israel but also against Qatar, the UAE, Saudi Arabia, Kuwait, Bahrain, and even a U.K. base in Cyprus. In short order, the region descended into a multi-front conflict with potential global consequences.

I won’t repeat the military or humanitarian details; those are readily available elsewhere. Instead, I’ll focus on what it may mean from a financial perspective.

Oil and energy prices will be the primary conduit through which we see economic and market impact. Iran produces roughly 3 million barrels of oil per day, about 3% of global production. The country also sits on the critical Strait of Hormuz, the chokepoint waterway through which an estimated 15% to 20% of global oil supply flows by tanker. Traffic through the Strait has already slowed to a trickle as shipping companies and insurers evaluate risks. While some disruption could be mitigated in the short term via pipelines and alternative ports, they simply cannot fully replace Hormuz volume. A lengthy shutdown would have significant repercussions for global energy prices.

Thus far, the initial market reaction looks textbook, if subdued. Traditional safe havens including gold, the U.S. dollar, and the Japanese yen are higher, while risk assets such equities are modestly lower. Defense and energy stocks are surging. Oil has traded in the mid-$70s to low-$80s per barrel range, up roughly 5% to 13% from recent levels. Airline stocks are notable underperformers, as a wide corridor of Middle Eastern airspace has been shuttered and one of the world’s busiest airports, Dubai International, was hit by a missile strike. Investors may wonder why the market reaction has not been more severe. That may reflect some prior anticipation of a conflict, as seen in the recent decline in safe haven 10-year U.S. Treasury yields from 4.26% at the start of February to 3.96% last week.

This is clearly a major geopolitical event. The human cost will be enormous, and the path of nations will be determined. Economically, the trajectory for risk assets will depend on both the duration and severity of global disruption. Elevated energy prices feed into inflation in the near-term and higher gas prices crimp consumer spending, particularly among lower-income households where financial stress is already visible. A swift resolution could lead to a return to normalcy. This morning, though, an off-ramp seems unlikely.

Block, formerly Square, announced it will slash workforce by nearly 50%, citing AI productivity gains

This adds fuel to an already contentious debate on the impact of AI on the job market. Block CEO Jack Dorsey was direct: “A significantly smaller team using the tools we’re building can do more and do it better…I don’t think we’re early to this realization. I think most companies are late. Within the next year, I believe the majority of the companies will reach the same conclusion and make similar structural changes.”

There are important caveats. Block expanded aggressively after the pandemic, growing from roughly 2,000 employees to 10,000. While many peers course corrected and reduced payroll in 2023/2024, Block has maintained its elevated employee count. The company has also been criticized by Wall Street for under-earning relative to peers, with adjusted operating margins in the low 20% range against a peer group running 35% to 40% or more.

So, we question: is this actually AI-driven workforce replacement or a company-specific rationalization dressed up with an AI narrative?

The true answer is likely nuanced. One fact worth mentioning: software job postings on Indeed are actually up 11% year over year. The picture is clearly more complicated than at first blush but the implications to our world are significant.

Private credit back in the news… another cockroach in the system

We have previously written about recent implosions in the private credit space, including First Brands and Tricolor. Those collapses caused significant write-downs at several large investment firms and regional banks. At the time, JP Morgan CEO Jamie Dimon commented that there were likely more ‘cockroaches’ in the system.

Last week, the industry found another one. U.K.-based mortgage provider MFS abruptly collapsed amid fraud allegations that the lender had ‘double pledged’ collateral. Investors in MFS include Elliot Management, with a roughly $200 million investment, as well as Barclays, Jefferies, and Apollo Global.

This impact may extend beyond the headline. Over the last five years, investor capital has flooded private credit chasing high yields and strong returns. Our concern is that investment firms loosened underwriting criteria in a rush to deploy capital. Combined with growing pressure in private equity, where many portfolios have considerable exposure to AI-disrupted software firms, there is potential for significant write-downs. Insurance companies and pension funds have deep exposure to both private equity and private credit.

Black swan, systematic events rarely announce themselves politely. This is an area we are monitoring closely.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

Country Indices Flash Report – February 2026

Japanese Prime Minister Takaichi convincingly won a snap general election. Her party’s two-thirds lower-house majority—the first post-war instance achieved without a coalition partner—gives her broad latitude to shape policy.

Sonya Mughal Named Women in Wealth Advocate of the Year at 2026 Private Asset Management Awards

About Sonya Mughal

Sonya became Chief Executive Officer of Bailard in April 2021, after nearly three decades at the firm. She is the first woman and first person of color to lead the company. Her leadership is marked by consistency and fairness, along with a clear expectation that decisions be both thoughtful and well reasoned.

"Wealth management is stronger when more women are part of it. As advisors, as leaders, and frankly, as clients,” said Mughal. “I am deeply honored, but this truly belongs to the Bailard team. Nearly half of our senior leaders are women, and that is no accident. It is what happens when people are genuinely committed to doing what is right."

Women in Leadership at Bailard

As of December 31, 2025, 48% of Bailard's VPs and above are women. That figure speaks to steady hiring, promotion, and retention decisions over time.

One of the firm’s more tangible practices is pay transparency. Managers understand that compensation decisions must be clear and defensible. That discipline encourages open conversation and reduces ambiguity around advancement, an area where finance has not always been consistent.

For clients, that consistency supports stable teams and clear processes. For employees, it creates a more transparent path for growth.

“The conversations I have with clients are different here,” said Lena McQuillen, CFP®, Vice President and Director of Financial Planning at Bailard. “There is a level of trust that comes from working with a firm that genuinely walks the talk, and you really do get to make a difference in people’s lives.”

About the Private Asset Management Awards

The Private Asset Management Awards recognize firms and individuals across the private wealth management space. The 2026 awards ceremony brought together senior decision-makers from family offices, multi-family offices, private banks, and wealth management firms across the United States. Winners are selected by an independent panel of industry professionals.

In addition to Mughal’s individual recognition this year, Bailard’s Chief Investment Officer Dave Harrison Smith, CFA, was shortlisted for Manager or Investment Research Professional of the Year. The firm was also shortlisted in prior years for Best Philanthropic Initiative and Women in Wealth Advocate of the Year - Company.

About Bailard, Inc.

Bailard is an independent firm that has served individuals, families, and institutions since 1969 with comprehensive wealth management and disciplined asset management solutions. Our work is rooted in clear values, long-term thinking, and a steady commitment to putting clients first. Across the firm, we provide financial and wealth planning, portfolio management, and asset management strategies spanning domestic and international equities, fixed income, sustainable and responsible investing, private real estate, and customized mandates. The firm manages more than $7.7 billion in assets as of December 31, 2025.

Bailard is a Certified B Corporation™ and signatory to the UN Principles for Responsible Investing. We are built on accountability, compassion, and a long-term commitment to doing what’s right for our clients. Learn more at bailard.com, and explore career opportunities at bailard.com/careers.

# # #

Leadership statistics as of 12/31/2025. Bailard does not endorse or control, either expressly or implicitly, the content posted by any third party and disclaims all comments made or information provided by non-Bailard employees. These recognitions do not evaluate the quality of services provided to clients and are not indicative of Bailard’s future performance. There was no cost to enter. The Private Asset Management Awards 2026 judging process is designed to be rigorous and thorough to ensure all entries receive full consideration and that excellence in each of the categories is truly rewarded. A mix of leading wealth managers, advisors/consultants, service providers, and other industry experts make up the judging panel. Presented by With Intelligence, part of S&P Global, winners were announced in February 2026. Additional information is available here: https://awards.withintelligence.com/privateassetmanagementaward/en/page/2026-winners.

Monday Macro with Dave - Growth Miss and Renewed Tariff Risk

Monday Macro with Dave

Weekly perspective on current developments, emerging risks, and potential implications for investors.

Growth Miss and Renewed Tariff Risk

Dave Harrison Smith, CFA

Chief Investment Officer

February 23, 2026

GDP growth came in very light for Q4, inflation also above target.

Raymond James described this as an “anti-goldilocks” report. GDP disappointed, rising 1.4% for the quarter versus 2.8% consensus expectations. Headwinds included the government shutdown and a disappointing quarter for retail spending, while business investment provided some upside offset.

Alongside the GDP release, inflation data showed price pressures remain slightly elevated. The Personal Consumption Expenditures Index , or PCE, which is the Fed’s preferred measured of inflation, rose 2.9% year-over-year versus consensus at 2.8%. Core PCE, which excludes food and energy and is viewed as a better gauge of underlying inflation trends, increased 0.4% month over month. That monthly page suggests inflation remains sticky beneath the surface. Investors are now pricing in two Fed rate cuts by year-end 2026.

The Supreme Court rejection of Trump’s use of IEEPA to implement tariffs was by far the biggest news of the week.

Over the weekend, Trump posted on Truth Social that his tariffs would indeed increasing from the 10% level he indicated last week to the maximum 15% allowed under Section 122. Recall that Section 122 allows for up to 15% global tariffs for a maximum of 150 days. Market reaction was negative Monday morning, as traditional safe havens like precious metals and international stocks held steadier.

Technology stocks were volatile over the week.

Anthropic released Claude Code Security, a coding agent designed to identify and suggest fixes for vulnerabilities. Despite limited overlap with existing products from major cybersecurity vendors, the announcement sent cyber stocks sharply lower.

Blue Owl, a large private credit manager involved in financing several AI data centers, saw shares plummet after halting outflows in one of its retail-focused funds. That pressured Oracle and Coreweave shares and coincided with reports that Blue Owl was struggling to secure financing for certain data center partnerships.

Finally, OpenAI was reported to be near closing a $100 billion financing round valuing the company at $800 billion. The company is reportedly materially lowering its projected spending , telling investors that it plans to spend $600 billion instead of the $1.4 trillion Sam Altman had bragged about last year. Encouragingly, after its “code red” in December, user growth has reportedly re-accelerated and reached new highs in 2026. OpenAI generated $13 billion in revenue in 2025 and is projecting $280 billion by 2030.

# # #

Past performance is no indication of future results. All investments have the risk of loss.

The information in this publication is based primarily on data available as of its publication date and has been obtained from sources believed to be reliable, but its accuracy, completeness, and interpretation are not guaranteed. Bailard undertakes no duty to update any of the information contained herein, and such opinions are subject to change without notice. We do not think this publication should necessarily be relied upon as a sole source of information and opinion. This publication is not a recommendation of, or an offer to sell or solicitation of an offer to buy any particular security or investment product. It does not take into consideration the particular investment objectives, financial situations, or needs of individual clients.

Any indices or other financial benchmarks referenced are provided for illustrative purposes only. Indices are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Any individual securities referenced herein are for illustrative purposes only and not necessarily representative of investments that have been made or will be made in the future. Bailard, Inc. makes no recommendation to buy or sell securities discussed herein. Bailard clients may hold positions in the securities discussed and may buy or sell such securities at any time.

Certain information may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Bailard, Inc. does not provide investment advice in jurisdictions where it is not authorized to do so.

CNBC: "Tech IPO hype gets drowned out on Wall Street by prospect of $1 trillion in debt sales"

Dave Harrison Smith, CFA, as source in a recent article published by CNBC.