Understanding Section 530A Accounts

When new savings rules are introduced, families often ask a simple question: Is this right for us? The recently created Section 530A account, also known as a “Trump Account,” is no exception.

While the name has drawn attention, the more practical question is how this account fits alongside familiar options such as 529 plans, custodial accounts, and Roth IRAs for children. Like most planning tools, 530A accounts come with trade-offs, and understanding those trade-offs helps families decide whether, and how, this option belongs in a broader strategy.

This article explains how 530As work, where they may fit, and how to think about them alongside other savings tools when deciding where to save for a child.

What Is a 530A Account?

530A accounts are designed to encourage long-term saving and investing for children under age 18. They share some characteristics with traditional IRAs in that contributions and investment earnings grow tax-deferred.

530A accounts are designed to encourage long-term saving and investing for children under age 18. They share some characteristics with traditional IRAs in that contributions and investment earnings grow tax-deferred.

What makes these accounts distinct is how they are funded, invested, and accessed during childhood. Until the year a child reaches age 18, 530As follow special rules that do not apply to traditional IRAs. Beginning in the age-18 year, the account transitions and becomes subject to the standard traditional IRA rules.

How 530A Accounts Are Funded

Contribution rules are one of the most important distinctions between 530A accounts and other savings vehicles for children. Contributions may come from several sources, with different rules applying before and after age 18.

Federal Contribution

Eligible children born between January 1, 2025, and December 31, 2028, may receive a one-time $1,000 Federal contribution. The child must be a U.S. citizen with a valid Social Security number, and an election must be made on IRS Form 4547. Although eligibility is tied to births beginning in 2025, contributions cannot be made before July 4, 2026.

Personal Contributions

Parents, grandparents, or any other individuals may contribute on a child’s behalf. Unlike traditional and Roth IRAs for children, earned income is not required, and there are no income limits for contributors. Total personal contributions from all sources are capped at $5,000 per year (lower than traditional and Roth IRA limits) and must be made by December 31 of the applicable year. Personal contributions are made with after-tax dollars and are not deductible.

Employer Contributions

Employers may contribute up to $2,500 per year for an employee or an employee’s dependent. These contributions count toward the $5,000 annual personal contribution limit and are not included in the employee’s taxable income.

Governmental and Charitable Contributions

Governmental and Charitable Contributions

Certain governmental entities and charitable organizations may also contribute to 530A accounts for a qualified class of beneficiaries under age 18. These contributions are not subject to dollar limits and do not count toward the annual personal contribution cap.

Contributions Beginning at Age 18

In the age-18 year, 530A accounts transition to a standard traditional IRA framework. Contributions must be supported by the beneficiary’s earned income and are subject to standard IRA limits and deductibility rules.

Investment Rules

While the beneficiary is under age 18, 530A accounts are limited to low-cost mutual funds or ETFs that track the S&P 500 Index, or other qualifying U.S. equity indexes. Individual securities, sector-specific funds, and fixed income investments are not permitted during this period.

Beginning in age-18 year, these restrictions are lifted and the account may be invested like any other traditional IRA, allowing for greater flexibility and alignment with the beneficiary’s time horizon, risk tolerance, and financial goals.

Access and Tax Treatment

530As are subject to a strict lock-up period during childhood. No withdrawals are permitted before age 18, and there are no hardship or special exceptions.

Beginning January 1 of the year the beneficiary turns 18, funds may be withdrawn for any purpose. Distributions generally follow traditional IRA rules, including ordinary income taxation and a potential 10% early withdrawal penalty before age 59½, unless an exception applies. 530A accounts are also subject to required minimum distribution (RMD) rules.

Personal contributions are made with after-tax dollars and create basis in the account. These amounts are not taxed again when distributed, though earnings are taxable and subject to early-withdrawal penalties. Contributions from the Federal government, employers, and charitable organizations (and earnings from these contributions) are treated as pre-tax dollars and are fully taxable when distributed.

All distributions follow pro-rata rules, meaning each withdrawal reflects a mix of taxable and after-tax amounts, rather than allowing personal contributions to be withdrawn first. This calculation applies only to the 530A account itself and does not aggregate other traditional IRAs.

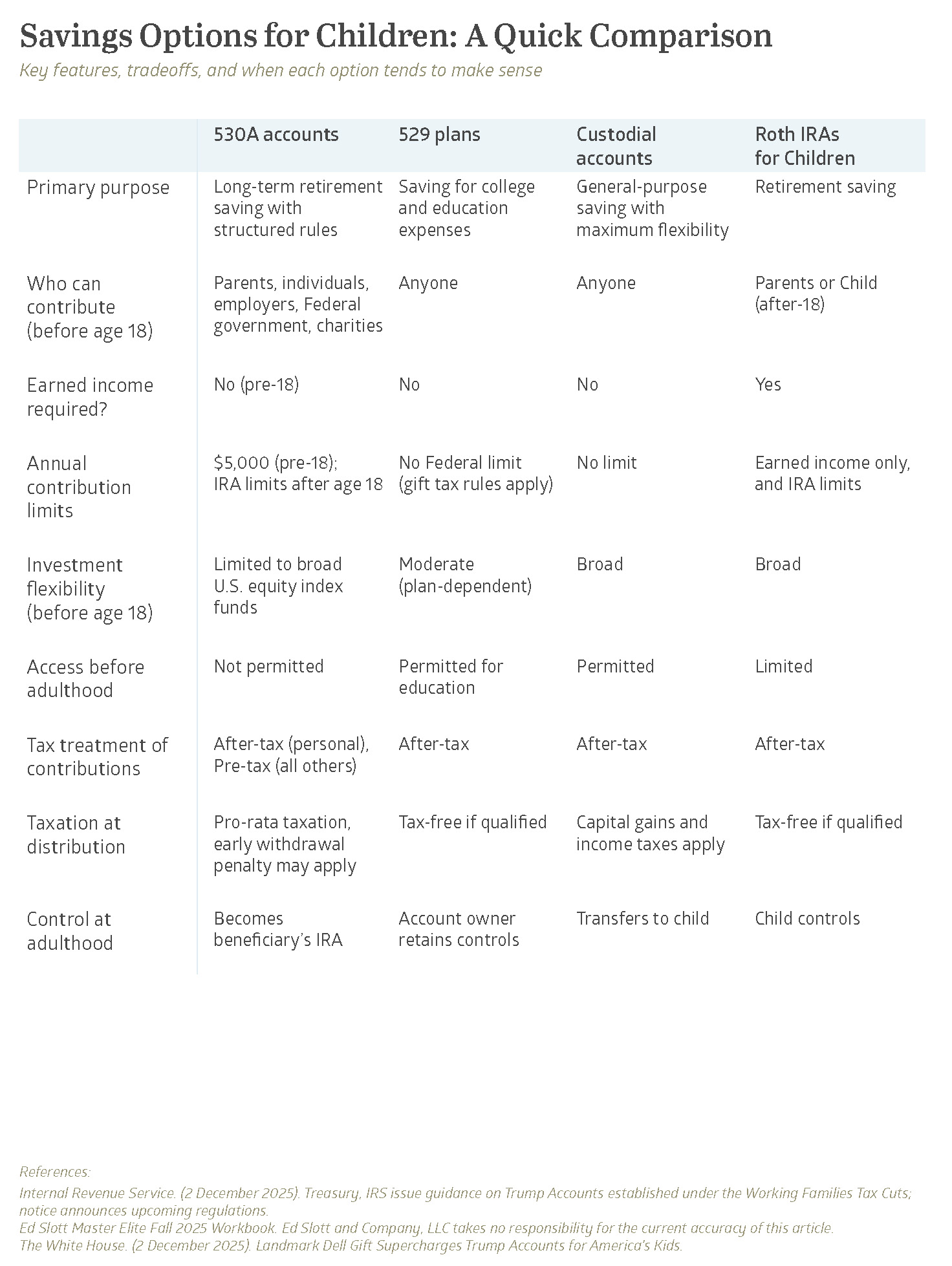

How 530A Accounts Compare to Other Options

Families typically have several tools available when saving and investing for children, each designed for different goals and tradeoffs. The right choice depends on how flexible the funds need to be, how they are expected to be used, and when access may be required.

At a high level:

- 530A accounts emphasize long-term growth with limited flexibility during childhood.

- 529 college savings plans are designed specifically for education-related expenses and often offer the most favorable tax treatment.

- Custodial accounts (UTMA/UGMA) provide broad flexibility but transfer control to the child at the age of majority.

- Roth IRAs for children can be effective when earned income is available and retirement savings is a priority.

The table below summarizes key differences across these options to help frame the trade-offs at a glance. In practice, many families use a combination of strategies rather than relying on a single account type.

Final Thoughts

While they add a tax-advantaged planning option for families, Trump Accounts are not a universal solution. Their usefulness depends on a family’s goals, time horizon, and how much flexibility is needed during childhood.

530A accounts are best viewed as a complement to existing strategies such as 529 plans, custodial accounts, or Roth IRAs for children. In many cases, the most effective approach is not choosing one account over another, but understanding how different tools can work together based on how and when funds are expected to be used.

# # #

# # #

References:

Internal Revenue Service. (2 December 2025). Treasury, IRS issue guidance on Trump Accounts established under the Working Families Tax Cuts; notice announces upcoming regulations.

Ed Slott Master Elite Fall 2025 Workbook. Ed Slott and Company, LLC takes no responsibility for the current accuracy of this article.

The White House. (2 December 2025). Landmark Dell Gift Supercharges Trump Accounts for America’s Kids.

Avoiding Crypto Probate

Cryptocurrency ownership has grown rapidly, and many people now hold Bitcoin, Ethereum, Solana, and other digital assets in wallets or on exchanges, such as Coinbase. Yet estate planning for these assets can be challenging. Unlike most traditional assets, cryptocurrency lacks a straightforward titling or beneficiary framework, which means it does not always fit neatly into conventional revocable trust planning.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

When planning is incomplete, trustees may face delays in accessing cryptocurrency, court involvement through probate, or loss of privacy—precisely the outcomes a revocable trust is designed to avoid.

Why Cryptocurrency Requires a Different Approach in Revocable Trust Planning

Traditional assets can often be placed into a revocable trust by changing legal title. A home can be deeded into a trust. A brokerage account can be retitled. Certain assets, such as life insurance policies, generally do not require retitling and instead name the revocable trust as the beneficiary.

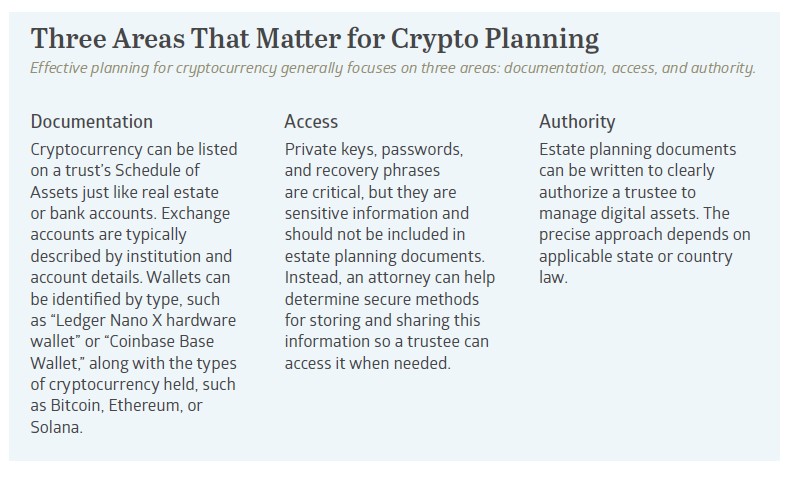

Other assets are handled differently. Tangible personal property—such as artwork, antiques, or collectibles—is commonly addressed by listing the asset on the trust’s Schedule of Assets and, in many cases, by executing a general assignment of personal property. These assets are not retitled in the traditional sense, but they are still brought within the trust’s asset base.

Cryptocurrency fits within revocable trust planning in a similar way, but with an added layer of complexity driven by how the asset is held. For estate planning purposes, the critical distinction is whether cryptocurrency is held directly by the individual in a self-custody wallet or held with an institutional custodian through an exchange account.

Wallets vs. Exchange Accounts

Self-custody wallets such as Ledger, Trezor, MetaMask, or Coinbase Base Wallet are controlled directly by the owner through private keys. There is no institution standing between the individual and the blockchain, which is a decentralized, secure digital ledger that transparently records transactions.

Because there is no traditional “title” to change, bringing wallet-held cryptocurrency into a revocable trust is typically handled by:

- Listing the wallet on the trust’s Schedule of Assets, and

- Executing an assignment of digital assets.

When done properly, a trustee can step in and manage these holdings directly without probate or other court involvement. What wallets generally do not allow is conversion into dollars or other fiat currencies. To liquidate, assets often must be transferred from the wallet into an exchange account.

Exchange accounts operate differently. Personal cryptocurrency exchange accounts generally cannot be held in the name of a revocable trust. Instead, the exchange functions as an institutional custodian and controls the private keys on behalf of the account holder.

During life, exchange accounts make it easy to buy, sell, and convert cryptocurrency to cash. After death, however, access often slows significantly. Institutional custodians are rightly cautious about releasing assets and typically require formal legal documentation to establish authority. Even when an exchange account is listed on the trust’s Schedule of Assets, custodians commonly require:

- A certified death certificate

- Proof of the trustee’s identity

- Court-issued authority, such as letters testamentary or letters of administration

In practice, this often means probate court involvement may still be required, despite advance planning. In California, a limited remedy may be available through a Heggstad petition, which allows a probate court to treat an asset as trust property if it was clearly listed on the trust’s Schedule of Assets, even if it was never formally transferred. While a successful Heggstad petition may help avoid a full probate administration, it still requires probate court filings, legal fees, and several months to complete.

[Note: Some institutional platforms support trust-owned accounts, such as Coinbase Prime, though these are generally designed for business or institutional use rather than personal accounts.]

A Practical Example: How Wallets and Exchanges Are Treated

Consider John, a California resident with two types of crypto holdings.

Wallet-held assets:

John has $150,000 of Bitcoin stored on a Ledger Nano hardware wallet and $50,000 of Ethereum in a Coinbase Base Wallet. Both are listed on his revocable trust’s Schedule of Assets and supported by an assignment of digital assets. When John passes away, the trustee retrieves the recovery information and transfers the cryptocurrency as directed in the trust. No probate court involvement is required, and the process remains private.

Exchange-held assets:

John also keeps $75,000 of cryptocurrency in a personal Coinbase exchange account. Even though the account is listed in the trust, the institutional custodian requires a death certificate, proof of identity, and probate court-issued letters of authority before granting access. This portion of his estate is delayed and requires legal filings.

Wallets may allow for smooth administration within a revocable trust. Exchange accounts held with institutional custodians are more likely to involve probate court oversight, even with advance planning.

Facilitating Access for the Trustee

Facilitating Access for the Trustee

The most important element of cryptocurrency estate planning is coordination. Working with an attorney helps ensure that critical access information is organized, securely documented, and available to the trustee when needed.

Cryptocurrency can be owned by a revocable trust and administered without probate, but only if the trustee can actually access the assets. Control depends on passwords, private keys, recovery phrases, and platform-specific procedures. Because this information is highly sensitive, it should not be included directly in the trust document. Instead, attorneys often help prepare a separate memorandum of instructions that explains where assets are held and how the trustee gains access.

This approach reduces confusion, delays, and court involvement by giving the trustee both clear authority and a practical roadmap for administering cryptocurrency assets.

Key Takeaways

Cryptocurrency does not have to derail a well-designed estate plan. The key distinction lies in how assets are held. Wallet-based cryptocurrency, when properly documented and connected to a revocable trust, may pass to heirs privately and efficiently without probate. Exchange-held cryptocurrency, managed by institutional custodians, may still require probate court involvement before funds are released unless accounts are structured in advance through platforms that support trust ownership.

# # #

This discussion is for educational purposes only and is not legal advice. Always consult a qualified attorney in your jurisdiction for guidance on your specific situation.

Named #1 Firm from Financial Planning's "Best RIAs to Work For"

Meaningful work depends on judgement built over years, not quarters. At its core, our work is a long-term partnership. Clients turn to us as plans evolve, responsibilities grow, and new possibilities take shape, and we don’t take it lightly when we are their first call. The specifics may differ, but the steady thread of trust is what gives our work its depth.

Financial Planning ranked Bailard No. 1 on its Best RIAs to Work For list. It was our first year participating, and the result reflects something we've built over decades. A culture where talented people want to stay, grow, and do their best work. Long tenure has helped strengthen that foundation, creating continuity that clients and partners often value in enduring relationships.

With Bailard’s first-place ranking came an interview with CEO Sonya Mughal, CFA, in which Financial Planning explored the firm’s approach to building an environment that supports lasting careers. The profile highlighted policies such as paid sabbaticals, flexible time off, full medical premium coverage for employees, and a hybrid model designed to encourage teamwork and collaboration across offices.

Bailard’s independence plays a quiet but important role in shaping that environment too. As an independent, employee-owned firm, we are not driven by outside shareholders or short-term pressures. That structure gives our leaders the latitude to plan for the long term and act with purpose, investing in people, refining processes, and strengthening the resources that serve our clients.

Earlier this week, Bailard appeared for the eighth consecutive year on Pensions & Investments' Best Places to Work in Money Management list. Viewed together, the two honors offer a window into a culture that fosters continuity and engagement. Clients often appreciate that steadiness, particularly when needs can span financial and estate planning, investing, real estate, philanthropic goals, and values-driven priorities.

Mike Faust, CFA, President of Wealth Management, shared his perspective. “Clients come to us expecting clarity and continuity, not quick fixes. We can support those relationships more effectively when our team feels aligned with the firm’s purpose and grounded in their work. That’s the value of a strong culture, and it’s something we work hard to maintain.”

Our commitment remains steady. Serve clients with care, support colleagues with intention, and protect the independence that allows us to do both well. That's what we'll continue to build.

To view the full 2025 Best RIAs to Work For list, visit: https://www.financial-planning.com/list/best-rias-to-work-for-2025-ranking

About Bailard, Inc.

Founded in 1969, Bailard is an independent, values-driven wealth and asset management firm serving individuals, families, and institutions. Bailard has built a long‐term asset management track record across domestic and international equities, fixed income, and private real estate, along with in-house sustainable, responsible, and impact investing expertise. The firm helps clients align their financial goals with their values. Headquartered in the San Francisco Bay Area, Bailard had over $7.5 billion in assets under management as of 9/30/2025. Bailard is majority employee-owned, woman-led, a Certified B Corporation™, and a UN Principles of Responsible Investing signatory.

# # #

Bailard was considered for these awards without paying for inclusion, however, some programs have charged a registration fee: Pensions & Investments required $199 in 2023, 2024, and 2025, and the 2023 program included a $499 data-sharing fee from Best Companies Group. The awards do not evaluate the quality of services provided to clients and are not indicative of Bailard's future performance.

About Financial Planning's Best RIAs to Work For

To be considered for participation, eligible firms must be a for-profit or not-for-profit business or public agency, have a U.S. facility, have a minimum of 10 employees working in the U.S., and have been in business a minimum of 1 year. Evaluation consisted of a two-part process. First, an evaluation of workplace policies, practices, philosophy, systems, and demographics. Second, an employee survey measuring day-to-day experience. The combined scores determined the final ranking. 60 firms were ranked in 2025. For more information on Financial Planning’s Best RIAs to Work For program, visit https://www.financial-planning.com/list/best-rias-to-work-for-2025-ranking

About Pensions & Investments’ Best Places to Work in Money Management

Pensions & Investments, owned by Crain Communications Inc., is the 50-year-old global news source for money management and institutional investing. P&I released the 2025 ranking in December 2025. Participating firms must have at least 20 U.S.-based employees, $100 million of discretionary institutional assets under management or advisement, and a minimum of one year in business. In 2025, 103 firms were ranked, with 25 managers recognized in Bailard's category of 50 to 99 employees. For 2024, 2023, 2022, 2021, 2020, 2019, and 2018, there were 113, 123, 100, 76, 94, 76, and 69 firms ranked, respectively. For additional details regarding methodology, please visit http://www.pionline.com/BPTW2025.

Bailard Recognized as One of P&I’s Best Places to Work

Great workplaces often start with a simple idea. When you support your people, everything else gets better. That belief has guided Bailard for decades. It’s also why this year’s recognition from Pensions & Investments carries real meaning. Bailard has once again been named one of the Best Places to Work in Money Management. It’s our eighth consecutive year on the list (2018-2025).

Great workplaces often start with a simple idea. When you support your people, everything else gets better. That belief has guided Bailard for decades. It’s also why this year’s recognition from Pensions & Investments carries real meaning. Bailard has once again been named one of the Best Places to Work in Money Management. It’s our eighth consecutive year on the list (2018-2025).

Unlike many industry awards, this recognition is grounded in employee feedback, with 80% of the evaluation focused on the day-to-day employee experience. For an independent firm in an industry where consolidation continues to accelerate, that validation matters. Independence holds up only when the culture underneath it is strong.

This year, Bailard is ranked 3rd among firms with 50-99 employees. And while awards are always a chance to pause and reflect, an eight-year streak reflects something deeper: a culture shaped by the choices our people make every day and anchored in our firmly held values of accountability, compassion, courage, excellence, fairness, and independence.

“Culture is something you build choice by choice. It’s the small, everyday moments of supporting one another and doing what’s right for the people we serve. Seeing Bailard recognized for the eighth year in a row is a reflection of a team I’m immensely proud of. They show up with purpose, integrity, and compassion. They’re the reason this culture stays strong," remarked Sonya Mughal, CFA, Bailard’s Chief Executive Officer.

At its core, this recognition reinforces what we strive for. When people feel supported, trusted, and valued, it shapes how they show up for clients and colleagues. As we mark this milestone, our focus stays on what comes next: strengthening our culture, supporting our team, and protecting the independence that helps us serve the people and communities who rely on us.

For a full list of the 2025 honorees, visit http://www.pionline.com/BPTW2025.

###

About Bailard, Inc.

Founded in 1969, Bailard is an independent, values-driven wealth and asset management firm serving individuals, families, and institutions. Bailard has built a long‐term asset management track record across domestic and international equities, fixed income, and private real estate, along with in-house sustainable, responsible, and impact investing expertise. The firm helps clients align their financial goals with their values. Headquartered in the San Francisco Bay Area, Bailard had over $7.5 billion in assets under management as of 9/30/2025. Bailard is majority employee-owned, woman-led, a Certified B Corporation™, and a UN Principles of Responsible Investing signatory.

About Pensions & Investments’ Best Places to Work in Money Management

Pensions & Investments, owned by Crain Communications Inc., is the 50-year-old global news source for money management and institutional investing. P&I released the 2025 ranking in December 2025. Participating firms must have at least 20 U.S.-based employees, $100 million of discretionary institutional assets under management or advisement, and a minimum of one year in business. In 2025, 103 firms were ranked, with 25 managers recognized in Bailard's category of 50 to 99 employees. For 2024, 2023, 2022, 2021, 2020, 2019, and 2018, there were 113, 123, 100, 76, 94, 76, and 69 firms ranked, respectively. For additional details regarding methodology, please visit http://www.pionline.com/BPTW2025. Bailard was considered for this award without paying for inclusion, however, some programs have charged a registration fee: Pensions & Investments required $199 in 2023, 2024, and 2025, and the InvestmentNews’ 2024 program, and Pensions & Investments 2023 program included a $499 data-sharing fee from Best Companies Group. This award does not evaluate the quality of services provided to clients and is not indicative of Bailard's future performance.

Earning Our Place Among America’s Top RIA Firms

More than 50,000 firms were nominated. Thirty-three thousand interviews were conducted. Only 250 firms made the list.

Among them: Bailard.

We are proud to be recognized among Forbes’ America’s Top RIA Firms. The honor reflects a long tradition of teamwork, integrity, and care for our clients’ success.

What matters more than the recognition itself are the quiet moments that make it possible. It’s listening closely, planning carefully, and following through on every promise. That is where trust is built and where the work truly matters.

“Awards come and go, but what endures is how we treat our clients and colleagues,” said Sonya Mughal, CFA, Chief Executive Officer. “That’s the part I’m most proud of.”

This honor follows other 2025 distinctions, including Barron’s Top 100 RIA Firms and the San Francisco Business Times’ Top Bay Area Corporate Philanthropists list. Each reflects the same foundation of steady leadership and a shared commitment to doing what is right for those we serve.

# # #

About Bailard, Inc.:

Founded in 1969, Bailard is an independent, values-driven firm serving individuals, families, and institutions with comprehensive wealth management and investment strategies across public and private markets. Headquartered in the San Francisco Bay Area, the woman-led, majority employee-owned firm manages over $7 billion in assets as of September 30, 2025. A Certified B Corporation™ and signatory to the UN Principles for Responsible Investing, Bailard combines deep expertise with a long-standing commitment to putting clients first.

Past performance is no indication of future results. All investments have the risk of loss. These awards do not evaluate the quality of services provided to clients and are not indicative of Bailard’s future performance. There was no cost to enter any of the recognitions described herein.

About Forbes’ 2025 America’s Top RIA Firms: Bailard ranked 91 out of 250 firms in the 2025 Forbes Top RIA Firms and 90 out of 250 firms in the 2024, each announced in October. The ranking, developed by SHOOK Research, is based on qualitative interviews and quantitative data, weighing factors such as revenue trends, assets under management, compliance records, and industry experience. More information is available here: https://www.forbes.com/sites/rjshook/2025/10/01/methodology-americas-top-ria-firms-2025/

About Barron's Top 100 RIA Firms: Announced in September 2025, 2024, 2023, and 2021 by Barron’s. Bailard ranked 92 out of 100 on the 2025 list; 88 in 2024; 99 in 2023; and 98 in 2021. Advisors who wish to be ranked complete a 102-question survey; Barron’s then verifies that data and applies its rankings formula to generate a ranking. The formula features three major categories of calculations: assets, revenue, and quality of practice with multiple sub-calculations in each. https://www.barrons.com/advisor/report/top-financial-advisors/ria?

About San Francisco Business Times’ Top 100 Corporate Philanthropists: Annual award, given in July of each year, SFBT recognizes the top 100 for-profit companies and nonprofit healthcare institutions based on the year’s cash donations to charitable organizations across the Greater Bay Area, including the counties of Alameda, Contra Costa, Marin, Napa, San Francisco, San Mateo, Santa Clara, Solano, and Sonoma. Bailard ranked #65 in 2025, #71 in 2024, #79 in 2023; #82 in 2022; and #89 in 2021. There was no fee to enter. Please visit the SFBT for more information: https://www.bizjournals.com/sanfrancisco/subscriber-only/2025/08/01/the-top-corporate-philanthropists-in-the-bay-area.html

Economic Brief: Gold Rush

From gold to gigabytes, Jon Manchester, CFA, CFP® (Chief Strategist, Wealth Management) draws a line from California’s first gold rush to today’s race for artificial intelligence, exploring the optimism, risk, and reinvention that come with every new boom.

From its very beginning, California has attracted dreamers and schemers. In early February 1848, the Mexican-American War concluded, with Mexico ceding the territory of Alta California along with Texas and other parts of the west. In exchange, the U.S. paid $15 million and forgave $3.25 million of debt. Just over a week prior to that formative event in our nation’s history, an itinerant carpenter named James Marshall had discovered gold in Coloma, CA, as he endeavored to build a sawmill for the landowner, John Sutter. Word of Marshall’s find quickly spread—at least by mid-19th-century communication speeds—kicking off a mad scramble to this new land of opportunity. In The Age of Gold, author H.W. Brands characterized the Forty-Niners: “All sought wealth; nearly all sought adventure too. The news from California was the most exciting most of them had ever heard; the rush to California promised to be the event of their lifetime. Like little boys hurrying to greet the circus, to catch a glimpse of the mighty elephant, the emigrants of 1849 couldn’t bear to miss out – and in fact the phrase ‘to see the elephant’ became a cliché on the trail.”1

In a sense, that fear of missing out continues to typify those who travel long distances to try their luck in the Golden State. The elephant has evolved over time. The birth of the semiconductor industry gave way to the dot-com craze and then the rise of social media. Today, artificial intelligence (AI) is the glittery object which has a new generation of dreamers affixing “California or Bust” bumper stickers to their (probably electric) wagons. It is the singularly dominant theme in capital markets, with vast and seemingly ever-growing tentacles across disparate industries.

During the gold rush, demand for clipper ships exploded as prospectors sought to find quick passage to San Francisco Bay. Similarly, AI is creating enormous demand for an ecosystem of adjacent businesses providing infrastructure to support the buildout. Spending continues to spike on data centers and for the power required to run those facilities. Brookfield Asset Management estimates that ultimately around $7 trillion will be needed to finance the growth of AI.2 The so-called hyperscalers—Microsoft, Amazon, Alphabet, and Meta Platforms—are projected to outlay roughly $340 billion on capital expenditures this year, increasing to $400 billion in 2026.3 BlackRock, the world’s largest asset manager, formed an AI partnership last year to raise $100 billion with the intent to invest in data centers, joining a crowded field with big players including Apollo, Blackstone, and many others hoping to strike a vein of digital gold.

This “build it and they will come” approach takes a certain boldness, a disregard for potential failure. Brands described the same mindset as occurring during the gold rush: “Where life was a gamble and success a matter of stumbling on the right stretch of streambed, old standards of risk and reward didn’t apply. In the goldfields a person was expected to gamble, and to fail, and to gamble again and again, till success finally came – success likely followed by additional failure, and additional gambling – or energy ran out. Where failure was so common, it lost its stigma. No one in California counted the failures, only the rich strikes that rewarded the tenth or hundredth try.”4

It seems likely that failure will eventually follow for some amidst this tidal wave of AI expenditures: buy now, pay later? Hedge fund manager David Einhorn cautioned recently that “there’s a reasonable chance that a tremendous amount of capital destruction is going to come through this cycle.”5 Amazon founder Jeff Bezos acknowledged that AI spending resembles an “industrial bubble” in which “investors have a hard time in the middle of this excitement distinguishing between the good ideas and the bad ideas.”6 However, he also thinks “the benefits to society from AI are going to be gigantic.” Beyond the bubble worries, there is some uneasiness around the financing of all of these projects, with large tech companies increasingly relying on debt.

While we impatiently wait for AI to pan out, the markets continue to handsomely reward the companies in the fight. According to JPMorgan strategist Michael Cembalest: “AI related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending since ChatGPT launched in November 2022.”7 OpenAI, the owner of ChatGPT, is not publicly traded, but its private market valuation has soared to a reported $500 billion. Bloomberg notes that ChatGPT has about 700 million weekly users—making it one of the fastest-growing consumer products in history.8

What’s Old is New Again

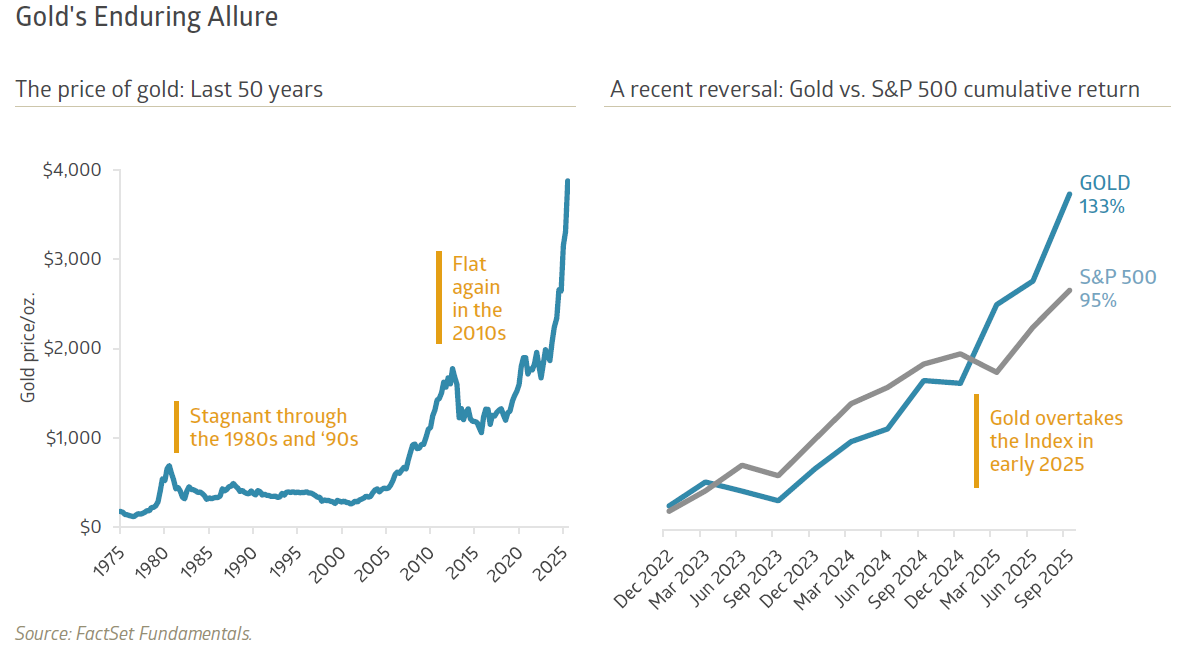

A funny thing happened on the way to coronate our new AI ruling class, though. Investors have once again developed a gold crush. In fact, the price of the alluring metal—which has captured imaginations for thousands of years—outpaced the stock market over the trailing three years, roughly since ChatGPT launched. The following page’s exhibit shows that gold soared 133% over that timeframe, ahead of the S&P 500 Index’s 95% total return. Not typically mistaken for a growth stock, it has been a goldilocks environment for the yellow metal. The Consumer Price Index (CPI) hit a peak of 9.0% year-over-year inflation in mid-2022, highest in over 40 years. This pushed some investors into gold as a store of value, or a way to avoid a loss of purchasing power. Inflation has normalized since, decelerating to 2.9% growth as of August 2025, but it has not reversed, which means prices continue to climb overall.

Meanwhile, rising concerns around unsustainable government debt levels have also weighed on the U.S. dollar, further exacerbated by a Federal Reserve monetary easing cycle which began a year ago. Lower short-term interest rates usually result in softening demand for the greenback. The Fed funds target rate of 4.25% remains well above what is considered a neutral rate, where monetary policy is neither expansionary nor contractionary. However, the Fed expects to keep easing, with the latest “dot plot” indicating a median estimate of 3.4% for year-end 2026. For gold bugs, the direction of monetary policy might be more important than the absolute level, providing further support to the futures price. With the inflation bogeyman still lingering offstage, any whiffs of accelerating inflation (due to tariffs, Fed easing, etc.) can extend the stay for gold.

Meanwhile, rising concerns around unsustainable government debt levels have also weighed on the U.S. dollar, further exacerbated by a Federal Reserve monetary easing cycle which began a year ago. Lower short-term interest rates usually result in softening demand for the greenback. The Fed funds target rate of 4.25% remains well above what is considered a neutral rate, where monetary policy is neither expansionary nor contractionary. However, the Fed expects to keep easing, with the latest “dot plot” indicating a median estimate of 3.4% for year-end 2026. For gold bugs, the direction of monetary policy might be more important than the absolute level, providing further support to the futures price. With the inflation bogeyman still lingering offstage, any whiffs of accelerating inflation (due to tariffs, Fed easing, etc.) can extend the stay for gold.

A further catalyst for gold’s relentless rise has been motivated buyers in the form of other central banks looking to diversify reserves. China’s central bank has been an aggressive buyer since 2023, according to Reuters, aiming to reduce its reliance on the U.S. dollar. Despite China’s buying spree, its gold position is currently smaller than five other countries, plus the International Monetary Fund, and accounts for just seven percent of China’s total reserves.9 Whether central banks will keep buying with gold near $4,000 per ounce is a viable question, but their concerted efforts to stockpile gold has clearly underpinned the bullion market.

Expense Card

The stock market’s brief April 2025 foray into bear market territory (>20% decline) now seems a distant memory. Tariffs remain a risk to profitability, but corporations have thus far largely managed to defray or offset the additional costs. Favorable tax policies outside of the trade realm clearly continue to help. The 2017 Tax Cuts and Jobs Act reduced the corporate tax rate from a high of 35% to a flat 21%, while this year’s One Big Beautiful Bill Act (OBBBA) permanently restored the ability for corporations to immediately expense domestic research and development (R&D) costs and returned to 100% deduction on qualifying business expenses, such as new computers, machinery, or other equipment.

According to Standard & Poor’s, the S&P 500 operating margin was 12.5% in the second quarter, its highest since 2021. Operating profits per share rose nearly 10% year-over-year in Q2 and growth is projected to accelerate to the 13% to 14% range over the final two quarters of 2025. Resilient corporate earnings growth and solid economic activity have taken recession odds sharply lower. The Bureau of Economic Analysis (BEA) recently revised up its Q2 Gross Domestic Product (GDP) growth estimate to 3.8% inflation-adjusted, a rebound from a small first quarter decline. Nonresidential fixed investment jumped 7.3%, buoyed by strong AI-related equipment spending. The U.S. consumer also did its part, propelled by high earners. Moody’s Analytics chief economist Mark Zandi calculated that the top ten percent of income earners now account for just over 49% of total expenditures – highest since 1989.10

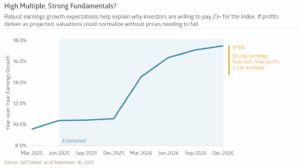

What remains is a fully priced U.S. large-cap equity market. The S&P 500 entered the final quarter of 2025 trading at nearly 23x estimated earnings over the next 12 months. Fed Chair Jerome Powell acknowledged as much in a late September speech: “…by many measures, for example, equity prices are fairly highly valued.” Investors seem willing to pay the price, however, emboldened by both the long-term promise of AI and rosy estimates for near-term earnings growth. S&P tabulates that S&P 500 earnings per share growth for 2026 is currently tracking at more than 17%. It could prove overly optimistic, but it does help explain why valuations are rich in an environment where the Fed is also cutting interest rates. Valuations remain much more restrained outside of the tech-heavy S&P 500 Index, with smaller company stocks and foreign equities relatively attractive.

Plenty of hurdles remain. We’re keeping a close eye on debt, whether at the federal, corporate, or individual levels. There will no doubt be those that misprice or underestimate risk and lose it all in a futile attempt to catch a glimpse of the mighty elephant. Buyer beware; yet remember that investing involves calculated risk.

Globalization, Reshoring, and the Cost of Stability

This quarter, Bailard’s SRII team looks at the forces reshaping global trade ,the costs that follow, and what these shifts might mean for investors.

Globalization and reshoring are pulling in different directions, yet both are shaping the future. One expanded U.S. GDP more than eightfold since 1950,1 lowered costs for consumers, and lifted millions worldwide out of poverty.2 The latter, however, left supply chains exposed to shocks from health crises, geopolitical tensions, and other global disruptions.

The contrast came into sharp focus during the pandemic. Lockdowns froze much of the global economy, exposing supply chain weakness while also delivering unexpected environmental benefits, from cleaner air and water to quieter oceans.3,4

The U.S. has since leaned into reshoring, encouraging companies to bring production back to domestic soil. Tariffs, subsidies, and industrial incentives are being used to reduce dependence on foreign suppliers and strengthen domestic industry. The goal is stronger supply chains and local jobs, even if it means higher costs.

Globalization’s gains and the costs that follow

Global trade delivered faster innovation and affordable goods while sharply reducing global poverty.5 Standardized shipping containers, introduced by Malcom McLean in 1956, slashed transport costs and accelerated the spread of global commerce.6

But those same connections created fragility. Millions of U.S. manufacturing jobs moved overseas, especially after China joined the World Trade Organization (WTO) in 2001.7 The pandemic highlighted the risk, exposing shortages of semiconductors, medical supplies, and basic goods.8 Geopolitical conflicts have since added strain, from sanctions on Russia to attacks near the Suez Canal.

Shipping, the backbone of global trade, carries environmental costs too. It produces about 3% of global carbon emissions each year, enough to rank as the world’s six-largest emitter if it were a country.9 The 2020 slowdown showed how quickly those impacts can change when trade contracts.

The vulnerabilities often surface as volatility, underscoring the need to diversify exposures across supply chains and regions.

Reshoring promises stability, with trade-offs

What began as a political slogan has become economic strategy. The U.S. is leaning on tariffs, subsidies, and industrial policies to bring production closer to home. For markets, this creates both winners and losers.

The 25% tariff on imported steel and aluminum10 is one example. While designed to reduce dependence on foreign suppliers, it raises costs for manufacturers and, ultimately, consumers. A modeled 25% auto tariff could increase car prices by about 13.5%, or about $6,400 on a new car,11 feeding directly into inflation.

The burden does not fall on the U.S. alone. Many lower-income countries depend on manufacturing jobs to reduce poverty. Reshoring could shift that balance, removing opportunities for millions in exchange for stability at home.

Reshoring does not end globalization, it changes its shape. The balance is moving toward security and away from pure cost efficiency. It makes global diversification and pricing power especially important.

Technology adds a wildcard

Advances in artificial intelligence (AI) may tilt this balance further. These tools can make global networks more adaptive, or reduce the appeal of offshoring by lowering labor costs. At the same time, AI’s productivity gains may ease inflationary pressures, though the benefits are likely to be concentrated in the firms sectors best able to deploy it. Large-cap technology and industrial automation companies, for example, may capture disproportionate value compared to smaller peers.

Market signals to watch

- Equities: Sectors with U.S. exposure and policy support—like semiconductors, clean energy, and logistics—may gain, while multinationals face higher costs.

- Fixed income: Inflation-linked bonds can offer protection if input costs rise, while credit markets may reward companies with strong balance sheets.

- Real assets and private markets: Infrastructure and logistics could stand to benefit, particularly as AI improves efficiency.

Inflation and wealth planning implications

Reshoring’s push for stronger domestic supply is not cost-free. Tariffs and subsidies raise costs, which companies often pass on to consumers. A study by the Federal Reserve Bank of San Francisco found that most of the wealth U.S. households built up early in the pandemic had vanished by late 2022 once inflation was considered.12 Real household net worth has grown only modestly since, despite strong nominal gains.13 Inflation continues to erode purchasing power.

These pressures are already shaping portfolio allocations. Many investors are favoring inflation-sensitive assets such as real estate, commodities, and inflation-linked bonds.14 They’re emphasizing sectors with durable pricing power to help portfolios hold value as higher input costs spread through the economy.

Long-term wealth planning must account for costs that rise faster than income, preserve purchasing power, and align exposures to higher trade and supply expenses. Philanthropic goals face similar choices: commit capital now while dollars stretch further, or preserve flexibility for future needs.

Preparation matters most

Globalization brought decades of growth and efficiency, but also fragility and uneven outcomes. Reshoring aims for stability, though at a higher price. Even small policy shifts in the world’s largest economy can ripple across workers, companies, and consumers worldwide.

The key is not to view globalization or reshoring as absolutes. Portfolios and plans should prepare for a mix of both. They should be positioned for opportunity where policy creates tailwinds, protected against higher costs, and built to weather shifts in markets and policy over generations.

Globalization’s path will keep shifting, sometimes gradually and sometimes abruptly, with technology shaping how costly or adaptive those shifts prove to be. Portfolios built for resilience can thrive whether globalization accelerates or reshoring takes hold.

1Amadeo, K. (2022). “An Annual Review of the U.S. Economy Since 1929.” The Balance.

2Our World in Data. (2021). “World population living in extreme poverty.”

3Arter, He, Holmes, Tull, et al. (2024). “Air Pollution Benefits from Reduced On-Road Activity Due to COVID-19 in the U.S.” PNAS Nexus 3(4).

4BBC News. (29 Apr 2020). “Wild Animals Enjoy Freedom of a Quieter World.”

5World Bank. (2015). “Poverty Headcount Ratio at $2.15 a Day (2017 PPP) (% of Population).” World Development Indicators.

6Blume Global. (2022). “The History and Evolution of the Global Supply Chain.”

7CGTN. (11 Dec 2024). “China’s promotion of economic globalization 23 years after accession to WTO.” CTGN.

8U.S. Intl Trade Commission. (2020). “Impact of the COVID-19 Pandemic on Freight Transportation Services and U.S. Merchandise Imports.”

9International Maritime Organization. (2014). “Third IMO GHG Study 2014.”

10Picchi, A. (10 Feb 2025). “Trump orders 25% tariffs on steel and aluminum.” CBS News.

11The Budget Lab at Yale. (2025). “The Fiscal, Economic, and Distributional Effects of 25% Auto Tariffs.” Yale University.

12Federal Reserve Bank of San Francisco. (Feb 2024). “The Rise and Fall of Pandemic Excess Wealth.” FRBSF Economic Letter.

13Advisor Perspectives. (12 Sept 2025). “Household Net Worth (Q2 2025).” Advisor Perspectives.

14AInvest. (Feb 2025). “Paradox of Wealth: High-Net-Worth Individuals Remain Financially Insecure in an Era of Inflation.”

Year-End Planning in a New Tax Landscape

Bailard’s financial planning and tax strategy teams help make sense of the One Big Beautiful Bill Act, so you can plan confidently for what lies ahead.*

As 2025 comes to a close…

Year-end planning takes on added importance with the passage of the One Big Beautiful Bill Act (OBBBA). This sweeping legislation brings both clarity and complexity to the tax landscape, introducing notable changes while leaving other familiar provisions intact. With some rules already in effect and others beginning in 2026, now is the time to take stock and ensure your financial plan remains well positioned.

Here’s a high-level overview of what’s changed—and what hasn’t—under the OBBBA, in three timely themes to consider before December 31:

- Accelerate charitable giving

- Leverage the expanded SALT deduction

- Consider Roth conversions

1) Accelerate charitable giving before the new AGI floor

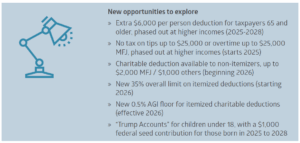

For many families, charitable giving is both a personal priority and a key planning tool. Beginning in 2026, charitable contributions for those who itemize deductions will only be deductible to the extent they exceed 0.5% of adjusted gross income (AGI).

While that may sound modest, it adds another hurdle for higher earners who regularly itemize. The good news: for 2025, gifts remain fully deductible up to current limits without the AGI floor. That makes this year a smart time to “lump” several years’ of donations into 2025. Doing so can help maximize deductions under today’s rules and reduce taxable income more effectively than spreading gifts across future years.

A donor advised fund (DAF) can make this easier. It allows you to make a larger, deductible contribution now while granting to charities gradually over time.

» Here’s how it works:

A high-income earner with $1,000,000 of AGI who typically donates $50,000 each year will, starting in 2026, only be able to deduct the portion exceeding $5,000 (0.5% of AGI). Their $50,000 annual gift would yield only a $45,000 deduction going forward.

By instead contributing three years’ worth of giving ($150,000) to a DAF in 2025, they can take the full deduction this year—without the AGI floor—and still direct $50,000 per year to their chosen causes. They’ve captured a larger deduction upfront, and likely lowered their 2025 tax bill in a meaningful way.

While itemizers face the new AGI floor starting in 2026, non-itemizers will gain a new opportunity to deduct up to $1,000 ($2,000 for married couples filing jointly, or MFJ) of charitable giving on cash contributions. Donations to a DAF or private foundation will not be eligible for this new deduction. It’s a small but welcome benefit for those who take the standard deduction.

2) Leverage the expanded state and local taxes (SALT) deduction

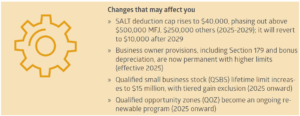

One of the more notable OBBBA provisions is the temporary expansion of the state and local tax deduction cap. For tax years 2025 through 2029, the cap increases from $10,000 to $40,000 for both single and joint filers who itemize.

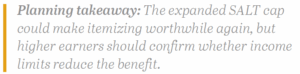

However, this benefit begins to phase out at $500,000 of AGI and fully reverts to the $10,000 limit once income reaches $600,000 or more. After 2029, the $10,000 cap returns unless further legislation is passed.

The higher SALT cap could make itemizing more attractive, especially for those living in high-tax states with sizable income and property tax bills. But it’s not just high earners who should take notice. Many households have defaulted to taking the standard deduction in recent years (currently $15,750 for single filers and $31,500 for MFJ), yet the higher SALT limit could make itemizing worthwhile again.

» Planning strategies if you’re near the phaseout:

If your income falls near the $500,000 to $600,000 phaseout range, there are ways to remain eligible for the full deduction this year and beyond:

- Defer income such as bonuses or business earnings into the following year

- Maximize pre-tax contributions to 401(k), 403(b), HSA, and similar employer retirement plans

- Use qualified charitable distributions (QCDs) if you’re subject to required minimum distributions (RMDs). QCDs allow you to donate up to $108,000 per year directly from an IRA to a qualified charity, satisfying all or part of your RMD while reducing AGI

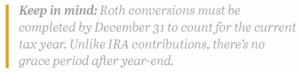

3) Consider Roth conversions wile rates remain low

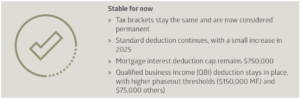

While the OBBBA makes today’s tax brackets “permanent,” that doesn’t mean they’ll stay that way. For now, rates remain historically low, offering an opportunity for proactive long-term tax planning.

For individuals with significant pre-tax retirement savings in traditional IRAs or 401(k)s, Roth conversions can be a powerful way to manage future taxes. RMDs can substantially increase taxable income once they begin, potentially pushing retirees into higher tax brackets, even under current rates.

The years between retirement and the start of RMDs or Social Security often present a valuable window. Many retirees fall into a lower tax bracket than during their working years, or after RMDs begin. That gap creates an opportunity to convert pre-tax retirement assets to Roth accounts, recognizing income at lower rates now to avoid higher rates later.

» Why Roth conversions can help:

- Qualified Roth withdrawals are tax-free in retirement

- Roth accounts aren’t subject to future RMDs, which allows longer tax-free growth

- Conversions may help offset potential tax increases after 2025, particularly for those expecting higher future income or estate tax exposure

If you’re nearing retirement or already retired but not yet taking Social Security or RMDs, consider whether a Roth conversion makes sense. Today’s low tax rates won’t last indefinitely, and acting now could make a lasting difference over time. Taking time to plan ahead now can make future withdrawals, and your overall tax picture, far more manageable.

Let’s make the most of 2025’s planning opportunities

The OBBBA has ushered in both new opportunities and new complexities in tax planning. Perhaps the clearest takeaway is this: AGI matters more than ever. From the new charitable giving floor to the expanded SALT deduction, many of the law’s most impactful provisions hinge directly on income thresholds.

That makes 2025 a pivotal year to manage income and deductions with care. Coordinating charitable giving, income timing, and retirement strategies can help keep your plan aligned with your goals while maintaining flexibility for what’s ahead.

Every household’s situation is unique, but preparation and foresight go a long way. A steady approach, informed by thoughtful planning, can help you feel confident that you’re well-positioned for what’s ahead.

Let’s talk.

OBBBA Snapshot: What’s changed and what’s new?

* Neither Bailard nor any employee of Bailard can give tax or legal advice. Please consult your tax or legal professional for such advice.

Bailard Recognized Among Barron’s Top 100 RIA Firms

Independent firm stands alongside the nation’s largest wealth managers.

SEPTEMBER 30, 2025 – Bailard, Inc. has been named to Barron’s list of the Top 100 RIA Firms for 2025, marking our fourth appearance in five years.

Unlike rankings based only on assets under management, Barron’s evaluates firms on a wide range of factors, from client retention and advisors’ experience to technology resources and charitable work.

For an independent firm like Bailard, it’s more than just another list. It shows that independence and values-driven service can stand alongside the biggest names in the industry without sacrificing the personal, values-driven approach that defines us.

“Being included in Barron’s Top 100 RIAs highlights Bailard’s ability to compete nationally while keeping our focus where it belongs, on doing right by our clients,” said Mike Faust, CFA, Bailard’s President of Wealth Management.

You can view the full Barron’s list here: https://www.barrons.com/advisor/report/top-financial-advisors/ria?

Bailard offers comprehensive wealth and asset management, with the resources of a national firm and the agility of an independent one. For us, independence isn’t just a structure. It’s the freedom to put our clients first, always.

# # #

About Bailard, Inc.:

Founded in 1969, Bailard is an independent, values-driven firm serving individuals, families, and institutions with comprehensive wealth management and investment strategies across public and private markets. Headquartered in the San Francisco Bay Area, the woman-led, majority employee-owned firm manages over $7 billion in assets as of September 30, 2025. A Certified B Corporation™ and signatory to the UN Principles for Responsible Investing, Bailard combines deep expertise with a long-standing commitment to putting clients first.

About the Barron's Top 100 RIA Firms: These achievements do not evaluate the quality of services provided to clients and are not indicative of Bailard’s future performance. There were no fees to enter. The Barron’s Top 100 RIA Firms was announced in September 2025, 2024, 2023, and 2021 by Barron’s. Bailard ranked 92 out of 100 on the 2025 list; 88 in 2024; 99 in 2023; and 98 in 2021. Advisors who wish to be ranked complete a 102-question survey; Barron’s then verifies that data and applies its rankings formula to generate a ranking. The formula features three major categories of calculations: assets, revenue, and quality of practice with multiple sub-calculations in each. Past performance is no indication of future results. All investments have the risk of loss.

Economic Brief: A Little Good News

Many years after hanging up his cleats in favor of a guitar, former linebacker Collins Obinna Chibueze still strikes a commanding presence under the bright lights. Standing 6'4", not counting the cowboy hat, the fast-rising singer better known as Shaboozey enjoyed a breakout year in 2024, earning him a “Best New Artist” nomination for last year’s Grammy Awards. The melodious Shaboozey moniker has its own football roots, dating back to when a high school coach slapped the name on his helmet as a phonetic reading of his surname. Shaboozey has been sounding it out ever since, blending country music with elements of hip hop, rock, and other influences. At their best, Shaboozey’s songs are playful and catchy while also introspective and questioning, built atop a bassline of human struggle.

It was undeniably a doozy of a year in 2025. Bloomberg columnist Clive Crook summarized it nicely: “Over the past 12 months, the U.S. has seen…every norm of economic policy—trade policy, fiscal policy, monetary policy—blithely tossed aside. At the same time, the U.S. economy stands at the bleeding edge of what might be as consequential an economic revolution as the transition from farming to manufacturing, or from manufacturing to services—except that the AI revolution could happen much faster.”1 Besides all that, 2025 was rather uneventful! The jump in economic uncertainty clearly did not dissuade the markets. It was, perhaps, another reminder that the stock market is not the economy. Investors heard sufficient good news to drive equity prices sharply higher for a third straight year. Critically, corporate profits did not disappoint: Standard & Poor’s (S&P) currently estimates that S&P 500 Index operating earnings advanced 13% per-share in 2025. That was the bottom line, but other tailwinds including lower interest rates, AI enthusiasm, and favorable tax policies also helped equities overcome numerous obstacles last year.

Amidst all the policy upheaval and a 43-day U.S. government shutdown—longest in history—investors learned to cope at times with a dearth of information from official government agencies. Beyond minding the information gaps, the August 2025 firing of Dr. Erika McEntarfer, commissioner of the Bureau of Labor Statistics (BLS), cast a shadow across the federal data landscape. Her dismissal immediately followed the Bureau’s July employment report in which the BLS sharply revised down its estimate of jobs added in May and June by a cumulative 258k. Whether or not the administration is correct that the “BLS is broken,” the optics of the decision did not go over well.2 In fact, handing McEntarfer a pink slip via social media hours after a disappointing jobs report may end up sowing more doubt. It prompted the Bloomberg Editorial Board to caution that “In so many words, this tells financial markets that official statistics are no longer to be trusted.”3 The ultimate consequences are unclear for the investment community as 2026 gets underway, but it may encourage decision-makers to rely more heavily on private sector data, where possible. Bloomberg’s Crook suggests that investors may be “flying blind” in an environment of heightened uncertainty and confusion over the state of the economy. For the financial markets, the adage “no news is good news” doesn’t typically apply.

Dot Com Club

A pivot to using more data from the private sector could easily start in Bentonville, Arkansas at Walmart’s global headquarters. The obvious reason: sheer scale. Walmart hauls in roughly 10% of all retail spending in this country, excluding automobiles.4 With around 2.1 million employees across 19 countries worldwide, Walmart amassed a staggering $681 billion of revenue in fiscal 2025—which in Gross Domestic Product (GDP) terms would put Walmart on par with countries such as Argentina and Sweden. Avoiding the company is a logistical challenge: 90% of the U.S. lives within 10 miles of a Walmart store.5 So when Walmart talks, the markets listen. In late November, Walmart reported its third quarter results, posting sales growth of ~6% and closer to a 7% advance for earnings per share (EPS). Perhaps more telling, outgoing CEO Doug McMillon said that U.S. customers and members are “still spending with upper and middle income households driving our growth.”6 McMillon acknowledged that lower income families have been under additional pressure, but also noted that like-for-like Q3 inflation was just 1.3% for Walmart US.

If Walmart as a tech company seems disorienting, consider that the world’s largest retailer just landed on the Nasdaq Stock Market. In December, after trading for over 50 years on the New York Stock Exchange, Walmart’s stock (WMT) migrated to the Nasdaq, joining companies such as Nvidia, Apple, Alphabet, and Microsoft. The exchange of choice for many tech companies, Nasdaq became the first U.S. stock market to trade online back in 1998. Walmart’s share price carries the sheen of a tech stock as well. After rising 23% last year, WMT finished 2025 trading at nearly 38x forward earnings, higher than many of its new Nasdaq peers.

Cold Brew

Although Walmart has managed to keep prices low via some alchemy of scale and technology, the overall inflation picture remains uncertain. Hot spots persist, including some high-profile areas. Electricity prices rose 6.9% year-over-year in November, per the BLS’s Consumer Price Index (CPI).9 Data centers are getting much of the blame, according to The Wall Street Journal, but hurricanes, wildfires, state renewable energy plans, and the replacement of aging or damaged grid equipment are all playing a role.10 California is feeling the pain more acutely than other states: power prices rose 35% inflation-adjusted over the 2019 to 2024 timeframe.

No area is getting more attention than health insurance costs. With the expiration of federal tax credits, the 24 million people that enrolled in coverage last year under the Affordable Care Act (ACA) will see their premiums increase significantly. San Francisco-based health policy organization KFF estimated that premium payments will more than double.11 For those covered under Medicare Part B, the 2026 standard monthly premium is going up nearly 10%. Employer-based health insurance is not immune, either. Mercer projects a total health benefit cost increase of 6.7% this year, pushing the average cost above $18,500 per employee.12 In 2025, Mercer’s annual survey found that the average cost of employer-sponsored health insurance rose 6%, driven in part by sharp growth in prescription drug spending with more companies including GLP-1 coverage.

Through all the noise, geopolitical tumult, and incertitude, Wall Street is uniformly optimistic. In fact, a year-end Bloomberg News survey found that all 21 strategists estimate the S&P 500 Index will post a fourth consecutive positive year in 2026.14 Wall Street analysts are estimating another strong year for corporate profits, as well, with S&P 500 earnings per share expected to increase by 14.8% on top of 2025’s already strong earnings growth.15 Again, the stock market is not the economy, but it does beg the question of whether everybody is gettin’ tipsy, to paraphrase Shaboozey. Another year of rising profits would certainly qualify as a little good news.

# # #

1 “Investors Are Flying Blind Into the ‘Golden Age,’ www.bloomberg.com, 12/26/2025.

2 “BLS Revisions Show President Trump Was Right – Again,” www.whitehouse.gov, 9/9/2025.

3 “Trusted Data Is a Vital Economic Asset,” www.bloomberg.com, 8/15/2025.

4 “How Walmart became a tech giant – and took over the world,” www.economist.com, 5/15/2025.

5 “Walmart, Inc.: Morgan Stanley Global Consumer & Retail Conference,” www.walmart.com, 12/2/2025.

6 “Walmart Inc. Q3 2026 Earnings Call,” www.walmart.com, 11/20/2025.

7 “Can Walmart Shed Its Discount Vibe?” www.nytimes.com, 6/23/2025.

8 “Heard on the Street: Should Walmart Really Be Trading Like a Tech Company?” www.wsj.com, 12/6/2025.

9 “Consumer Price Index for All Urban Consumers (CPI-U), Table 7,” www.bls.gov, 12/18/2025.

10 “Be Prepared to Keep Paying More for Electricity,” www.wsj.com, 12/29/2025.

11 “ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire,” www.kff.org, 9/30/2025.

12 “Mercer survey finds US employers and workers will face affordability crunch as health insurance cost is expected to exceed $18,500 per employee in 2026,” www.mercer.com, 11/18/2025.

13 “High Coffee Prices Are Changing How Consumers Take Their Daily Brew,” www.bloomberg.com, 12/16/2025.

14 “Every Wall Street Analyst Now Predicts a Stock Rally in 2026,” www.bloomberg.com, 12/29/2025.

15 FactSet, EPS One-Year Growth (%) estimated for year-end 2026, data retrieved 1/8/2026.

Specific investments described herein do not represent all investment decisions made by Bailard. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Read more