Fintech: The Engine Accelerating Financial Inclusion

Eric Greco, Equity Analyst, explains how the advancements of fintech companies are helping to provide the unbanked and underbanked with access to a broader range of often-crucial financial services.

While substantial progress has been made in the 15 years following the Great Financial Crisis—largely attributable to socioeconomic gains—significant barriers remain within the U.S. financial services industry. There is a need to address the millions of unbanked and underbanked Americans who lack adequate access to traditional banking services. The unbanked and underbanked populations are disproportionately low-income, minority, and immigrant households. They face a range of obstacles from high banking fees and minimum balance requirements, to limited branch access. These barriers largely keep them confined to an ecosystem outside the conventional financial system.

According to the Federal Deposit Insurance Corporation’s (FDIC’s) 2021 National Survey of Unbanked and Underbanked Households survey, 4.5% of U.S. households (or 5.9 million) were unbanked in 2021, meaning that no one in the household had a checking or savings account. This represents a decline from 5.4% or 7.1 million households who fell into the unbanked category in 2019, the lowest since the survey began in 2009. Additionally, an estimated 14.1% or 18.7 million households were underbanked, meaning that they had a bank account, but also used alternative financial services like money orders or payday loans. This represents a decline from 16.0% or 21.0 million households who fell into the underbanked category two years prior.1

The Rise of Nonbanks

In recent years, there has been a surge in the popularity of digital payments and mobile banking platforms (“nonbanks”) that offer peer-to-peer payment and banking services, such as PayPal, CashApp, (subsidiary of Block), Chime, and Venmo (subsidiary of PayPal). These platforms, which allow users to send and receive money electronically, have been a gamechanger for many individuals who have historically been underserved by traditional banking institutions.

Coinciding with the rise of smartphone ownership in the U.S.—over 85% of adults in 2021 reported smartphone ownership according to the Pew Research Center—digital payments and mobile banking utilization have skyrocketed. Mobile banking usage rose from 15.1% of households in 2017 to 43.5% in 2021.2 This provides a unique opportunity for mobile payment and banking platforms to service the very members of our society who lack basic access to traditional banking services. Look no further than the global remittances commonly used by immigrants to send or receive funds cross-border to family and friends. Visa recently published data showing 53% of consumers are now leveraging mobile, peer-to-peer apps to send funds globally, versus 34% utilizing a physical bank and the remaining 12% sending cash, checks, or money orders by mail.3

Addressing Financial Inclusivity

Financial inclusion, which refers to the process of bringing unbanked and underbanked populations into the traditional financial system, has come to the forefront as a critical issue. These populations face significant barriers to accessing financial services and products, which hampers the ability to save, invest, and build financial stability. In the United States, financial inclusivity has improved over the past decade as numerous fintech companies within the digital payment, neobank, and mobile banking vertical (both publicly traded and private companies) have emerged and addressed some of the inequities facing the unbanked and underbanked.

Financial inclusion, which refers to the process of bringing unbanked and underbanked populations into the traditional financial system, has come to the forefront as a critical issue. These populations face significant barriers to accessing financial services and products, which hampers the ability to save, invest, and build financial stability. In the United States, financial inclusivity has improved over the past decade as numerous fintech companies within the digital payment, neobank, and mobile banking vertical (both publicly traded and private companies) have emerged and addressed some of the inequities facing the unbanked and underbanked.

Fintechs, leveraging AI and predictive analysis tools, have not only made certain features more ubiquitous—such as free debit card issuance, early direct deposit, no account minimums, no monthly fees, and zero overdraft fees—but have also disrupted and triggered significant change across the digitally-enabled-user banking experience provided by traditional banks. Additionally, nonbanks often have less stringent requirements for opening an account than conventional banks. Chime, for example, does not require a credit check to open an account, making it more accessible to those with poor credit or no credit history.

Fintechs have not solved every issue of financial inclusion across the financial services industry, but they certainly have driven innovation, inclusivity, and disruption. These are key characteristics Bailard’s Technology Equity Research team looks for as it screens investment opportunities in the financial services industry.

In addition to offering low-cost financial services, nonbank providers also offer financial education and literacy for the unbanked and underbanked. Many platforms offer educational resources and tools that help users understand financial concepts and manage money more effectively. This is particularly useful for people who are new to financial services and may not have the knowledge or experience to make informed decisions. For example, CashApp offers a free financial education program called CashApp Boost, with tips on budgeting, saving, and investing. Similarly, Venmo provides resources and information on personal finance, such as how to build credit and manage debt. These enhancements can be particularly valuable for the unbanked and underbanked, who often lack access to financial education.

Fintech Product Development

We also note a trend in nonbanks driving financial inclusion through new products that are more tailored to the unbanked and underbanked. Many of these new offerings have provided an avenue towards escaping the predatory payday loan industry. It has not been uncommon for payday lenders and loan sharks to take advantage of financially-vulnerable individuals by offering cash-strapped customers exorbitantly high interest rate loans, ultimately making repayment burdensome.

Anecdotally, it is more common for digital payments platforms and mobile banks to offer loans and credit payment products—such as buy now, pay later—to consumers with limited access to broader banking services. While certain aspects of the terms behind these products have received scrutiny, these loans are typically more favorable and more accessible to low-income individuals. Offerings such as buy now, pay later, are generally structured to allow a consumer to make four interest-free payments every two weeks. Again, while fintechs may not be reinventing the wheel as it pertains to loans and credit offerings, they are forcing traditional banks to optimize their products in order to be more competitive.

CashApp’s free debit card (called Cash Card) offers “Boosts,” allowing users to earn discounts and rewards at select merchants. This rewards-like feature linked to a user’s debit card is still relatively nascent. The benefit of helping users save money on everyday purchases can be particularly valuable for low-income households. As another example, Venmo offers Venmo Credit, which is a line of credit that can be used to make purchases. With often limited access to credit, the underbanked segment is likely to find this especially useful. Usage of Venmo Credit allows the underbanked an avenue to make purchases and build credit history, both of which can greatly aid future financial stability.

All that said, it’s imperative we highlight the importance of ensuring accounts are FDIC-insured in light of the recent volatility in the banking sector surrounding bank deposits. Users of mobile payment and/or banking platforms should be aware that not all banking institutions are insured by the FDIC. Numerous fintechs catering to digital payments and mobile banking are registered banks or leverage partner banks for FDIC insurance. However, this is not always the case and may often depend on the type of product and services being utilized. Nonbank payment companies are typically subject to less rigorous regulatory oversite than traditional banks. Users of nonbanks may be subject to contractual rules and procedures that are not supported by federal statutory or regulatory standards, resulting in fewer of the protections afforded to bank customers.

In Summary

Nonbanks have emerged as key players in promoting financial inclusion for the unbanked and underbanked in the U.S. Through digital payment services, savings accounts, loans, and educational resources, nonbanks have made it easier for individuals to access more traditional financial services.

Make no mistake about it, many of the consumer-friendly banking and financial services brought to market by fintechs have forced traditional financial institutions to reevaluate product offerings and adopt more consumer-friendly policies, while also modernizing user experiences to mitigate attrition across business lines. In our view, this has the potential to continue improving financial stability and increase economic opportunities for millions of Americans who are currently excluded, in some form, from traditional banking services. As such, emerging fintechs and nonbanks are likely to play an increasingly important role in promoting financial inclusion with a strong positive societal benefit for years to come.

1 https://www.fdic.gov/analysis/household-survey/2021execsum.pdf

ESG-related Regulatory Requirements

While ESG has become mainstream, it has become a much more polarized political issue in the United States. Nevertheless, regulators at home and abroad are working to improve ESG disclosures and build a better framework for ESG investors.

Bailard’s View on the Economy: Everybody Act Normal

In this quarter’s closing brief Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) takes a look at the difficulties of defining, and returning to, normal.

In the 1920 United States presidential election, 55-year-old Ohio Republican Senator Warren G. Harding handily defeated Ohio’s Democratic Governor James Cox, winning 37 states and amassing 60.4% of the popular vote. Two-term incumbent Woodrow Wilson—eligible to run again—had been brushed aside by the Democratic party after suffering a severe stroke and amidst tepid enthusiasm for his foreign policies in the wake of World War I. The election was notable for many reasons. It closely followed the passage of the Nineteenth Amendment to the U.S. Constitution, giving women the right to vote in all 48 states (at the time). That greatly helped in boosting the total number of voters by over eight million, or nearly 45%, compared to the 1916 election. The 1920 ballot also featured two future presidents as vice presidential candidates in Republican Calvin Coolidge and Democrat Franklin D. Roosevelt.

When voters went to the polls in November 1920, the U.S. was mired in a recession marked by sharp deflation, an overcorrection from high wartime inflation. The nascent Federal Reserve, founded seven years prior to stabilize the banking system, had hiked its lending rate as high as 7% in mid-1920 in an attempt to temper what had been rising prices. Nobel-prize winning economist Milton Friedman and colleague Anna Schwartz later argued in a landmark 1963 book titled A Monetary History of the United States that the Fed miscalculated the lag times associated with monetary policy changes, resulting in the central bank still raising rates during the early stages of the recession.1 Unemployment jumped higher, and the Dow Jones Industrial Average sank nearly 30% over the twelve months leading up to the election. Tensions ran high seemingly everywhere: labor strife, race riots, plus a bombing on Wall Street that killed 40 and injured hundreds.

Meanwhile, the world was still reeling from the Great Influenza pandemic. An estimated 500 million people worldwide were infected by the virus in the 1918 to 1920 timeframe, or roughly one-third of the world’s population.2 A staggering 50 million or more died, including approximately 675,000 in the United States. In comparison, the World Health Organization (WHO) currently estimates 6.67 million have died globally from COVID-19.3 Needless to say, it was a challenging time.

In retrospect, then, it doesn’t seem particularly surprising that Harding’s main campaign slogan was “return to normalcy.” It had a simple, timeless appeal. Malleable and open to interpretation, normalcy is somewhat in the eye of the beholder. A main facet of Harding’s pitch was to put America first, a phrase which ironically Wilson had used to justify staying out of World War I in its initial years. In a May 1920 speech in Boston, Harding suggested America’s present need was “not submergence in internationality, but sustainment in triumphant nationality.”4 For a nation weary from battles both home and abroad, the message resonated sufficiently to carry Harding and Coolidge to the White House.

Back to the Future

A century later, with the COVID-19 pandemic hopefully on the wane and the Fed again in inflation-battling mode, there appears to be some clear parallels to that time. One interesting link from a societal standpoint—although certainly not unique to either time period—is the collective yearning to see things get back to some version of normal (however defined). We’ve been through this before, whether it was the aftermath of 9/11 or the credit crisis. In each instance, what follows seems to be a race to declare a “new normal” has arrived. There is some truth to this, of course. The COVID-19 pandemic has likely indelibly altered the way we work, for instance. Other behaviors, such as returning to crowded arenas or airports, quickly revert.

Each crisis alters the landscape in its own way. Roughly three years past the onset of the COVID-19 pandemic, the global economy is still trying to find its footing. In a November 2022 outlook piece, the Organization for Economic Co-Operation and Development (OECD) projected global real GDP (gross domestic product) growth of just 2.2% in 2023. Per the OECD: “Tighter monetary policy and higher real interest rates, elevated energy prices, weak household income growth, and declining confidence are all expected to take a toll on growth, especially in 2023.”5 For the U.S., they estimate scant 0.5% growth this year, followed by still negligible 1.0% growth in 2024.

Any economic growth in the U.S. for 2023 might be viewed as a minor victory. The consensus view seems to be coalescing around a shallow recession at some point this year. The Bloomberg Economics team foresees a 0.9% GDP contraction in the second half of 2023, driven by an investment downturn as companies reduce inventories amidst slower consumer spending.6 They also expect a decline in residential investment due to higher interest rates, and note that U.S. home prices would need to fall around 15% to restore the housing market to equilibrium. This is not 2008, Bloomberg assures us: a structural undersupply of houses and higher credit quality of mortgage borrowers limit the downside and the spillover risks to the wider economy. After 124 consecutive months of growth for the Case-Shiller U.S. National Home Price Index, October 2022 marked four straight months of declines. Before we hit the panic button, the Index was still up 9.2% on a year-over-year basis.

The big question remains whether the Fed’s rate hiking campaign will tip the U.S. economy into recession, as it did in 1920. Faced with inflation not seen since the early 1980s, the Fed was forced last year to rapidly raise the Fed Funds target rate from 0.25% all the way to 4.5%. In December, the Fed’s projections indicated a peak rate in the 5% to 5.25% range. That is well above the 2.5% level that the Fed considers neutral—meaning neither accommodative or restrictive—when inflation is at 2%. With the Consumer Price Index (CPI) running at +7.1% year-over-year in November, though, the Fed has to play bad cop until prices cool further. Attempting to define what is “normal” for the Fed Funds rate is highly dependent on the time frame. Over the last 50 years, the average Fed Funds rate has been approximately 4.9%. Shortening the time horizon to the last 20 years, however, the average rate was just 1.4%. Tricky word, normal.

The big question remains whether the Fed’s rate hiking campaign will tip the U.S. economy into recession, as it did in 1920. Faced with inflation not seen since the early 1980s, the Fed was forced last year to rapidly raise the Fed Funds target rate from 0.25% all the way to 4.5%. In December, the Fed’s projections indicated a peak rate in the 5% to 5.25% range. That is well above the 2.5% level that the Fed considers neutral—meaning neither accommodative or restrictive—when inflation is at 2%. With the Consumer Price Index (CPI) running at +7.1% year-over-year in November, though, the Fed has to play bad cop until prices cool further. Attempting to define what is “normal” for the Fed Funds rate is highly dependent on the time frame. Over the last 50 years, the average Fed Funds rate has been approximately 4.9%. Shortening the time horizon to the last 20 years, however, the average rate was just 1.4%. Tricky word, normal.

Too Much of a Good Thing?

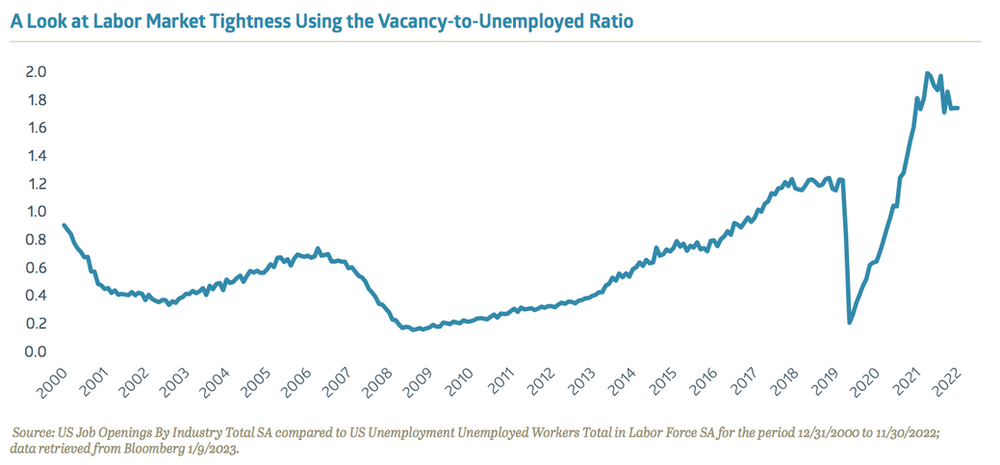

nKeeping inflation in check remains the Fed’s primary focus, but its other mandate is to maximize sustainable employment. With the unemployment rate at just 3.5% nationally as of December, matching a five-decade low, you’d have to say that box is checked. However, Fed Chair Powell has been clear that the labor market is too tight. Job openings have slowed, but remain elevated at roughly 10.5 million as of November. The Fed’s favored gauge for labor market tightness—shown below—is the vacancy-to-unemployed ratio, which was 1.74 versus 1.15 at the end of 2019.7 This excess demand for workers puts upward pressure on wages, and makes the Fed’s inflation-fighting job more difficult.

The December jobs report provided some good news. Average hourly earnings rose 4.6% year-over-year, a deceleration from +4.8% in November and a continuation of a slowing trend that saw this metric hit a 2022 high point at +5.6% last March. If sustained, this is the formula that could potentially deliver a “soft landing” for the economy: unemployment remains low, but wage growth and inflation moderate. As former Fed governor Randall Kroszner said: “It’s not that the Fed wants fewer jobs. What they want is lower wage growth more because they’re worried about persistent inflation.”8

If employment stays strong and housing prices remain resilient, it’s hard to imagine a near-term recession. Layoffs have picked up, but at a reasonable clip. According to the data firm Challenger, U.S. companies announced 320,173 layoffs over the first eleven months of 2022, a six percent increase. Just over 25% of those occurred in the tech sector where Amazon, Facebook, and others are attempting to right-size their operations. Despite the pressure on tech companies, California’s unemployment rate declined 1.7 points over the twelve months ending with November 2022 to 4.1%. The lowest state unemployment rates were in Utah (2.2%), Minnesota (2.3%), and North Dakota (2.3%).

Transitioning away from ultra-low interest rates never promised to be an easy road. This process of normalization took some prisoners in 2022. The tech-heavy Nasdaq Composite Index sank 33% on a price-only basis as investors repriced high growth, high valuation stocks. Some of the biggest winners in 2021 dropped to the bottom of the 2022 scoreboard, including California-based chipmaker Nvidia, which soared 125% two years ago before a 50% plunge in 2022. The lone S&P 500 Index sector that posted a positive price-only return in 2022 was Energy. The closing price of West Texas Intermediate (WTI) crude oil jumped as high as $123/barrel last March, up 64% from its year-end 2021 level, before fading to $80/barrel when 2022 came to a close. Nevertheless, the S&P 500 Energy sector returned 59% price-only last year, helped by attractive dividends and low valuations. It was an abnormal year, as usual.

A couple years after that 1920 presidential election, poet Robert Frost composed “Stopping by Woods on a Snowy Evening” at his home in Vermont. It contained the famous concluding (and repeated) line “And miles to go before I sleep.” That is a pretty apt saying for the markets in 2023. Many challenges remain for corporate America: higher interest rates, higher input costs, and likely lower margins. The easy money era is over.

1 “In the Shadow of the Slump: The Depression of 1920-1921,” www.econreview.berkeley.edu, 3/18/2021

2 “History of the 1918 Flu Pandemic,” www.cdc.gov

3 “WHO Coronavirus (COVID-19) Dashboard,” www.covid19.who.int, 1/4/2023

4 “Warren G. Harding’s pledge to ‘return to normalcy’,” www.britannica.com

5 “OECD Economic Outlook, Volume 2022 Issue 2,” www.oecd-ilibrary.org, 11/22/2022

6 “US Growth Outlook 2023,” Bloomberg Intelligence, 12/29/2022

7 “US REACT: Quitters Make It Hard for Fed to Cool Wages,” www.bloomberg.com, 1/4/2023

8 “Fed Gets ‘Goldilocks’ Report: Slower Wage Growth, Solid Hiring,” www.bloomberg.com, 1/6/2023

“One word Benjamin: Semiconductors”

A well-rounded look at the state of the semiconductor industry as a component of technology investing from Chris Moshy, Senior Vice President of Equity Research.

September 30, 2022

If the classic 1967 film “The Graduate” was re-made today, the sage advice Dustin Hoffman’s character Benjamin Braddock received from a family friend would be undoubtedly updated to: “I’ve got one word for you, Benjamin: semiconductors.”

While plastics1 are no doubt ubiquitous in today’s economy, the world could not function without semiconductors: small silicon-etched2 integrated circuits found in everything from laptops and kitchen appliances to smartphones and self-driving vehicles. Undeniably, and for better or worse, innovation, product cycles, and device proliferation of all kinds are inexorably driving semiconductors deeper into the infrastructure of our daily life.

Think about the feature set of today’s vehicles—lane departure warning, blind spot detection, GPS mapping, adaptive cruise control, and performance-tuned engines—all semiconductor enabled. Electric vehicles are really supercharged computers with microchip-laden battery systems and software on wheels. The smartphone you may be using to read this operates primarily on semiconductors with its bright OLED3 foldable screen, powerful digital camera, a super speedy and cool-running CPU, plenty of fast-swapping memory to manage and store apps, and is web-connected via a cell signal using a 5G millimeter-wave chipset. Yikes! Where’s my rotary phone?

The comprehensive nature of the semiconductor industry underscores why we strongly believe the group is an integral component of a technology investment strategy. It is also an industry defined by rapid innovation, brutal competition, significant capital investments, and, as the current environment reminds us, one subject to substantial cyclicality.

By many measures the current business cycle for semiconductors has peaked and the retrenchment in stock prices has been painful. Over the past 12 months ending September 2022, the Philadelphia Semiconductor Index (SOX), a broad industry performance measure, is down 29.3% versus the S&P 500 Index, down 17.7%. On a ten-year basis, however, the SOX Index gained 528% vs the S&P500 at 153%; and a 20-year comparison shows the SOX Index up 682% vs S&P500 less than half that at 304%.4

The semiconductor industry is still expected to grow mid-single digits this year, and current estimates for 2023 reflect low-single digit declines in global semiconductor revenues. This is down from the 26% growth enjoyed in 2021.5 After several years of above-trend demand, particularly in consumer durables during the pandemic, many end markets are now faced with excess customer inventories and buyers retracing their steps. PCs and smartphones sales have contracted meaningfully in 2022, as have other consumer products such as appliances, leisure equipment, and entertainment hardware. Even in areas showing good demand, think of the auto sector, component order rates are slowing as inventories fill up and the outlook for the global economy darkens.

Whether this downturn in the semiconductor sector will be short and shallow or more protracted is actively analyzed in the markets. Our current view is it will be early- to mid-2023 before visibility improves and industry recovery begins, but stock prices often anticipate a business upturn by a quarter or more. The depth and breadth of an economic recession of course will impact that forecast.

There are other issues at work that impact both the current business cycle and the long-term supply challenges. Some may be surprised to learn that many of the most recognizable consumer products in the world are dependent on very few regional suppliers. This includes the most advanced semiconductors and sophisticated electronic components that are at the core of flagship products. As Apple Inc. states in its annual 10k filing, “Substantially all the Company’s hardware products are manufactured by outsourcing partners that are located primarily in Asia… A significant concentration of this manufacturing is currently performed by a small number of outsourcing partners often in single locations.” This concentrated supplier risk is not limited to Apple; many leading semiconductor and consumer device companies6 rely on the same narrow supplier channels for product manufacturing and assembly.

Recent supply chain disruptions, capricious government closures of regional manufacturing hubs, and China’s increasingly menacing posture towards Taiwan has brought the issue front and center for business executives and members of Congress alike. Interestingly, Eastern Europe’s unrest and Western Europe’s unpredictable energy supply and expensive workforce makes the U.S. the location of choice for future semiconductor capacity additions. Of course, the effort will greatly benefit from the CHIPS Act, a bill signed into law this past summer that provides grants and tax breaks to companies building semiconductor manufacturing plants in the U.S. The CHIPS Act helps a select set of companies finance capacity expansions to build semiconductor facilities for their own operations or to provide outsourced fabrication services for others.

The CHIPS Act does limit companies from using funds to pay dividends or for share repurchases. Yet, it also improves the flexibility for companies to make capacity investments while maintaining capital return programs for shareholders—even during an industry downturn. In today’s environment, semiconductor companies are aware of the industry’s cyclicality and have learned to budget capacity growth based on demand forecasts and cost targets rather than the availability of capital. Understandably, with so much new investment capital and incentives entering the industry in coming years, it will be important to monitor the impact on industry supply discipline including the growth of outsourced capacity in the U.S.

Lastly, the rise of export restrictions on key technologies to China is a growing concern for companies and investors. Chinese firms are among the largest buyers of U.S. technology, including semiconductors, components, and fabrication equipment. Currently, most U.S. technology sales to China are considered “lagging” or “legacy” products and equipment, but still amount to 20%+ of sales for many companies, while sales of leading-edge products that tend to be restricted are in the low single digits. Without better policies around technology transfer, continued export restrictions will limit the long-run potential of the region’s growth for U.S. companies.

This year has not been easy for technology investors and, once again, the semiconductor industry has proven its cyclicality. While we expect some pressure on business fundamentals through year-end, we are on the offensive for investments, including in the semiconductor ecosystem. It’s an industry in which the most innovative and competitive companies are generally rewarded by successively higher revenues, profits, and stock prices with each business cycle. The industry is well-capitalized, and the CHIPS Act ensures continued growth investments in its manufacturing base. Market leaders in the technology industry can shift surprisingly quickly from cycle to cycle so investing in the sector requires attention (and patience), but the fascinating and rewarding opportunities justify the effort.

1 The original piece of advice to Benjamin Braddock!

2 Germanium substrate is also common, and the latest generation chip designs incorporate gallium arsenide substrates

3 Organic light emitting diode

4 Philadelphia Semiconductor Index; SPDR 500 ETF; Bloomberg LP

5 Gartner Forecasts Worldwide Semiconductor Revenue Growth

6 Qualcomm, Inc., AMD Corp., Nvidia Corp., Microsoft, Inc. and many other operate under similar “fab-less” manufacturing models

A Special Letter from Bailard’s CEO, Sonya Mughal, CFA

Humbled and honored. These are the words I keep coming back to as I have accepted the post of Chief Executive Officer at Bailard. Peter Hill, CEO from 2008 through this spring, has dedicated 36 years of his life (and counting) to Bailard and its stakeholders. The pursuit of excellence embodies his career, particularly the pursuit of excellence without cutting corners. Throughout his leadership, Peter devoted his time to take us to the next level through his steady guidance. All with a great deal of patience, and always doing the right thing.

Early achievements in Peter’s tenure include building out Bailard’s institutional client base with our asset allocation consulting business, something that was quite novel and not pursued by many in the industry. Soon after, Peter transitioned into the role of Chief Investment Officer where he steadily grew the team, always trying to hire the best.

A passionate believer in active management, he built a tremendous investment management team, one that could serve clients across many different asset areas. And when Tom Bailard began to think about his retirement and succession, Peter was appointed as the Firm’s first non-Founder CEO in 2008. This turned out to be no easy task. A few short months in, we faced the worst financial crisis that since the Great Depression, putting our clients and the Firm under tremendous stress. Having a steady hand and guiding the company through that crisis was no small feat.

As the waters were beginning to calm after Peter started his role as CEO, we also began the search for liquidity for the company’s largest shareholder. Maintaining our independence has been near and dear to us as a Firm, and Peter faced this question with a fresh perspective. And after a dalliance with an investment banker, and other forms of capital, he reaffirmed the belief that the best way to honor Tom and to continue to build Bailard was to remain independent. And so started the out-of-the-box thinking, something that is innately “Peter”! Having solved one of the most important issues for us as a Firm and managed through one of the biggest financial crises in recent memory, Peter turned his attention to the future.

Inspired by his nephew who won a Gold medal at the 2012 Olympic Games in London, Peter came back enthused. “Let’s have our own ‘Olympic’ plan.” The beauty of it? You can’t change the date! You set a goal and you work towards it, day by day, one foot in front of the other. Because you’re taking the entire company on this journey, you measure your progress and you regularly report your results, good or bad. In the words of our CIO Eric Leve, “Peter’s greatest gift is his vision. He takes an inspired, long view of the landscape and strives for big goals.” The Olympic plan was this vision in action.

An “Olympic”-sized plan meant Olympic-sized goals. And thus we endeavored to double assets under management and revenues within a four-year time frame. It was courageous, and it required everyone to pull on the same rope, to believe in the same dream. “Are you on the bus or not?” he asked at an all-company meeting once. And he meant it.

From guiding Bailard through the 2008 financial crisis and fostering our independence to setting ambitious goals and spearheading the launch of the Bailard Foundation, Peter has consistently been a steady, determined leader. Our EVP of Real Estate, Preston Sargent, notes how Peter was able to lead Bailard through so many years of change, saying his “thoughtful, calm, and reassuring leadership style was ideal to guide the Firm.”

Among these accomplishments is one that is less defined, but still impactful. Shifting a Firm’s focus without changing its core culture is not an easy task, but one Peter managed without fail. Our Vice Chairman, Burnie Sparks, summarizes it well, noting Peter was, “instrumental in some of the Firm’s most dynamic growth in its history. That growth was no accident. It was led and nurtured.” To me, that has been one of his greatest achievements.

Bailard was built on tremendous openness and transparency. Our stated values are accountability, courage, compassion, fairness, excellence and independence, each one as important as the next. Never losing sight of these values but with an eye to making the company even better for our clients, our employees, and our shareholders was Peter’s goal. One that he has very humbly achieved, taking little credit along the way, but making the Firm stronger and more competitive today than when he took over.

The Origins of Socially Responsible and Sustainable Investing

One of the fastest growing areas in investing today is socially responsible investing (SRI) and environmental, social, and governance (ESG) investing. The growth in SRI and ESG has not just been driven by the heightened desire of individual investors to align social and environmental values with portfolios, but also by the realization that ESG metrics can be a valuable gauge of risk and can drive investment performance. It may be surprising to some that SRI has been around for decades, and ESG arrived in the mid-2000s. Inside this research paper published in The Journal of Impact and ESG Investing, “From SRI to ESG: The Origins of Socially Responsible and Sustainable Investing,” Bailard’s own Blaine Townsend, CIMC®, CIMA®, explores the history of SRI and ESG investing.

Inside, you’ll learn:

- How the history of SRI and ESG investing has roots not only faith-based investing but also in the civil rights, antiwar, and environmental movements of the 1960s and 1970s;

- How investment risks posed by climate change and poor corporate governance were a large catalyst to ESG investing;

- How ESG data is now much more widely available than even a decade ago, making ESG investing much more viable; and

- The impact of SRI and ESG on investment returns.

The Strength of our Values in Unprecedented Times

As we turn from one quarter to the next, it at once feels like time is passing both quickly and slowly. Thinking back six weeks, we were dining at restaurants, throwing birthday parties, and strolling through grocery store aisles. That already feels like ages ago, and that kind of normalcy now itself seems novel. We at Bailard are familiar with dynamic conditions from frequently-changing market signals to slower-moving economic indicators. But this is different. Social and fiscal policies are evolving daily around a health crisis that goes beyond the markets and the economy to our homes and loved ones.

Just six months ago, we wrote in the 9:05 about our firm-wide values: accountability, compassion, courage, excellence, fairness, and independence. These values have always been core to who we are and today, in these testing times, they are more important than ever.

Bailard, with our clients, has overcome numerous economic shocks over the 50 years since our founding. And while 2020 has brought us extraordinary, previously-unthinkable times, we are confident we will overcome this too. Within the pages of this quarter’s 9:05, you’ll find the same relevant, measured perspective on the markets and economy that you have come to expect from your Bailard team. We continue to take a long-term perspective on the market, yet are mindful of short-term opportunities to minimize losses or even uncover possible gains. And, as always, we work tirelessly to ensure the needs of our clients are first and foremost.

This unprecedented health crisis presents a unique challenge for we, as humans, thrive on social connection. While the pandemic has in some cases brought generations of families together under one roof, in other cases we are separated and far away. And we cannot see our friends (or at least, not in-person). With that in mind, we thought to share a little of our experience, and you’ll find the back cover of this newsletter offers a peek into our lives as we shelter-in-place.

It shouldn’t have come as a surprise, but we are so pleased to witness the strength of our team during this time. We hope you share in the pride that we feel as our colleagues exhibit not only the excellence you might expect but exceptional compassion for our clients and our communities. We thank you for your partnership and, more importantly, wish safety and good health for you and your families. If you have any questions or concerns and want to discuss more, please reach out to us.

Peter M. Hill

Chairman and Chief Executive Officer

Executive Vice President

Chief Operating Officer, Chief Risk Officer

Our Values in the Midst of the Pandemic

Having accepted the post of CEO in the depths of a pandemic, I was optimistic that once we got past the worst, the next couple of years would at least be on a somewhat more upward trajectory. That was wishful thinking, in hindsight. The last 36 months have been challenging for all investment professionals. From dealing with the pandemic and inflation worries that have persisted longer than most thought, to an aggressive and very hawkish Federal Reserve Bank that raised interest rates at the fastest clip than most of us have seen in our careers, not to mention major market sell-offs in the equity and fixed income markets, and finally to classic “runs on banks” that bring back memories of the 1930s, this has been a challenging time. And it’s important to acknowledge that.

Several years ago, in connection with Bailard’s 50th anniversary, we set about codifying the values that are foundational to our company. Several were not unexpected—like Excellence, Fairness, and Accountability—but two stood out as different and important. I speak often to my colleagues about Compassion. It plays an instrumental role in how we treat each other and how we care for our clients, partners, and community. But, as the world continues to raise new challenges, the value of Courage keeps bobbing up to the surface.

Courage takes many forms in work and in life. Sometimes, Courage means holding steadfast to a sound plan in the face of adversity. On the other hand, it speaks to the willingness to challenge one’s thinking and take calculated risks when warranted. And, at its core, Courage is the backbone to stand up and do what is right, even when it is hard.

Crucially, I find that courage begets courage. When we push outside our comfort zones, we grow professionally and personally. It then compounds, building trust and serving as inspiration and creating a community where we motivate each other in the pursuit of greatness. I am inspired every day by this team. I see how their courage creates a workplace that is innovative and thriving, but also brave and caring.

With the words of Jim Collins in mind, it is impossible to foretell exactly what lies ahead and we, instead, rely on each other. For over five decades, individuals, families, and institutions alike have entrusted Bailard. We have weathered challenges together and forged new paths. The undercurrents of Compassion and Courage run deep and provide the wind at our backs, allowing us to look ahead in preparation for the next challenge.