Spotlight: A Closer Look at the One Big Beautiful Bill

Understanding the newest wave of tax reform—and how it might affect you.

On July 4, President Trump signed the “One Big Beautiful Bill” Act into law, marking the most sweeping tax changes since the 2017 Tax Cuts and Jobs Act (TCJA). The law introduces a mix of permanent extensions, temporary enhancements, and entirely new programs.

To help make sense of what’s changed, we’ve grouped the key provisions by topic—covering individual income tax, estate planning, charitable giving, business ownership, and new savings programs for children—so you can more easily see what may apply to your financial picture.

Summary of Major Tax Reforms

INDIVIDUAL INCOME TAX

Many of the temporary provisions from the 2017 tax law are now permanent, including current tax brackets and the expanded standard deduction. These changes are expected to benefit a broad range of taxpayers, especially retirees.

Many of the temporary provisions from the 2017 tax law are now permanent, including current tax brackets and the expanded standard deduction. These changes are expected to benefit a broad range of taxpayers, especially retirees.

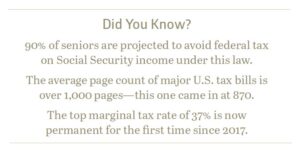

- The TCJA’s income tax brackets are now permanent; the top rate remains 37%.

- Standard deduction made permanent at $15,750 (Single) and $31,500 (Married Filing Jointly, “MFJ”).

- An extra $6,000 deduction is available for seniors; however, the provisions expire in 2028 unless extended.

- Approximately 90% of seniors are projected to avoid federal income tax on Social Security, though the benefits themselves remain taxable.

ESTATE PLANNING

The law locks in historically high estate tax exemptions, which may help high-net-worth families plan with more confidence.

- The estate tax exemption will reach $15 million per person in 2026, and is now permanent.

- Spousal portability remains, allowing a surviving spouse to inherit unused exemption amounts.

TIPS & OVERTIME INCOME

For some workers, the bill provides a new income tax exemption for tips and overtime pay, subject to income thresholds.

- Up to $25,000 in tip and overtime income is exempt from federal income tax.

- Still subject to employment tax and reporting requirements.

- This benefit expires in 2028.

STATE AND LOCAL TAX (SALT) DEDUCTION

After years of debate, the SALT deduction cap has been lifted, at least for now, for many taxpayers.

- The SALT deduction cap increases to $40,000 for AGIs under $500,000.

- It phases down to $10,000 for AGIs over $600,000.

- Applies equally to all filing statuses (marriage penalty).

- Scheduled to revert in 2030.

CHARITABLE GIVING

The law offers expanded incentives for charitable giving, including some new options for non-itemizers.

- Non-itemizers can now deduct up to $2,000 (MFJ) or $1,000 (Single) in charitable donations.

- Itemizers face a new 0.5% AGI floor for deductibility (similar to medical expense deductibility).

- The 60% AGI limit on cash donations to public charities is now permanent.

BUSINESS OWNERS

Business owners will benefit from the return of full bonus depreciation and continued access to state tax deduction strategies at the entity level.

- 100% bonus depreciation reinstated for assets placed in service after January 2025.

- Deductibility of state and local taxes via elective pass-through entity tax (PTET) regimes is preserved.

- 20% Section 199A deduction for Qualified Business Income made permanent.

“TRUMP ACCOUNTS” FOR CHILDREN

A new savings program aims to help families invest early in their children’s future.

- Children born between 2025–2028 receive a $1,000 federally funded account from the IRS.

- Parents may contribute up to $5,000/year; employers up to $2,500 (no deductions for either).

- Funds must be invested in approved U.S. mutual funds or ETFs.

- Distributions are generally prohibited before age 18 and fully taxable when withdrawn.

What This Could Mean for You

These reforms could create meaningful planning opportunities, especially for retirees, business owners, and high-income earners. But benefits vary based on your unique circumstances, and some provisions will expire unless extended.

Whether or not action is needed now, understanding how the law intersects with your financial plan can help position you more effectively for the future.

Want to Talk It Through?

If you’d like help assessing how these changes could affect your financial picture, reach out to your Bailard team or email tax@bailard.com. We’re happy to start the conversation and explore what’s possible.

Important: The above does not take into account the particular investment objectives, financial situations, or needs of individual clients. Neither Bailard nor any employee of Bailard can give tax or legal advice. The contents of this document should not be construed as, and should not be relied upon for, tax or legal advice.

Economic Brief: Tariff for Tat

Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) reflects on the start of America with Benjamin Franklin and the role of, and impact on, these $100 bill “Benjamins” today on trade, negotiations, and tariffs.

Founding father Benjamin Franklin wore many hats for our nascent republic, both literally and figuratively. Often depicted wearing a tricorn hat—de rigueur for the colonial era—Franklin famously donned a fur cap when he traveled to France in late 1776 as the key member of America’s first diplomatic delegation. Tasked with securing the vital support of Great Britain’s arch rival following the Declaration of Independence, he methodically curried favor at Versailles and amongst French nobility. Using the skills he honed while representing the colonies in London, Franklin worked relentlessly to advance America’s interests and procure France’s military and financial backing.

member of America’s first diplomatic delegation. Tasked with securing the vital support of Great Britain’s arch rival following the Declaration of Independence, he methodically curried favor at Versailles and amongst French nobility. Using the skills he honed while representing the colonies in London, Franklin worked relentlessly to advance America’s interests and procure France’s military and financial backing.

His carefully cultivated homespun image, complete with the fur cap, won Franklin a great deal of popularity. Fur caps became fashionable in Paris, and his likeness was embossed on collectible candy dishes, stitched into clothing, and engraved into snuff boxes and walking sticks. In February 1778, his efforts culminated in the signing of treaties that provided for a military alliance, recognized the United States as an independent nation, and established terms of commerce. It was a remarkable coup for our fledgling country and proved instrumental in winning the Revolutionary War. To Stacy Schiff, author of “Benjamin Franklin and the Birth of America,” France’s affection for Franklin was a critical factor: “Every other American envoy who approached Versailles bungled along the way. Franklin was inventing the foreign service out of whole cloth.”1

For over a century now the $100 bill has featured Franklin’s portrait, in honor of his indispensable role in America’s push for freedom. Today, it could be said that U.S. foreign relations depend more than ever on Benjamins—meaning those crisp $100 bills that cross oceans in exchange for goods. After an extended period of globalization, the current U.S. administration appears determined to rapidly de-globalize. Longtime foreign allies are scrambling to adjust to this policy pivot and the new D.C. power brokers are clearly not afraid to ruffle diplomatic feathers. In this “America First” approach, relationships with foreign governments seem to be largely transactional in nature and ruled by protectionist instincts. It is indeed all about the Benjamins in this new world order.

As the economy struggles to adapt to this paradigm shift, even the agenda setters have warned of possible near-term pain. In a March 2025 interview with CBS News, Commerce Secretary Howard Lutnick said the administration’s economic policies are worth it even if they lead to a recession. Many economists disagree, including former Treasury Secretary Larry Summers. He referred to tariffs as “a self-inflicted supply shock” and cautioned that inflation should move higher in response. Michael Goldstein, managing partner at New York-based Empirical Research Partners, estimates that the direct tariff impacts—combined with the impact from the associated uncertainties—could reduce 2025 real GDP (Gross Domestic Product) growth to the 1.0% to 1.5% range, while adding 0.5% – 1.0% to inflation. Similarly, Goldman Sachs hiked its 2025 core PCE (Personal Consumption Expenditures) inflation forecast to 3.5% due to tariffs, and lowered its 2025 GDP growth forecast to 0.5%. In doing so, Goldman Sachs upped its twelve-month recession probability to 45%, citing the expectation for sluggish growth, a deterioration in household and business confidence, and statements from White House officials indicating a greater willingness to tolerate near-term economic weakness in pursuit of their policies.

The Tariff Gambit

If the daily barrage of tariff-related news has you confused, you’re not alone. In fact, corporate executives feel the same. According to analysis from MarketWatch, 64 companies in the Standard & Poor’s (S&P) 500 Index mentioned policy uncertainty on their quarterly earnings call with analysts, up from 33 in the prior quarter. This lack of clarity could weigh on economic activity in the near-term, simply by slowing decision-making. Gill Segal, a University of North Carolina economist, observed that “Policy uncertainty, in particular, typically leads to lower business investment and lower future GDP, as a result.”

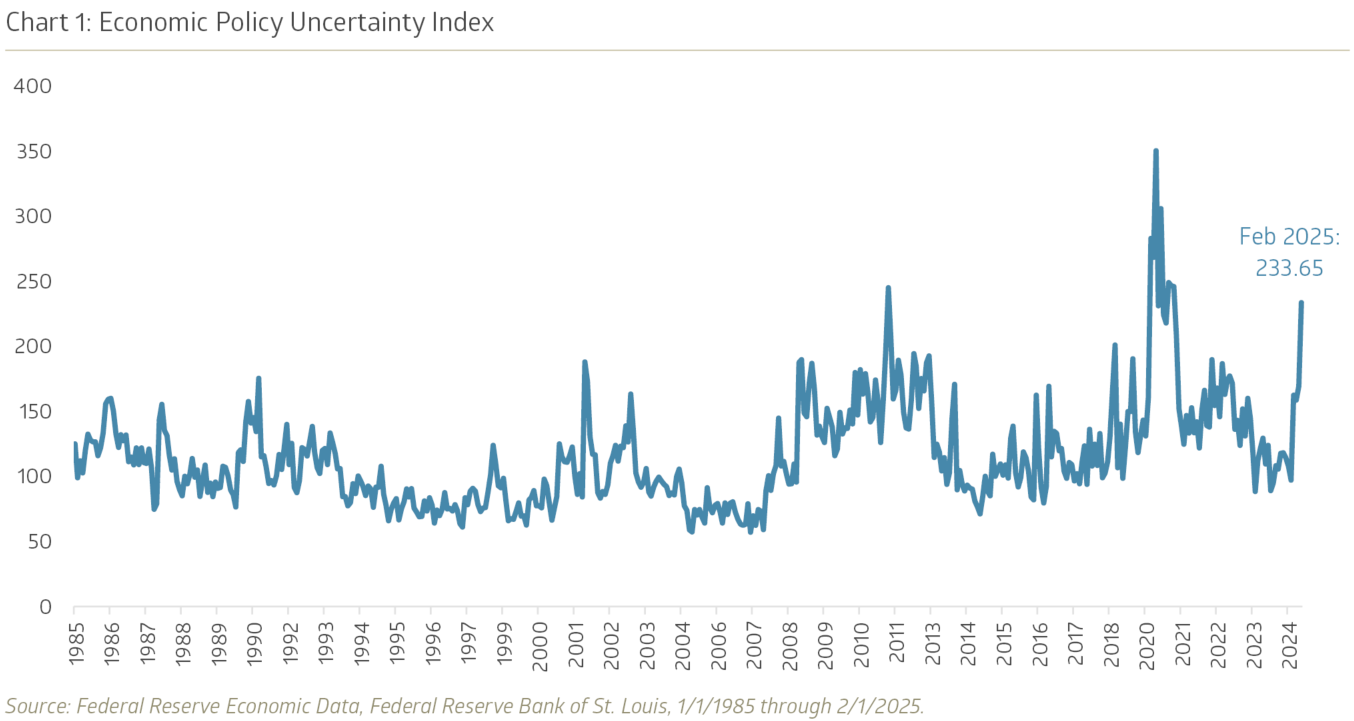

Empirical Research Partners has taken to titling their recent notes “The Fog of War.” A trade war is admittedly a different type of war, but it is sowing confusion. A trio of academics created an Economic Policy Uncertainty Index with data back to 1985. On their methodology, the level of uncertainty has only reached a higher level during the Great Financial Crisis (GFC) and the initial stages of the pandemic—both recessionary periods. Perhaps it’s not surprising that consumer sentiment readings have moved sharply lower year to date. The March 2025 reading for the University of Michigan’s Consumer Sentiment Index declined 28% year over year. In the release, Director Joanne Hsu said, “Consumers continue to worry about the potential for pain amid ongoing economic policy developments. Notably, two-thirds of consumers expect unemployment to rise in the year ahead, the highest reading since 2009.” Speaking at the U.S. Monetary Policy Forum in March, Federal Reserve (Fed) Chairman Jerome Powell assuaged these worries somewhat, noting that “Sentiment readings have not been a good predictor of consumption growth in recent years.”

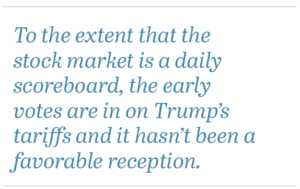

To the extent that the stock market is a daily scoreboard, the early votes are in on Trump’s tariffs and it hasn’t been a favorable reception. The “T is for Tariffs” playbook may rightly protect some industries, but the broad nature of the tariffs and the start-and-stop rollout clearly rattled the markets in the first quarter of 2025. Investors prefer greater degrees of predictability, making the erratic course that trade policy has followed less than ideal. They are also willing to pay more for perceived predictability, which is why the preference is often reflected in market valuations. For example, the S&P 500 Consumer Staples sector—filled with steady companies such as Costco Wholesale and Procter & Gamble—has traded at a forward price-to-earnings multiple nearly two points higher than the overall S&P 500 Index over the trailing 20 years. This, despite posting below-average earnings growth. More cyclical sectors or industries typically trade at lower valuations, an acknowledgement of their greater earnings variability. As such, it is a natural reaction for equity valuations to decline in periods of higher uncertainty. We are seeing that currently, with the S&P 500 Index’s forward price-to-earnings multiple about two points lower year to date. Still trading at roughly 20x forward earnings, the S&P 500 could see further multiple contraction without some fiscal and/or monetary policy relief.

To the extent that the stock market is a daily scoreboard, the early votes are in on Trump’s tariffs and it hasn’t been a favorable reception. The “T is for Tariffs” playbook may rightly protect some industries, but the broad nature of the tariffs and the start-and-stop rollout clearly rattled the markets in the first quarter of 2025. Investors prefer greater degrees of predictability, making the erratic course that trade policy has followed less than ideal. They are also willing to pay more for perceived predictability, which is why the preference is often reflected in market valuations. For example, the S&P 500 Consumer Staples sector—filled with steady companies such as Costco Wholesale and Procter & Gamble—has traded at a forward price-to-earnings multiple nearly two points higher than the overall S&P 500 Index over the trailing 20 years. This, despite posting below-average earnings growth. More cyclical sectors or industries typically trade at lower valuations, an acknowledgement of their greater earnings variability. As such, it is a natural reaction for equity valuations to decline in periods of higher uncertainty. We are seeing that currently, with the S&P 500 Index’s forward price-to-earnings multiple about two points lower year to date. Still trading at roughly 20x forward earnings, the S&P 500 could see further multiple contraction without some fiscal and/or monetary policy relief.

Reboot Button

Historically, political risk has been a factor that carries more weight in emerging market countries. Broadly defined as the risk that investment returns could be impacted by country instability or political changes, it has leapt up the list of concerns for investors in 2025. We don’t have to look too far back to see the political changes the market desires. In the wake of November’s election, optimism reigned around tax-friendly legislation, deregulation, inflation relief, and directional improvement in our nation’s fiscal fitness. Although the administration is working on each of those items, the checklist has clearly taken a backseat to an unwanted, deeply unpopular trade war. This is not the business-friendly approach that was promised. For a U.S. equity market that entered the year with high expectations built into valuations, this distraction (at best) has been enough to derail the market’s momentum.

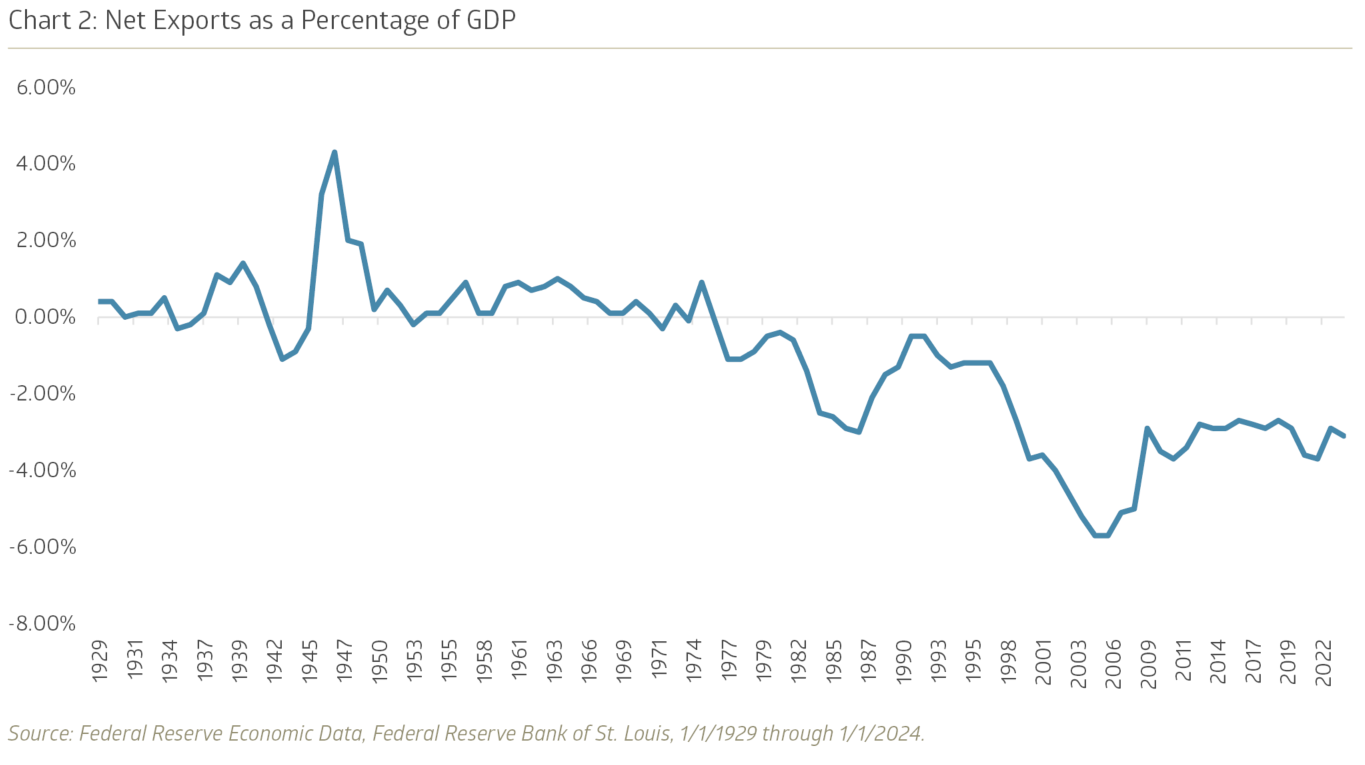

With the stroke of his pen—and President Trump has signed 109 executive orders alone thus far in his second term—we could see a realignment of the administration’s priorities. It is not too much to hope for, although the tariff troubles have already gone much further than expected. This myopic focus on our balance of trade is a bit puzzling, looking at historical data. Net exports as a percentage of GDP have drifted around the -3% territory since the Great Financial Crisis. It does subtract from U.S. GDP growth, but from a big picture standpoint the headwind is not particularly impactful. It seems like there is more risk in killing the goose that lays the golden eggs, so to speak.

Ultimately the equity markets should refocus on corporate profits, the long-term driver of stock prices. Earnings expectations for 2025 have edged lower, but only by around two percent for the S&P 500 year to date. For the multinational companies that heavily populate the large-cap universe, it will be more challenging to maintain profitability with rising input costs and reciprocal tariffs. The quarterly S&P 500 operating margin averaged close to 12% last year—but its average since 2006 has been 9.6%. To avoid an earnings shortfall versus expectations, corporations will need to carefully manage the trade off between passing prices along to customers and absorbing costs (sacrificing margins) to preserve sales. The foggy environment isn’t helping with that decision tree. Target Corporation, known for its bulls eye logo, announced in March that it will eschew offering quarterly guidance and move to only providing annual guidance numbers. Chief Financial Officer James Lee commented: “This change reflects our expectation of continued elevated volatility, which limits the effectiveness of quarterly forecasts.” Separately, Target said it would continue to move sourcing for its in-store brands, including All in Motion and Cat & Jack, away from China and toward Guatemala and Honduras.

Amidst the tariff tumult, positives remain. Importantly, the labor market remains strong with the unemployment rate at 4.2% versus a 50-year average of 6.1%. Federal government layoffs remain front page news, but with roughly three million workers that sector is fairly small compared to a little over 170 million in the civilian labor force. Monetary policy could also help: the futures markets now lean toward a Fed Funds target rate of 3.5% by year-end, a full percent below its current level.

Amidst the tariff tumult, positives remain. Importantly, the labor market remains strong with the unemployment rate at 4.2% versus a 50-year average of 6.1%. Federal government layoffs remain front page news, but with roughly three million workers that sector is fairly small compared to a little over 170 million in the civilian labor force. Monetary policy could also help: the futures markets now lean toward a Fed Funds target rate of 3.5% by year-end, a full percent below its current level.

In November 1789, about five months before his death, Benjamin Franklin wrote a letter to a French scientist. In that letter, Franklin offered what is now a famous quote: “Our new constitution is now established, everything seems to promise it will be durable; but, in this world, nothing is certain except death and taxes.” A wise man, that Franklin.

1 “Ben Franklin in Paris: How He Won France’s Support for the Revolutionary War,” www.history.com, 3/20/2024.

2 “Wall Street Journal editorial calls Trump tariffs ‘dumbest trade war in history,’ www.theguardian.com, 2/2/2025.

3 “Where We Stand: The Fog of War,” Empirical Research Partners, March 2025.

4 “US Daily: Countdown to Recession,” Goldman Sachs Investment Research, 4/6/2025.

5 “The word from U.S. companies to Wall Street in new Trump era is ‘uncertainty’,” www.morningstar.com, 3/20/2025.

6 “Surveys of Consumers,” www.sca.isr.umich.edu, March 2025.

7 “Guide to the Markets,” JPMorgan Asset Management, March 2025.

8 “S&P 500 Earnings and Estimate Report,” www.spindices.com, 3/31/2025.

9 Target Corporation Q4 2024 earnings call, 3/4/2025.

10 “Target braces for first-quarter profit pressure due to tariffs, low demand,” www.reuters.com, 3/4/2025.

11 “Benjamin Franklin’s last great quote and the Constitution,” www.constitutioncenter.org, 11/13/2023.

Financial Spring Cleaning: Small Steps for Big Impact

In a special feature this quarter, Lena McQuillen, CFP® (Vice President and Director of Financial Planning) and Dave Jones, JD, LLM, CFP® (Senior Vice President and Director of Estate Strategy) have joined forces and prepared a set of practical ways to refresh and organize your finances this season.

As the seasons change, it’s an ideal time to refresh and organize different aspects of life—including your finances. Making improvements doesn’t have to be overwhelming or time-consuming. The power of small, actionable steps is that they add up over time, leading to meaningful progress. Instead of tackling everything at once, focusing on quick, manageable tasks ensures steady progress without the stress of a complete financial overhaul.

Each of the following steps is simple to implement and provides a tangible benefit. Whether you take on one today and another next month or work through them gradually, every action moves you toward a stronger financial foundation. Setting aside just 15-30 minutes each week for financial check-ups can make these tasks feel effortless while delivering long-term security and peace of mind.

- Use Everplans for Important Documents

Keeping important financial documents in order can make a significant difference in times of need. Yet, many people store essential papers in multiple places, making access difficult for both them and their families. Everplans is a secure digital platform that allows you to safely store and organize important financial, legal, and personal documents in one place. This simple step helps ensure critical information is available when needed.

Time commitment: 30-45 minutes.

How to get started:

- Upload estate planning documents—wills, trusts, powers of attorney, and advance directives.

- Store financial records, such as bank accounts, investment portfolios, and retirement plans.

- Keep personal records (birth certificates, marriage licenses, Social Security information) in a secure location.

- Don’t forget to include legacy items like family recipes, cherished photos, and letters to loved ones.

- Assign access to trusted individuals so they know how to retrieve documents when needed.

- Freeze Your Credit and Monitor Your Credit Report

Identity theft can be financially and emotionally devastating, and prevention is much easier than recovery. One of the most effective ways to protect yourself is by freezing your credit, which blocks unauthorized access to your financial profile. It’s free and quick to freeze your credit, and you can temporarily lift or remove the freeze when needed. Additionally, monitoring your credit report helps catch inaccuracies and signs of fraud early.

Time commitment: 15 minutes.

How to take action:

- Contact each of the three major credit bureaus separately to place a freeze on your credit. They’ll ask for your full name, date of birth, Social Security Number, and address, so be prepared.

- Equifax – Freeze Your Credit Here or call 1-800-349-9960

- Experian – Freeze Your Credit Here or call 1-888-397-3742

- TransUnion – Freeze Your Credit Here or call 1-800-680-7289

- Each bureau will issue a PIN or password, store this securely for future updates

- Review your credit report annually to ensure accuracy.

- Streamline Subscriptions and Recurring Expenses

Monthly and annual subscriptions can quietly accumulate, leading to unnecessary spending. Many of these expenses go unnoticed or are no longer providing value. Taking a few minutes to review and optimize recurring charges can free up resources for more meaningful financial priorities.

Time commitment: 15-20 minutes.

Steps to simplify your subscriptions:

- Review recent bank and credit card statements to identify recurring charges.

- Cancel or downgrade subscriptions that are no longer used or needed.

- Set calendar reminders for renewals of major services to reassess their value before automatic charges occur.

- Update Digital Passwords and Security Measures

Cybersecurity threats continue to evolve, and financial accounts are prime targets for fraud. Strengthening your digital security doesn’t require complicated tech skills—small updates can make a big difference in protecting your wealth.

Time commitment: 20 minutes.

Easy ways to enhance digital security:

- Update passwords for financial and personal accounts—if you’ve been using the same password for years, now is the time to change it.

- Avoid using the same password across multiple platforms.

- Enable two-factor authentication whenever possible to add an extra layer of protection against unauthorized access.

- Use a password manager to securely store login credentials rather than relying on memory or sticky notes.

- Conduct a Beneficiary Check-Up

Most financial institutions allow you to designate beneficiaries, which ensures that your assets transfer smoothly to the right individuals when the time comes. However, life events—such as marriages, divorces, or births—can impact your original choices. A quick check of your financial accounts, either online or with your provider, ensures that your assets are aligned with your wishes. This small but essential step prevents unnecessary legal complications down the road.

Time commitment: 20-30 minutes.

Where to check beneficiaries:

- Retirement Accounts, including 401(k), IRA, and Roth IRA

- Life Insurance Policies

- Bank and Investment Accounts

- Estate Planning Documents

- Review Annual Gifting and Charitable Contributions

Strategic annual gifting can help reduce estate tax burdens while allowing you to support your loved ones and favorite causes. Whether giving to family, friends, or charities, a structured approach can ensure your generosity is both intentional and efficient.

Time commitment: 30 minutes

How to approach gifting:

- Review annual exclusions – You can gift up to $18,000 per recipient in 2024 without incurring gift taxes.

- Evaluate Donor-Advised Funds (DAFs) or direct charitable gifts to optimize tax efficiency.

- Plan the timing of gifts, as early-year contributions may provide greater impact.

- Ensure Proper Titling of Accounts and Assets

Properly titling your financial accounts and assets is one of the simplest yet most effective ways to ensure your estate plan functions as intended. Incorrect titling can help you avoid future headaches including probate delays, tax inefficiencies, or unintended asset distribution.

Time commitment: 30-45 minutes.

What to review:

- Confirm that bank, brokerage, and investment accounts are correctly titled.

- Ensure real estate properties are held under the appropriate ownership structure.

- If you have a trust, check that assets are titled in the trust’s name to avoid probate delays.

Final Thoughts: Small Steps, Big Impact

Taking small, thoughtful steps today can make a significant difference in your financial security. Whether you tackle one item this month or make financial check-ups a regular habit, each action helps build a stronger, more organized financial future.

As always, your Investment Counselor is here to help with any of these steps. If you have questions or need guidance, don’t hesitate to reach out.

A few minutes each week can go a long way, keep track by checking off each step below.

- Use Everplans for Important Documents

- Freeze Your Credit and Monitor Your Credit Report

- Streamline Subscriptions and Recurring Expenses

- Update Digital Passwords and Security Measures

- Conduct a Beneficiary Check-Up

- Review Annual Gifting and Charitable Contributions

- Ensure Proper Titling of Accounts and Assets

1 Berkshire Hathaway Inc. News Release. 25 November 2024. https://www.berkshirehathaway.com/news/nov2524.pdf

White Paper: "AI Is Moving Fast—And the Winners Might Not Be Who You Expect"

AI is evolving fast, and so is the way investors are approaching it. In his latest white paper, Dave Harrison Smith, CFA—EVP, Domestic Equities—shares where he sees the shift in AI investing, from buildout to opportunity. Read on for his full analysis:

Kiplinger: "Private Credit: Coming Soon to a Portfolio Near You"

Private credit could be a good source of diversification for sophisticated investors, but beware of the risks.

Economic Brief: It Don't Mean a Thing, If It Ain't Got That Swing

This quarter, Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist – Wealth Management, and Portfolio Manager – Sustainable, Responsible and Impact Investing) delves into the paradoxes of momentum investing, inflation’s persistent influence, and the resilience of the U.S. economy in an era of shifting market dynamics.

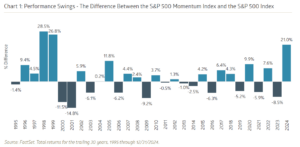

Contrarians are not having a moment. Those resolute and hardy investors who row against the tide of popular opinion—shunning trendy stocks and embracing the unloved—found themselves sinking in 2024. A tidal wave of capital flowed into the fashionable set of equities, largely comprised of companies with a plausible artificial intelligence (AI) story. Winners kept on winning, resulting in a historic rout for momentum investing. In fact, the Standard & Poor’s (S&P) 500 Momentum Index had its best year relative to the overall S&P 500 Index since 1999. It soared 46%, including dividends, outpacing the benchmark S&P 500 by 21 percentage points.

and embracing the unloved—found themselves sinking in 2024. A tidal wave of capital flowed into the fashionable set of equities, largely comprised of companies with a plausible artificial intelligence (AI) story. Winners kept on winning, resulting in a historic rout for momentum investing. In fact, the Standard & Poor’s (S&P) 500 Momentum Index had its best year relative to the overall S&P 500 Index since 1999. It soared 46%, including dividends, outpacing the benchmark S&P 500 by 21 percentage points.

Launched a decade ago—but recalculated back to 1994—the S&P 500 Momentum Index includes the top quintile of the S&P 500 based on trailing 12-month price performance. The Index is rebalanced on a semi-annual basis. As investment concepts go, it does not get any simpler than selecting stocks solely based on price strength. It also challenges conventional thinking: buy low, sell high. Nonetheless, momentum investing has worked over longer timeframes (see Chart 1), although the approach can suffer painful reversals and has not outperformed in more than two consecutive years since the late 1990s. Academics have struggled to pinpoint why momentum investing succeeds. The performance edge is well-documented with a long track record. A 1993 article in the Journal of Finance is cited as the pioneering study on momentum.1 The authors presented data showing that buying recent stock winners and selling losers produced significantly higher short-term returns than the overall U.S. stock market during the 1965 to 1989 time period. This ongoing performance anomaly could be partly attributed to behavioral factors such as FOMO (fear of missing out) and a bandwagon effect.2 The “Big Mo” might also reflect fundamental strength (rising sales, e.g.) already embedded in prices that can persist in the short-term.

Akin to a snowball rolling downhill, momentum investing is driving ever-larger market capitalizations and a more concentrated U.S. large-cap stock market. As one example, the four largest holdings in the S&P 500 Momentum Index—Amazon.com, NVIDIA, Broadcom, and Meta Platforms—carry a combined market capitalization of $8.2 trillion, greater than the cumulative market cap of roughly the bottom 64% of the S&P 500. Morgan Stanley equity strategist Mike Wilson touched on the intersection between momentum and market concentration in a December note. “Another consideration is the growing propensity of investors to use price momentum as a key factor in their investment strategy. Rebalancing has also been de-emphasized as many investors have let their winners run, given the lack of mean reversion in the past several years. This all helps to explain the extreme concentration we’re seeing in many equity markets, not just in the United States.”3

To borrow from Sir Isaac Newton, momentum is the product of mass times velocity, so perhaps this makes some sense. We have exceptionally large companies moving at a fast pace and creating the momentum that helped lift the S&P 500 Index to a greater than 20% return in 2024 for the third time in the last four years. These market moves have been underpinned by robust asset flows into U.S. equities. According to The Wall Street Journal, investors added over $1 trillion to U.S.-based exchange-traded funds (ETFs) last year, shattering the previous record set in 2021.4 Not surprisingly, momentum ETFs were a popular choice. Invesco’s S&P 500 Momentum ETF pulled in over $3 billion of net purchases over the first 11 months of 2024—incredible growth considering the fund now has around $4 billion under management.5 The hot money trades seeking instant gains may prove ill-timed if the AI trade falters, but until then investors are siding with inertia. As the late New York Yankee great Yogi Berra once said: “Nobody goes there anymore. It’s too crowded.”

The Real Return

A leading kryptonite candidate for the equity markets could be higher-than-expected interest rates. The post-COVID inflation shock still reverberates today, even though the Consumer Price Index (CPI) year-over-year growth rate peaked in mid-2022. As of November 2024, the CPI growth rate was down to 2.7%, a full point below the 50-year average of 3.7%. Price growth has clearly decelerated, but not reversed, and the cumulative impact has made life uncomfortable for policymakers. There is a compelling argument that inflation cast a deciding vote in the recent presidential election. U.S. Federal Reserve Chair Jerome Powell acknowledged in his December press conference that inflation “remains somewhat elevated relative to our two percent longer-run goal.”6 This comment followed after the Fed’s decision to cut the Federal Funds target range to an upper limit of 4.5%, marking a third consecutive easing from its peak of 5.5%.

Any enthusiasm for the (expected) rate cut was quickly doused when Fed watchers realized that the updated Federal Open Market Committee (FOMC) projections implied only two additional rate cuts in 2025. Questioned on this in the press conference, Powell flagged the uncertain inflation outlook. He continued: “And, you know, the point of that uncertainty is it’s kind of common sense thinking that when the path is uncertain you go a little bit slower. It’s not unlike driving on a foggy night or walking into a dark room full of furniture. You just slow down.” An apt metaphor with wonderful imagery, but investors were not impressed. The S&P 500 Index traded down 2.95% in response, the second-worst trading session of 2024 and one of only four greater than 2% daily declines for the year.

Rate anxiety is real. With a more cautious FOMC outlook, the 10-year U.S. Treasury Note yield rose 78 basis points,7 or 0.78%, during the fourth quarter, finishing at 4.57%. The S&P 500 Equal Weighted Index declined 2.3% price-only in Q4, perhaps illustrating the perceived impact of higher rates on the average (smaller) S&P 500 company. Further down the market cap spectrum, the S&P SmallCap 600 Index declined 1.0% over the final quarter of 2024. Ebbing inflation will obviously continue to be a key to interest rate stability in 2025. Without further disinflation progress, bond investors may require a higher real, or inflation-adjusted, return. Longer-term rates may rise regardless, considering our country’s inconvenient $36 trillion (and counting) debt load. This has some analysts watching the horizon for the return of the “bond vigilantes,” those disaffected bond traders who sell bonds—driving yields higher—to signal unhappiness with fiscal and/or monetary policies.

Over the last 30 years, as seen in Chart 2, the median spread between the 10-year U.S. Treasury Note yield and the Fed Funds target rate has been 121 bps. At year-end 2024 the spread was a miniscule 8 bps. The most straightforward path to normalize that relationship is further easing by the FOMC, combined with a steady 10-year yield. However, as the Fed would say, this will all be data dependent. Inflation will need to cool further, which would allow the FOMC to proceed on its intended rate cut plan. Any missteps could result in higher long-term yields, harming not only the bond market, but equities as well. With the S&P 500 Index trading at nearly 22x projected 2025 operating earnings—versus a long-term median of approximately 17x—there is not a lot of room for error.

Steady as She Goes

Although inflation dominated headlines again in 2024, particularly during the run-up to the presidential election, overall U.S. economic growth has been resilient. Gross Domestic Product (GDP) grew at a roughly 3% inflation-adjusted rate over the middle six months of 2024, and is estimated to have decelerated to a still solid 2.4% growth rate in Q4.8 The ongoing struggle to foster economic gains for a wider swath of the population continues. While the service economy chugs along, the goods-producing sector remains stuck in neutral. The Institute for Supply Management (ISM) reported that economic activity in the manufacturing sector declined for a ninth consecutive month in December.9 ISM’s survey has actually indicated a manufacturing contraction for 25 of the last 26 months, although the December reading did include some green shoots with new orders and production both in expansion territory.

The U.S. economy is much more dependent on services than goods, of course. In 2023, over 67% of Personal Consumption Expenditures (PCE) went to services, with goods accruing the other 33%.10 According to BlackRock’s Rick Rieder, head of global asset allocation, we may be needlessly worrying about whether the economy will experience a hard or soft landing. Instead, he suggests we think about the U.S. economy as a satellite: “Satellites don’t land. They just get tired over time, and they need a bit more energy…The Fed raises rates 500 basis points, and it doesn’t make a difference, and it’s because the service economy is not cyclical. Goods are hugely cyclical.”11

Rieder’s argument feels like a trap: an explanation designed to fit the narrative since we have only experienced one, technically brief (COVID) recession over the trailing 15 years. It likely contains some truth, however. The economy has recently weathered some “rolling recessions” in which only certain sectors experience a downturn. Perhaps our predominantly service economy can help minimize overall cyclicality, outside of the black swan events. Disappointingly, it will not remove uncertainty, unless AI solves that problem, too. To pull another Yogiism, or pearl of wisdom from Yogi Berra: “It’s tough to make predictions, especially about the future.”

Rieder’s argument feels like a trap: an explanation designed to fit the narrative since we have only experienced one, technically brief (COVID) recession over the trailing 15 years. It likely contains some truth, however. The economy has recently weathered some “rolling recessions” in which only certain sectors experience a downturn. Perhaps our predominantly service economy can help minimize overall cyclicality, outside of the black swan events. Disappointingly, it will not remove uncertainty, unless AI solves that problem, too. To pull another Yogiism, or pearl of wisdom from Yogi Berra: “It’s tough to make predictions, especially about the future.”

1 “Momentum Investing: It Works, But Why?”, www.anderson-review.ucla.edu/momentum, 10/31/2018.

2 “Momentum Investing: what it is, why it works and what to buy,” www.moneyweek.com, 6/15/2018.

3 “What Is Breadth Telling Us?”, Morgan Stanley Research Sunday Start, 12/22/2024.

4 “A Record-Shattering $1 Trillion Poured Into ETFs This Year,” www.wsj.com, 12/30/2024.

5 “Investors Are Looking to Momentum ETFs in 2024,” www.etftrends.com, 11/29/2024.

6 “Transcript of Chair Powell’s Press Conference,” www.federalreserve.gov, 12/18/2024.

7 A basis point (bp) is 0.01%.

8 GDPNow, www.atlantafed.org, 1/3/2025.

9 “Manufacturing PMI® at 49.3%,” www.ismworld.org, 1/3/2025.

10 “Gross Domestic Product (Third Estimate), Third Quarter 2024,” www.bea.gov, 12/19/2024.

11 “DealBook: R.T.O. battle,” www.nytimes.com, 10/12/2024.

Planning for Generational Wealth: Maximizing Tax Efficiency

Lena McQuillen, CFP®, Vice President and Director of Financial Planning, outlines the distinctions between Traditional and Roth retirement strategies, when each is most effective, the implications of new laws, and ways to share these insights with your family.

For those who have already built their wealth, the focus shifts to preserving it, optimizing its use in retirement, and empowering future generations to achieve financial success in a tax-efficient manner. Many readers will have already made key decisions about their retirement accounts—such as 401(k)s, 403(b)s, or 457(b)s—during their working years. Now, the opportunity lies in maximizing those decisions to enhance your family’s financial well-being. Just as you’ve built and managed your wealth, you can pass on the knowledge and strategies to help your family achieve similar success. The choice between Traditional and Roth accounts remains pivotal, offering different advantages for optimizing outcomes both now and in the future. Understanding these options can help refine your strategy and empower your heirs, equipping them with the tools to build on your financial legacy.

Understanding the Basics

A Traditional 401(k) allows contributions on a pre-tax basis, reducing taxable income during your working years. Over time, these funds grow tax-deferred, but taxes are owed on withdrawals. Required minimum distributions (RMDs) begin at age 73 (or age 75 if born in 1960 or later), impacting your taxable income in retirement.

Roth 401(k) contributions, made with after-tax dollars, offer a different advantage: earnings grow tax-free, and qualified withdrawals are not taxed if the account has been open for at least five years and withdrawals are made after age 59½. Additionally, Roth accounts bypass RMDs, allowing assets to grow tax-free indefinitely—a benefit particularly valuable for estate planning. For families managing wealth across generations, Roth accounts can provide a powerful vehicle for tax-free growth over your lifetime.

How Much Can You Contribute?

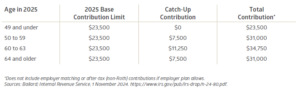

The SECURE 2.0 Act has introduced new opportunities for optimizing retirement accounts. In 2025, enhanced catch-up contributions allow individuals aged 60 through 63 to contribute up to $11,250 beyond the $23,500 base limit. If your children or grandchildren are early in their careers, encouraging them to maximize contributions to their own accounts can set the stage for long-term financial security.

Additionally, employers now have the option to match contributions to Roth accounts, providing additional flexibility for wealth transfer and reinforcing the value of maximizing contributions to these accounts early.

How Much Should You Contribute?

- While contributing the maximum may no longer apply to you personally, consider how these strategies can be leveraged for your family: For Children and Grandchildren: Encourage them to maximize Roth contributions early in their careers, reaping the benefits of tax-free growth over decades. Highlight the importance of contributing enough to qualify for employer matching funds—essentially free money that accelerates their savings—to make the most of their retirement plans. Also encourage them to evaluate their living expenses relative to their salary for a sustainable savings rate that balances immediate needs with long-term goals.

- Managing Your RMDs: Strategically converting portions of Traditional accounts to Roth during years with lower taxable income can reduce the impact of future RMDs. For your heirs, guiding them in understanding how RMDs may affect inherited accounts and encouraging early planning can optimize their tax efficiency, supporting a smoother transfer of wealth.

- Integrating Contributions: Use your resources to gift or match contributions to family members’ retirement accounts, fostering their financial independence. Consider offering a dollar-for-dollar match on your grandchild’s Roth IRA contributions. For instance, if they contribute $3,000 from their summer job earnings, you match it with another $3,000 (up to their total earnings or annual limit, whichever is less). This not only incentivizes their savings habit but also allows them to maximize tax-free growth potential from a young age, leveraging decades of compounding.

These actions not only benefit your family but also extend the tax-efficient strategies that have supported your success. If contributing the maximum feels daunting to your younger loved ones, suggest they start small. Gradually increasing the allocation as income rises or debts are paid off can ease the transition while building wealth consistently.

Factors to Consider: Maximizing Family Wealth

When planning for your family’s financial future, understanding the role of Traditional and Roth accounts is critical. These tools offer unique advantages that can help optimize your wealth strategy and leave a lasting legacy.

Traditional Pre-Tax Accounts

Traditional Pre-Tax Accounts

Traditional 401(k) accounts are effective for managing current cash flow but require thoughtful tax planning to maximize their benefits and minimize liabilities. By reducing adjusted gross income (AGI), they can also provide additional flexibility for managing tax brackets. Converting funds to Roth accounts during low-income years can mitigate RMD impacts and leave more tax-efficient assets to heirs.

Roth Accounts

Roth 401(k)s offer significant flexibility for legacy planning. Contributions grow tax-free, withdrawals are not taxed, and they provide a strategic tool for multi-generational wealth transfer. Encouraging younger family members to prioritize Roth contributions amplifies these benefits.

Splitting Contributions Between Pre-Tax and Roth Accounts

Allocating contributions across pre-tax and Roth accounts provides flexibility to adapt to tax law changes or shifting financial priorities. This approach helps families draw funds in the most tax-efficient manner. Additionally, starting in 2026, catch-up contributions for high earners must be directed to Roth accounts, highlighting the importance of considering both account types in your overall strategy.

An Example of Strategic Allocation in Action

Meet Chloe and Nathan: Recently retired professionals, Chloe and Nathan transitioned from high-earning careers to focusing on wealth preservation and supporting their family’s financial growth. With significant Traditional and Roth retirement accounts, their approach emphasizes tax efficiency and legacy planning.

- Strategic Conversions: During low-tax years, they convert portions of their Traditional 401(k) accounts to Roth accounts. This minimizes future RMDs, maximizes tax-free growth, and provides greater flexibility for drawing retirement income.

- Legacy Planning: Chloe and Nathan prioritize leveraging their Roth accounts to create tax-efficient wealth transfer opportunities. This strategy enables their heirs to benefit from tax-free growth while supporting the family’s long-term financial goals.

- Mentoring the Next Generation: They mentor their adult children on the importance of early saving and tax diversification, particularly through Roth contributions, fostering strong financial habits and long-term independence.

Chloe and Nathan’s thoughtful strategy not only secures their retirement but also sets up their family for financial success, illustrating how retirement planning evolves with life’s stages.

Next Steps

Managing wealth in retirement involves more than sustaining your lifestyle; it’s about building a foundation for future generations to thrive financially. Consider these steps:

- Evaluate Family Tax Strategies: Collaborate with your Investment Counselor to optimize tax efficiency for both current and future generations. For individuals in a higher tax bracket now, contributing to a Traditional 401(k) may make the most sense. Conversely, for those currently in a lower tax bracket, Roth contributions may be more advantageous.

- Foster Financial Education: Use your experience to mentor younger family members on the value of Roth accounts, tax diversification, and long-term planning. Estimate retirement income needs and work with your Investment Counselor to model various scenarios. This includes understanding the impact of diverse income sources such as Social Security and investments.

- Reassess Regularly: Life events, tax law changes, and shifting priorities necessitate periodic adjustments to any strategy. Annual check-ins help keep your plan aligned with financial objectives.

For those no longer contributing to a 401(k), integrating these practices helps you leave a legacy that supports your family’s financial success while minimizing tax burdens.

Conclusion

Choosing between a Traditional pre-tax 401(k) or a Roth 401(k) is not a one-size-fits-all decision; it depends on your unique financial situations, long-term goals, and tax environment. As you transition into retirement, the focus shifts from building wealth to preserving it and empowering your family. Thoughtful planning and informed choices today lay the groundwork for a secure tomorrow. Working closely with a trusted partner helps to ensure that your legacy not only supports your heirs but also instills financial independence and security for generations to come.

Estate Planning Gold: Insights from Warren Buffet's 2024 Letter

Join Director of Estate Strategy, Dave Jones, JD, LLM, CFP®, as he explores Warren Buffett’s timeless insights on estate planning, highlighting actionable principles to guide thoughtful and purposeful generational wealth strategies.

On November 25, 2024, just days before Thanksgiving, Warren Buffett released a letter to shareholders of Berkshire Hathaway Inc.1 Unlike the usual updates on business operations or investments, this letter carried a heartfelt message filled with timeless wisdom on estate planning. Buffett shared reflections on mortality, responsibility, simplicity, and transparency—principles that are as practical as they are profound. For those tasked with managing generational wealth, his insights provide not only lessons but a roadmap for purpose-driven planning. As we begin the new year, let’s examine these lessons and consider how they might inspire our own approach to estate planning.

Acknowledge Mortality

“Father time always wins. But he can be fickle—indeed unfair and even cruel—sometimes ending life at birth or soon thereafter while, at other times, waiting a century or so before paying a visit. To date, I’ve been very lucky, but, before long, he will get around to me.”

In reflecting on the passage of time, Buffett addresses an essential truth: none of us can escape it. Planning for the future is both prudent and necessary. While reflecting on his own life and luck, he emphasizes the importance of taking proactive steps to ensure that his estate planning is handled responsibly. For Buffett, this means facing mortality head-on and making thoughtful decisions about the future.

The new year is an ideal time to consider your own plans. How can you prepare now to give your loved ones clarity and peace of mind when the time comes?

Choose the Right Successor(s)

“[T]omorrow’s decisions are likely to be better made by three live and well-directed brains than by a dead hand. As such, three potential successor trustees have been designated. Each is well known to my children and makes sense to all of us.”

Choosing the right successors is a cornerstone of Buffett’s estate planning philosophy. His selection of capable trustees—respected by both himself and his family—emphasizes the importance of communication, collaboration, and accountability. By involving his children in the process, Buffett fosters alignment and clarity.

For your own estate, think about the individuals who could best carry out your wishes. Are they prepared to handle the responsibilities you’re entrusting to them? Clear communication and thoughtful choices now can make all the difference later.

Give Responsibly

“[Susie] left $10 million to each of our three children, the first large gift we had given to any of them. These bequests reflected our belief that … wealthy parents should leave their children enough so they can do anything but not enough that they can do nothing.”

This sentiment encapsulates Buffett’s philosophy of responsible giving. While financial security is a gift, excess can stifle ambition and purpose. By leaving “enough to do anything but not enough to do nothing,” Buffett fosters independence and encourages his heirs to carve out their own paths in life.

Not every family will relate to or need such a framework, but it’s a principle worth reflecting on. What balance will empower your loved ones without diminishing their drive? This new year, evaluate how your legacy can support growth and self-reliance.

Make It Simple

“I change my will every couple of years – open only in very minor ways – and keep things simple. Over the years, Charlie [Munger] and I saw many families driven apart after the posthumous dictates of the will left beneficiaries confused and sometimes angry.”

Simplicity is a hallmark of Buffett’s estate planning philosophy. Complexity breeds confusion, resentment, and potential conflict among beneficiaries. By keeping his will straightforward and regularly updated, Buffett avoids potential disputes and provides clarity.

As you think about your own plans, ask yourself: Could someone easily understand and implement your wishes? Simplicity may be the key to preserving harmony within your family.

Be Transparent and Flexible

“I have one further suggestion for all parents, whether they are of modest or staggering wealth. When your children are mature, have them read your will before you sign it.

Be sure each child understands both the logic for your decisions and the responsibilities they will encounter upon your death. If any have questions or suggestions, listen carefully and adopt those found sensible. You don’t want your children asking ‘Why?’ in respect to testamentary decisions when you are no longer able to respond.

Over the years, I have had questions or commentary from all three of my children and have open adopted their suggestions. There is nothing wrong with my having to defend my thoughts. My dad did the same with me….”

Transparency is perhaps Buffett’s most transformative principle. By discussing his will openly with his children, he fosters alignment, understanding, and a shared sense of purpose. This collaborative approach strengthens familial bonds and preempts conflicts that could arise later.

While not all family dynamics allow for such openness, it’s worth considering where possible. Honest conversations about your intentions can reduce misunderstandings and increase trust. As we move into a new year, could greater transparency in your plans create more unity and clarity?

Final Thoughts

Warren Buffett’s 2024 letter provides a compelling framework for intentional, values-driven estate planning. By acknowledging mortality, giving responsibly, keeping things simple, and prioritizing transparency, Buffett offers a model for creating a legacy that balances financial security with purpose.

As you reflect on your plans for the year ahead, take inspiration from Buffett’s insights. Estate planning isn’t just about transferring wealth—it’s about fostering unity, empowering future generations, and making meaningful impact. May the new year bring clarity and peace to your planning.

1 Berkshire Hathaway Inc. News Release. 25 November 2024. https://www.berkshirehathaway.com/news/nov2524.pdf

Economic Brief: Shadow of Doubt

Not all pauses are created equal. Jon Manchester, CFA, CFP® (Senior Vice President, Chief Strategist, Wealth Management, and Portfolio Manager, Sustainable, Responsible and Impact Investing), shares how this one mattered.

There is power in the pause. Take a breath, stop to think, sleep on it. In this rapid reaction, first to land the ‘digital’ punch world, we could probably all benefit from a hesitation move. This is well understood in the field of psychology, where the late Austrian psychologist Viktor Frankl is credited with saying “Between stimulus and response, there is a space. In that space is our power to choose our response. In our response lies our growth and our freedom.” That power is also appreciated by the financial markets, particularly when the pause removes—at least temporarily—a perceived impediment. A mere week after announcing sweeping “Liberation Day” tariffs in early April, President Trump largely shelved the plan for 90 days. He explained that people “were getting a little bit yippy, a little bit afraid.” The remark, in keeping with the President’s signature off-the-cuff style, lent support to the idea of a “Trump put;” broadly meaning that the President uses the markets as a barometer for his policies and then adjusts accordingly. Equity investors clearly had a case of the yips: the Standard & Poor’s (S&P) 500 Index traded down more than 15% in response to the trade war escalation. The bond market trembled as well. The 10-year U.S. Treasury Note yield jumped roughly 30 basis points higher in a matter of days and reportedly caused Trump’s inner circle to fear sparking a financial crisis.

Wall Street does enjoy a good “kick the can down the road” party, whether it is yet another increase to the debt ceiling or an injunction delaying new regulations. This time was no different. In fact, Strategas Research Partners noted it took just 55 days for the S&P 500 to return to a new high—the fastest recovery following a 15% drawdown in history. The dizzying ascent, which resulted in the S&P 500’s best quarter since December 2023, has left some market participants puzzling over the dichotomy between what they feel and what stock prices show. Amidst the noise of an unresolved trade war, Middle East hostilities, floundering consumer confidence numbers and other disconcerting data, it is not particularly surprising that there is a degree of cognitive dissonance involved here. This mental discomfort is actually a fairly routine aspect of investing. There is always a laundry list of doubts casting a shadow over the markets, the so-called wall of worry. The dissonance is only exacerbated by inherent contradictions in the financial markets. For example, the bad news is good news phenomenon. In recent years, weak economic data (seemingly bad) has cheered investors conditioned for the sugar high of easier monetary policy or fiscal policy support. It creates confusion around exactly what we are rooting for as investors and an incongruous feeling as equities trade higher on disappointing news.

We Now Return to Our Regularly Scheduled Programming

The 90-day pause on “reciprocal” tariffs allowed the markets to refocus on corporate earnings and guidance. A notable positive in this interim was reaffirmation around the equity market’s dominant theme: artificial intelligence (AI). With doubts starting to creep in, the large-scale cloud service providers offered reassuring guidance in April regarding planned capital expenditures (capex) for 2025. Alphabet stuck with its $75 billion bogey, saying it continues to have more customer demand for Cloud services than it has capacity. Meta Platforms raised its capex guidance range to $64 to $72 billion, up from $60 to $65 billion previously. Microsoft was rumored to have cancelled projects during the quarter, but its capex spending ran at a roughly $67 billion annualized rate and the company said it expects to grow capex in fiscal 2026. The sheer magnitude of these numbers is indicative of how these companies perceive the AI opportunity. In the lull following the storm of tariff-related headlines, the announcements provided a needed dose of confidence to equity markets and reinvigorated the AI trade. By the end of the second quarter, leading AI semiconductor companies ranked among the best performers for the three-month period, including Broadcom (+65%) and NVIDIA (+46%).

The resumption of tech leadership within the S&P 500—Semiconductors and Software were the top performing industry groups last quarter—lent an air of business as usual to the markets. It also took the large-cap index back up to an elevated valuation, trading at more than 22x estimated earnings for the next 12 months. As has been the case in recent years, however, the average stock is significantly cheaper. The S&P 500 Equal Weight Index finished June with a projected 17.8x forward price/earnings multiple. Over 200 stocks in the S&P 500 declined during the second quarter, reflecting a tougher environment for companies lacking real estate on the high-priced AI (or crypto) avenues. Nonetheless, corporate earnings reports overall helped to rally the markets. First quarter operating earnings per share rose 5.3% year-over-year for the S&P 500, led by the Communication Services, Healthcare, and Technology sectors. Standard & Poor’s reports that 77% of S&P 500 companies posted higher-than-expected Q1 earnings, topping the average of roughly 73% over the trailing 13 years.

Profit growth continues to get a boost via significant share repurchases. In fact, the S&P 500 set a quarterly record for buybacks in Q1 at $293 billion, up nearly 24% year-over-year. Share buybacks—which boost earnings per share growth by reducing shares outstanding—have not been slowed by the 1% excise tax on net buybacks, part of the Inflation Reduction Act of 2022. Apple led the way with $26 billion of buybacks and amazingly holds 18 of the top 20 highest repurchase quarters. By using some of its prodigious cash flows for buybacks—the iPhone maker generated nearly $109 billion in free cash flow during fiscal 2024—Apple has been able reduce shares outstanding by nearly 36% over the past decade.

Foreign Exchange

For multinational firms with sprawling global supply chains, it was clearly a choppy first half of 2025. Some companies reacted to the policy uncertainty by throwing in the towel on providing earnings guidance, acknowledging the folly of trying to provide accurate forecasts with so many unknowns. One silver lining for these firms may have emerged from the turbulence. The U.S. dollar declined nearly 11% versus a basket of major currencies over the first six months of the year, its worst start to a year since 1973. Although a weaker dollar does make imports more expensive, it also means that revenues earned abroad in foreign currencies translate into more dollars. This is not likely to be a major tailwind, but at the margin it can be additive.

Nike, which gets more than 50% of sales from abroad, reported a roughly one percentage point negative currency impact to reported revenue growth last quarter. It hedges some of its foreign currency exposure, but for a company squarely in the path of the tariffs storm, seeing foreign exchange turn positive might ease some pain. Nike CFO Matt Friend noted on the company’s fiscal Q4 earnings call that they have “consistently been a top payer of US duties, with an average duty rate on footwear imported into the United States in the mid-teens range.” Friend added that Nike currently sources around 16% of imported footwear from China, but aims to reduce that to the high-single-digits by fiscal 2026, diversifying supply to other countries around the world.

For U.S. investors, the weaker dollar has given foreign investments added allure. Through June, the MSCI ACWI ex USA Index returned a robust 8.8% in local currency terms but jumped to a 17.9% return when translated to dollars. After years of a strong dollar weighing on (unhedged) international equity returns for U.S. investors, the reversal has sharply amplified returns. Of course, the opposite is true for international investors putting assets into U.S. markets. Longer-term, we want to continue to attract capital to our shores.

The markets, as with life, never stop moving. Still, there are moments of pause, and therein lies the power. Famed economist John Kenneth Galbraith once said, “Faced with the choice between changing one’s mind and proving there is no need to do so, almost everybody gets busy on the proof.” There is power in choosing our response. Wait for it….